Consumer Confidence Decline Analysis: October 2025 Economic Outlook and Demographic Impact

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on the PYMNTS report [4] published on October 28, 2025, which reported that consumer confidence edged down in October as lower-income households feel strained heading into the year’s final months.

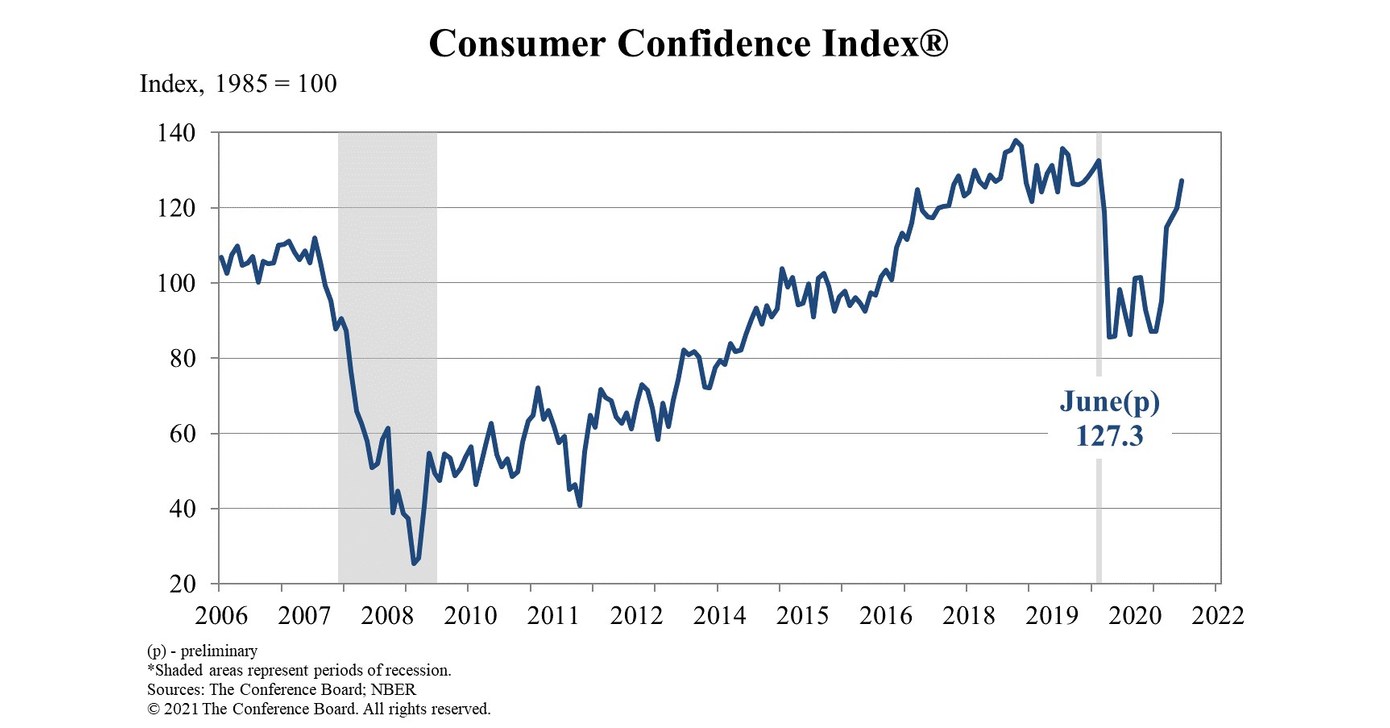

The October 2025 Consumer Confidence Index declined by 1 point to 94.6 from September’s 95.6, marking its lowest level since spring [4]. This modest headline figure masks significant underlying dynamics in consumer sentiment. The data reveals a concerning divergence between current and future economic assessments, with the Present Situation Index actually rising 1.8 points to 129.3, while the Expectations Index dropped 2.9 points to 71.5 [1].

The sustained weakness in expectations is particularly noteworthy, as the Expectations Index has remained below the critical 80-point threshold since February 2025 [3]. This level historically correlates with increased recession risk, indicating that consumers anticipate economic challenges ahead despite their current relative comfort. The timing of this decline is especially significant as it comes just before the holiday shopping season, potentially impacting retail projections and consumer spending patterns [1].

The headline emphasis on lower-income households feeling strained [4] reflects broader economic inequality trends. Research indicates that households with annual incomes under $50,000 experience significantly higher financial stress, with 53% reporting money-related stress compared to only 40% of those earning $100,000 or more [5]. This demographic divide is particularly consequential as lower-income households typically have less financial cushion to absorb economic shocks and spend a larger percentage of their income on necessities, making them more sensitive to inflationary pressures.

Despite various policy interventions, inflation remains consumers’ biggest concern according to write-in survey responses [1]. This persistence indicates that price pressures continue to affect household budgets, particularly for lower-income families. The decline in tariff mentions, while still elevated, suggests some easing of trade-related concerns, but the overall cautious outlook indicates that consumers remain wary of multiple economic factors including employment prospects and income growth.

The current confidence level of 94.6 represents a substantial erosion from 109.5 a year ago, showing significant deterioration in consumer sentiment over the past 12 months [1]. This long-term decline suggests that current concerns are not merely temporary fluctuations but reflect deeper structural economic challenges affecting household financial security and outlook.

The declining consumer confidence, particularly the weakening expectations component, signals potential headwinds for economic growth. Consumer spending drives approximately 70% of U.S. GDP, and declining confidence typically precedes reduced spending, especially on big-ticket items and discretionary purchases. The strain on lower-income households is particularly concerning as this demographic represents a substantial portion of consumer spending and could lead to reduced discretionary spending, increased reliance on credit, and delays in major purchases [1].

Businesses should anticipate potential shifts in consumer behavior, particularly in sectors serving lower-to-middle income demographics. The confidence decline may affect retail sales (especially for non-essential items), housing market activity, automotive sales, and travel and entertainment spending. The divergence between present situation assessments and future expectations suggests that while current spending may remain relatively stable, businesses should prepare for potential softening in demand heading into 2026 [1].

The sustained low level of the Expectations Index below 80 points since February 2025 indicates that consumers anticipate economic challenges ahead [3]. This could influence Federal Reserve policy decisions, fiscal policy considerations, employment and wage growth initiatives, and inflation targeting strategies. The clear demographic impact on lower-income households suggests targeted policy interventions could be particularly effective.

The October 2025 consumer confidence data reveals a complex economic landscape where current conditions appear relatively stable but future expectations remain pessimistic. The 1-point decline to 94.6 [4] represents the lowest reading since April 2025 [2], with the Expectations Index at 71.5 remaining well below the 80-point recession-risk threshold [1]. Lower-income households are experiencing particular strain [4], reflecting broader economic inequality trends where financial stress disproportionately affects those with annual incomes under $50,000 [5]. Inflation persists as the primary consumer concern [1], despite some easing of trade-related worries. The timing ahead of the holiday season and the substantial decline from 109.5 a year ago [1] suggest these trends could have significant implications for consumer spending patterns and economic growth heading into 2026.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.