Private and Liquid Credit Markets: Complementary Forces Reshaping Corporate Finance

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on the Oaktree Capital report “Friends Not Foes” [1] published on November 5, 2025, which challenges the conventional view that private and liquid credit markets are competitors. The analysis reveals that these markets have evolved into powerful complements, creating a more versatile financing ecosystem for both issuers and investors [1]. Private credit has grown to become a mainstream asset class with over $1.7 trillion in assets, fundamentally reshaping corporate financing since the 2008 financial crisis [1].

The private credit market has transitioned from an obscure niche to a mainstream asset class, now constituting a core pillar of sub-investment grade financing [1]. This evolution was catalyzed by regulatory changes following the 2008 financial crisis, where banks’ retreat from corporate lending due to stringent capital requirements created a funding gap that alternative lenders filled [1]. The COVID-19 pandemic further accelerated this trend when traditional syndicated debt markets periodically became unavailable, forcing borrowers to seek credit offering rapid execution and enhanced flexibility [1].

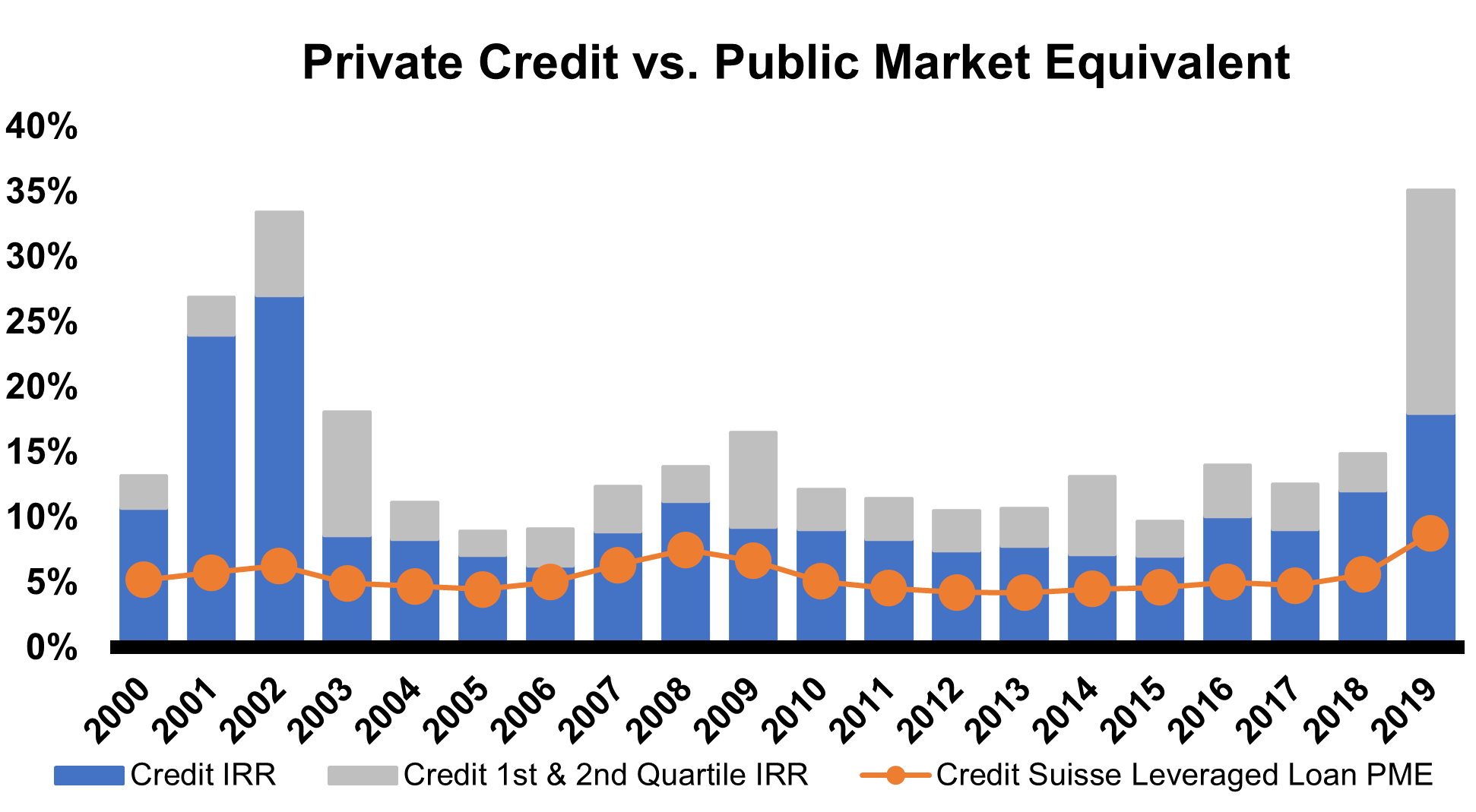

Recent data shows private credit expanded to approximately $1.5 trillion at the start of 2024, up from $1 trillion in 2020, with projections estimating growth to $2.6 trillion by 2029 [2]. This growth trajectory reflects broader institutional adoption, with pension funds and insurers increasingly viewing private credit as a core income strategy rather than a niche alternative [3].

The relationship between private and liquid credit markets demonstrates clear symbiotic characteristics. In 2022, when liquid credit markets were subdued, private lenders provided crucial financing that stabilized many public borrowers when liquid markets couldn’t help [1]. Conversely, as liquid credit markets stabilized entering 2024, public financings boomed, leading to roughly $25 billion of loans moving in each direction between direct lending and broadly syndicated loan markets [1].

This dynamic creates a more resilient financing ecosystem where borrowers can access different funding sources across varying market conditions, while investors benefit from complementary risk-return profiles [1]. The convergence in pricing is evident, with direct lending spreads falling to around SOFR+525 bps compared to approximately 370 bps for broadly syndicated loans (BSLs) [4].

European credit markets have shown remarkable activity in 2025, with the third quarter seeing record European CLO activity and robust demand helping AAA-rated spreads compress below 130 basis points for tier-one managers [1]. Direct lending activity in Europe has been particularly strong, with over €30 billion of volume so far in 2025, exceeding the level for the same period in 2024 [1].

Asset-backed finance (ABF) represents a relatively untapped corner of private credit, with the U.S. market (excluding real estate) representing approximately $5.5 trillion in addressable universe, where private lender participation remains limited [1]. The convertible bond market has also experienced exceptional growth, with September setting a monthly record for convertible bond issuance at nearly $30 billion [1].

The market remains bifurcated by quality, with well-regarded names remaining well bid while lower-quality issuers face significant challenges. Recent data shows CCC-rated loans trading outside their historical average, with spreads exceeding 1,200 bps, while B- and BB-rated loans trade within their long-term average spread range [1]. This quality bifurcation is exacerbated by a CLO buyer base with limited appetite for CCC-rated loans, creating selective competition primarily focused on higher-quality credits [1].

For issuers, the dual access to liquid and private credit markets provides crucial flexibility, allowing companies to optimize their capital structure based on prevailing market conditions, pricing, and execution requirements [1]. Large borrowers particularly benefit from having two sets of lenders that can step in across different market conditions, with private lenders able to move unilaterally or in smaller groups, circumventing banks that may be constrained by hung loans or risk aversion [1].

For investors, sophisticated portfolio optimization is possible by combining liquid and private credit to solve for an optimal blend of yield, liquidity, and volatility [1]. The liquid portion can meet investor liquidity requirements and allow rapid capital deployment, while the private portion dampens volatility and offers yield premiums [1].

- Continued Growth Trajectory: Private credit funds currently have more than $250 billion in dry powder to deploy, creating competitive pressure that should continue to drive market activity [4]

- Technological Advancement: Advances in technology and data analytics are enabling more sophisticated credit underwriting and risk management, particularly important for private credit where information asymmetry can be significant [1]

- Diversification Benefits: The new diversification lever for investors is evolving from a static 40% investment grade corporate bond allocation to a dynamic portfolio of private and liquid credit [1]

- Quality Concentration Risk: The market bifurcation by quality creates potential concentration risk, with lower-quality issuers facing significant challenges and limited access to capital [1]

- Regulatory Dependency: The continuing impact of post-2008 banking regulations remains a fundamental driver, and any regulatory changes could affect the competitive dynamics [1]

- Interest Rate Sensitivity: While the “higher for longer” interest rate environment currently supports attractive yields, changes in monetary policy could impact both private and liquid credit markets [1]

The symbiotic relationship between private and liquid credit markets represents a fundamental shift in corporate financing, moving away from a zero-sum competitive view toward a complementary ecosystem that benefits all stakeholders. The convergence in pricing and terms, particularly in larger deals, reflects market maturity and increased competition [4]. However, quality bifurcation remains a key characteristic, with well-regarded names commanding favorable terms while lower-quality issuers face challenges [1].

The “higher for longer” interest rate environment continues to support attractive yields in both markets [1], while technological advancements are helping bridge information gaps between private and liquid markets [1]. With substantial dry powder available for deployment and sustained capital expenditure requirements across Western economies, the complementary relationship between these markets is expected to strengthen further [1, 4].

Financing requirements will remain high as large-cap M&A activity gradually returns and borrowers seek to refinance a looming wall of debt [1]. The continued growth in capex requirements across data center financing, increased defense expenditure, and digital infrastructure build-out creates sustained demand for both private and liquid credit solutions [1].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.