Analysis of November 2025 U.S. Private Sector Job Losses (ADP Report)

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

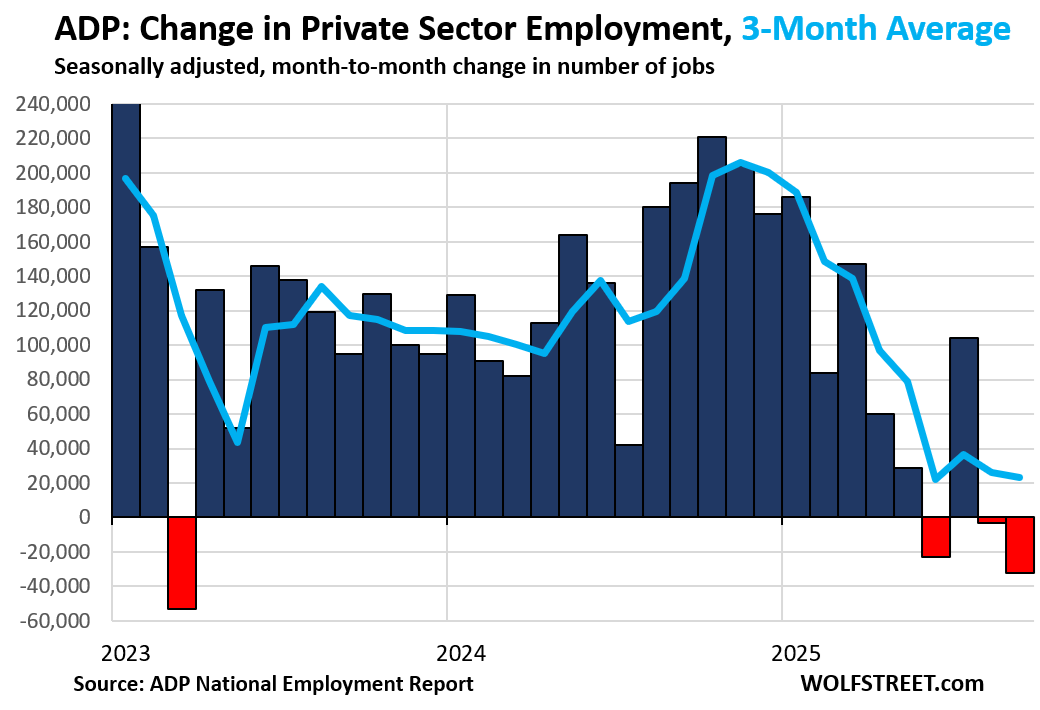

This analysis is based on the ADP November 2025 Private Sector Employment Report and associated market reactions [1]. Private employers lost 32,000 jobs, missing consensus expectations of a 40,000 gain [1]. Small businesses (1-49 workers) bore the brunt, shedding 120,000 jobs, while larger firms (50+ workers) added 90,000 [0]. Key sectors with losses included professional/business services (-26k), information services (-20k), manufacturing (-18k), financial activities (-9k), and construction (-9k) [1]. Wage growth for job stayers moderated to 4.4% year-over-year, down from 4.5% in October [1].

Despite the labor market weakness, major U.S. indices posted gains: S&P 500 (+0.18%), NASDAQ Composite (+0.13%), Dow Jones (+0.44%) [0]. This counterintuitive reaction stemmed from elevated Fed rate cut expectations, which rose to 85-90% probability for the December 9-10 meeting—up from 60-65% a month prior [7]. Sector performance varied: Consumer Cyclical (+0.97561%) and Consumer Defensive (+0.97217%) led gains, while Communication Services (-0.81876%) and Energy (-0.2683%) underperformed [0]. ADP’s stock traded up 0.49% to $258.43 during regular hours [0].

A critical context gap is the delayed BLS nonfarm payrolls report, typically more comprehensive than ADP’s data, due to a U.S. government shutdown. The BLS report is now scheduled for December 16, after the Fed meeting [5][7].

- Small Business Vulnerability: Small businesses (accounting for ~50% of U.S. private-sector employment) are disproportionately affected by labor market weakness, losing 120,000 jobs while larger firms expanded [1][6]. This highlights uneven economic resilience across business sizes.

- Market Sensitivity to Fed Policy: The positive market reaction to weak labor data underscores that near-term Fed policy expectations—rather than immediate labor market health—are driving investor sentiment [0][7].

- Wage Growth Moderation: Slowing year-over-year wage growth (4.4%) could ease inflationary pressures, potentially supporting a more dovish Fed policy stance in 2026 [2].

- Labor Market Slowdown: November marks the third job loss in four months, indicating a broad hiring slowdown that could lead to higher unemployment and weaker consumer spending if sustained [5].

- Small Business Resilience: Ongoing small business job losses threaten long-term economic stability, given their large share of employment [1][6].

- Fed Policy Calibration: A rate cut could support growth but risks reigniting inflation if not carefully calibrated [7].

- BLS Report Uncertainty: The delayed BLS report may contradict ADP’s findings, creating volatility if it shows a different labor market trend [5].

- Rate Cut Support: A Fed rate cut could benefit rate-sensitive sectors, supporting economic growth [7].

- Inflation Easing: Moderating wage growth may help bring inflation closer to the Fed’s 2% target, reducing future tightening risks [2].

The ADP report signals significant labor market weakness in November 2025, driven by small business job losses. The unexpected positive market reaction reflects investor focus on near-term Fed rate cuts, with markets pricing an 85-90% probability of a 25-basis-point cut in December. The delayed BLS report means policymakers and investors will lack comprehensive labor data ahead of the Fed meeting, adding uncertainty to policy decisions.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.