US Banking Sector Valuation Compression and Credit Deterioration in October 2025

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on the Seeking Alpha report [1] published on November 7, 2025, which reported significant valuation compression in the U.S. banking sector during October 2025.

The banking sector experienced substantial valuation compression in October 2025, with the median price-to-adjusted tangible book value (TBV) declining by 7.5% to 131.2% from 141.9% at the end of September [1]. This represents the lowest month-end valuation for banks since May 2025. The sector’s performance was notably weak, with the 207 banks analyzed posting a median total return of -3.6%, significantly underperforming both the S&P US BMI Banks index (-1.1%) and the broader S&P 500 (+2.3%) [1].

The valuation decline coincided with widespread credit deterioration disclosed in third-quarter earnings reports. Specific institutions including First Internet Bancorp, Eagle Bancorp Inc., and Amerant Bancorp Inc. experienced notable credit quality issues [1]. This credit deterioration was further evidenced by isolated fraud losses affecting several banks, including JPMorgan Chase and Fifth Third Bancorp due to secured lending to Tricolor Holdings, a subprime auto lender [2]. U.S. Bancorp also reported a 14% increase in credit loss provisions in Q3 2025 compared to Q2 2025 [3].

The sector’s underperformance contrasted sharply with broader market strength. Major indices showed positive momentum over the past 30 days: S&P 500 (+1.59%), NASDAQ (+2.90%), and Dow Jones (+1.76%) [0]. However, the Financial Services sector declined 1.82% on November 6, 2025, making it one of the worst-performing sectors [0]. The Financial Select Sector SPDR Fund (XLF) declined 2.24% during October 2025, closing at $52.41 [0].

The banking sector’s valuation compression reflects fundamental concerns about asset quality and future earnings potential. The price-to-adjusted TBV metric is particularly significant for banks as it accounts for loan loss reserves and unrealized securities gains/losses, providing a more accurate picture of underlying asset quality [1]. The 7.5% monthly decline suggests rapidly eroding investor confidence.

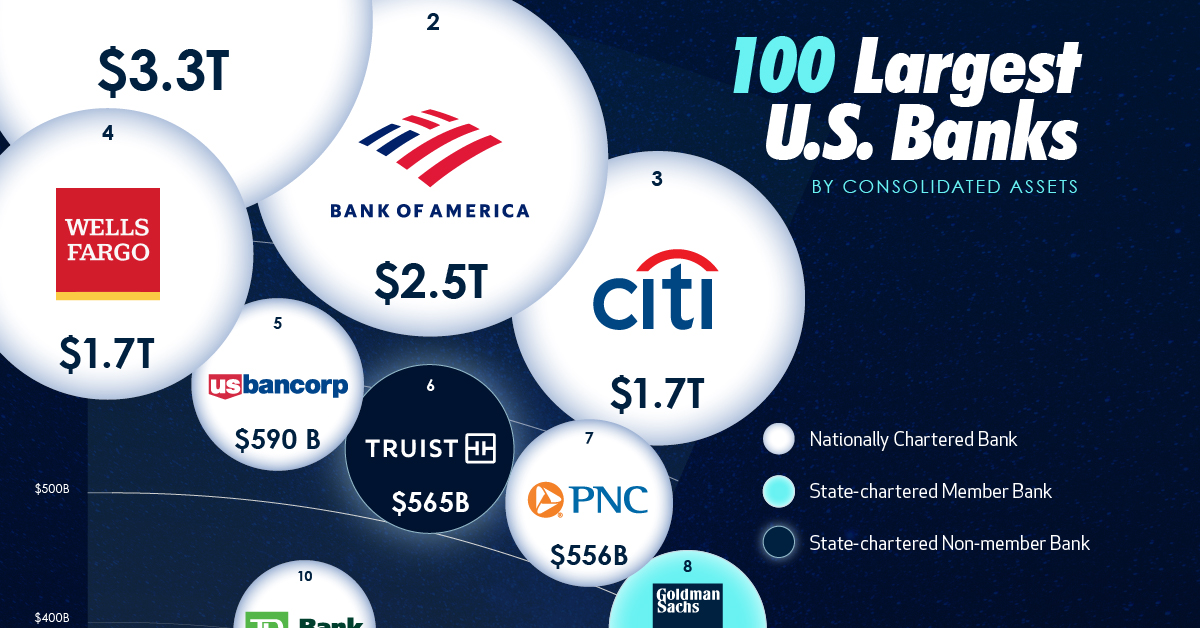

The performance divergence within the sector is noteworthy. While the median bank return was -3.6%, there was significant individual variation - Bank of America (BAC) actually gained 3.88% in October, closing at $53.29, while Wells Fargo (WFC) showed weakness [0]. This suggests that credit quality issues and market concerns are not uniformly distributed across all banking institutions.

The underperformance gap of 5.9 percentage points relative to the S&P 500 [1] indicates that the valuation compression was driven by sector-specific fundamentals rather than broad market rotation. The combination of credit deterioration and fraud losses in specific lending segments (particularly auto lending) has raised concerns about collateral management quality and underwriting standards [2].

The analysis reveals several risk factors that warrant attention. The combination of declining valuations and credit deterioration may significantly impact banking sector stability in the coming quarters. Key risk indicators include:

- Credit Quality Degradation: The reported “myriad credit issues” and specific fraud losses suggest potential for further credit deterioration [1][2]

- Valuation Compression Risk: The 7.5% monthly decline in price-to-adjusted TBV indicates rapidly eroding investor confidence [1]

- Earnings Pressure: Higher credit provisions could pressure bank earnings and dividend sustainability

- Liquidity Concerns: Credit quality issues may impact funding costs and deposit stability

Decision-makers should closely monitor quarterly credit metrics, regulatory responses, economic indicators, and market sentiment. Historical patterns suggest that banking sector valuation compression combined with credit deterioration typically leads to extended periods of underperformance and potential regulatory scrutiny [0].

The banking sector ended October 2025 with significant valuation compression, with median price-to-adjusted TBV declining to 131.2% from 141.9% in September [1]. The sector’s median return of -3.6% substantially underperformed both banking indices (-1.1%) and the broader S&P 500 (+2.3%) [1]. This underperformance was driven by widespread credit deterioration in Q3 earnings reports, specific fraud losses in auto lending, and increased credit loss provisions at major institutions [1][2][3]. The divergence from broader market performance suggests sector-specific fundamental concerns rather than general market weakness.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.