Rising Household Debt and Deepening K-Shaped Economic Divide: November 2025 Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis examines the critical economic trends highlighted in the November 7, 2025 Reddit discussion regarding rising household debt and the deepening K-shaped economic divide. The concerns raised in this post are substantiated by comprehensive economic data showing record debt levels and increasing wealth concentration that threaten the sustainability of consumer-driven economic growth.

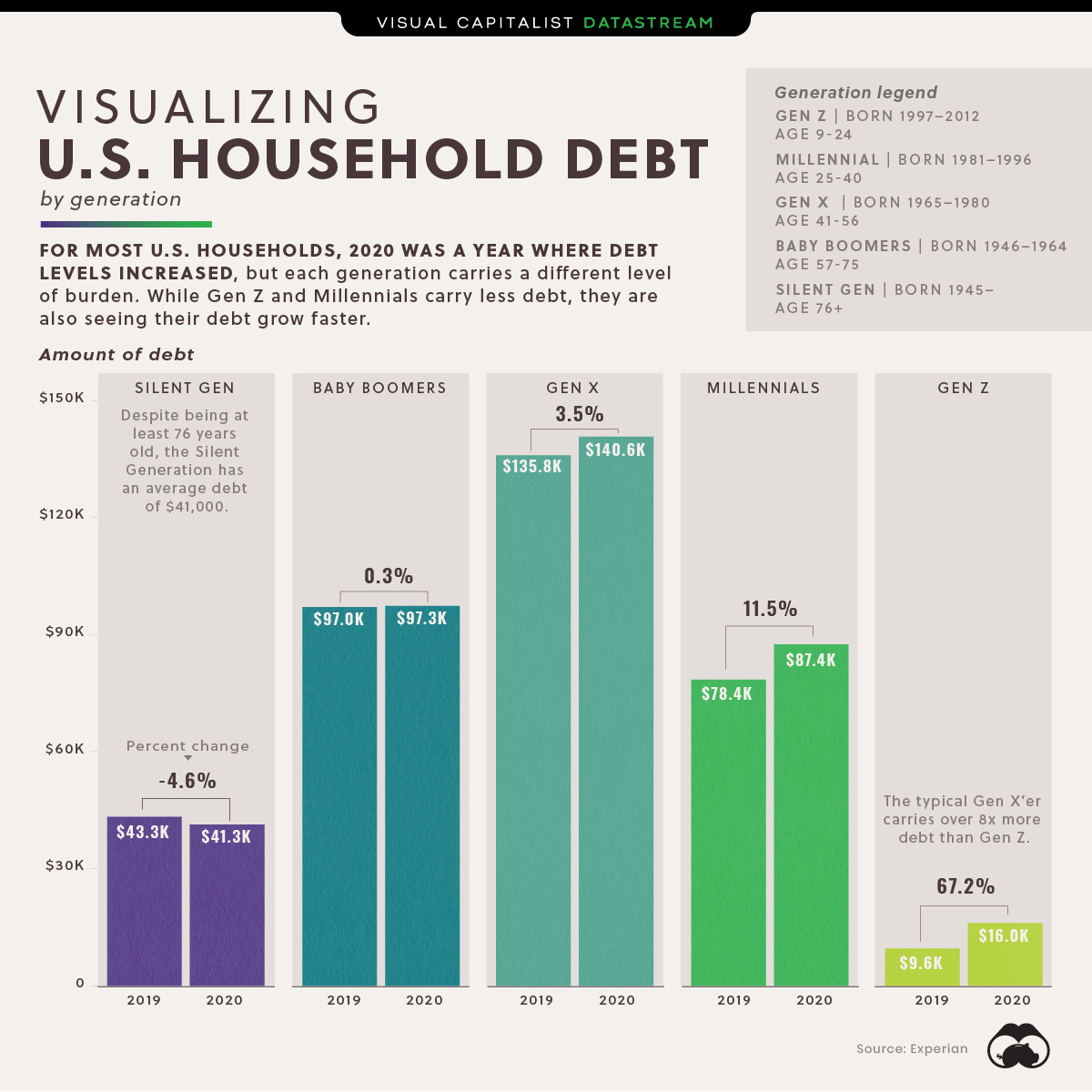

The U.S. household debt landscape has reached unprecedented levels, with total debt climbing to $18.59 trillion in Q3 2025, representing a $197 billion quarterly increase [2]. Most concerning, credit card balances have surged to an all-time high of $1.23 trillion, up $24 billion in Q3 alone and nearly 6% year-over-year [1][2]. The average consumer now carries $6,523 in credit card debt, a 2.2% increase from the previous year [1].

This debt burden is not distributed evenly across the population. TransUnion’s research reveals an increasing polarization in consumer credit risk, with more borrowers falling into either superprime (credit score 780+) or subprime (credit score below 600) categories [1]. This bifurcation mirrors the broader K-shaped economic phenomenon where different segments experience diverging economic trajectories.

The wealth concentration data underscores the severity of the economic divide. The top 10% of Americans now control over 87% of corporate equities and mutual fund shares, while the top 1% alone holds 50% of U.S. stock wealth, approximately $23 trillion [3]. This concentration creates significant vulnerabilities, as demonstrated by research showing that rising wealth inequality increases household mortgage leverage and corporate debt levels, creating financial stability risks [4].

Educational disparities further exacerbate this divide. Stock market participation shows stark differences: 84% of college graduates own stocks compared to only 42% of those with only high school education [3]. This gap in asset ownership creates long-term wealth accumulation disparities that compound over time.

The current trajectory presents fundamental challenges to consumer-driven economic growth. With approximately 60% of credit card users carrying revolving debt at roughly 20% annual interest rates [1], many households are trapped in high-cost borrowing cycles. As Moody’s chief economist Mark Zandi noted, “many are borrowing money to supplement their income and now they are paying interest on that debt” [1].

Morgan Stanley Research forecasts that U.S. consumer spending growth will weaken to 3.7% in 2025 from 5.7% in 2024, with more pronounced cooling expected among lower- and middle-income consumers [5]. This slowdown reflects the mounting pressure from debt service costs and stagnant real wages that have not kept pace with inflation.

The delinquency trends reveal emerging systemic vulnerabilities. In Q3 2025, 3% of outstanding debt became seriously delinquent (90+ days past due), marking the largest quarterly increase since 2014 [2]. Younger borrowers (18-29) face particularly acute distress with a 5% serious delinquency rate, more than double the rate from a year earlier [2].

Student loan debt presents another critical pressure point, with total outstanding balances climbing to a record $1.65 trillion [2]. This debt burden disproportionately affects younger workers at the beginning of their careers, potentially delaying wealth accumulation and homeownership.

The financial stress extends beyond balance sheets to broader social well-being. Studies indicate that 38% of consumers find it “difficult” or “very difficult” to pay bills on time, with 67% of those falling behind citing insufficient income [1]. This creates what Achieve’s co-founder Brad Stroh called “a volatile combination” that could leave lasting economic impacts on at-risk households [1].

The analysis reveals several interconnected risk factors that warrant close monitoring:

-

Financial Stability Vulnerability: The concentration of wealth and debt creates systemic risks, with the top 10% owning 89% of stock wealth [4]. Any significant market decline could trigger cascading effects throughout the economy.

-

Consumer Debt Sustainability: High-interest credit card debt combined with elevated delinquency rates suggests growing financial stress among households, particularly younger borrowers [2].

-

Economic Growth Constraints: The polarization of economic outcomes may constrain broader economic growth, as consumer spending becomes increasingly dependent on a smaller segment of high-income households [5].

While the analysis reveals significant challenges, several areas warrant continued observation for potential policy interventions and market adjustments:

-

Policy Response Effectiveness: Monitoring how monetary and fiscal policies address the wealth concentration and debt sustainability issues could provide insights into economic resilience.

-

Demographic Adaptation: Understanding how younger borrowers adapt to high debt levels may reveal emerging financial behaviors and market opportunities.

-

Regional Economic Patterns: The analysis would benefit from examining how these trends manifest across different geographic areas and housing markets.

The economic data confirms the concerns raised in the original Reddit post about rising household debt and the K-shaped economic divide. The convergence of record debt levels ($18.59 trillion), increasing wealth concentration (top 1% holding 50% of stock wealth), and rising delinquency rates creates a complex economic environment with significant implications for financial stability and sustainable growth [0][1][2][3][4][5].

The situation reflects broader structural challenges in the post-pandemic economy, where years of monetary stimulus and asset price appreciation have disproportionately benefited wealthier households while leaving many consumers increasingly dependent on high-cost debt to maintain spending levels. The emerging trends suggest that current economic growth patterns may not be sustainable without addressing the underlying wealth and debt distribution issues.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.