Fed Rate Cuts and China Trade Deal: Market Analysis and Investment Opportunities

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

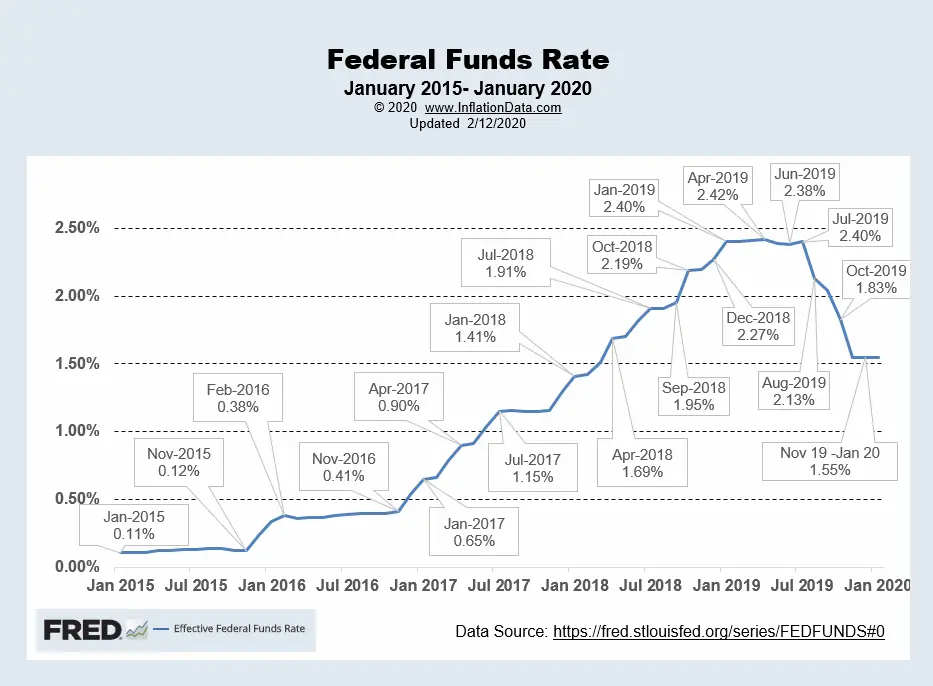

This analysis is based on the MarketWatch report [1] published on November 4, 2025, examining investment opportunities following the Federal Reserve’s latest rate cut and the Trump-Xi trade meeting. The Fed reduced rates by a quarter-point and announced it would stop shrinking its balance sheet in December, while Fed Chair Powell suggested no December rate cut might occur [1].

Current market performance reveals significant sector divergence. Major indices show weakness with the S&P 500 down 0.25%, NASDAQ declining 0.34%, and Russell 2000 falling 0.61% [0]. However, this masks important underlying patterns: technology and semiconductor stocks face substantial pressure (QQQ -1.91%, SMH -3.08%), while financial sectors show resilience (XLF +0.51%) and investors seek safety in long-term Treasuries (TLT +0.23%) [0].

The U.S.-China trade agreement introduces both opportunities and complexities. The deal reduces tariffs on Chinese imports, simplifies access to Chinese rare-earth elements, and restarts Chinese soybean purchases [1]. However, current market sentiment appears more cautious than the article’s optimistic scenarios would suggest, with small-cap stocks under pressure despite expected trade deal benefits.

The most significant insight is the disconnect between expected trade deal benefits and actual market behavior. While the analysis suggests smaller caps and technology should benefit from improved trade relations, current data shows technology weakness and small-cap underperformance [0]. This indicates investors may be more concerned about Fed policy uncertainty and potential inflation surprises than trade deal optimism.

The November 13th CPI release emerges as a critical market catalyst. While consensus expects inflation near 3% year-over-year, upside surprises to 3.2%+ could trigger rapid market rotation out of growth stocks [1]. The article highlights core PCE services inflation as “stubborn,” suggesting underlying inflation pressures may persist despite headline improvements.

The ongoing partial government shutdown adds significant uncertainty, potentially affecting economic data reliability and transportation sector timing [1]. This creates a complex environment where traditional economic indicators may be less reliable, making investment decisions more challenging.

-

Inflation Surprise Risk:An upside inflation reading could quickly reverse current market trends, particularly affecting technology and growth stocks [1].

-

Fed Policy Uncertainty:Powell’s hint of no December cut creates ambiguity that could increase market volatility around economic data releases [1].

-

Trade Policy Implementation Risk:The article acknowledges potential “snags in the deal” that could reverse expected gains, particularly in the semiconductor sector [1].

-

Data Reliability Concerns:The government shutdown may affect the accuracy of upcoming economic reports, complicating investment decisions [1].

Despite risks, several opportunities exist if key conditions are met:

-

Financial Sector Strength:The current resilience in financial ETFs (XLF +0.51%) suggests potential continued benefit from rate cut environment [0].

-

Transportation Sector Recovery:If the government shutdown ends by mid-November, transportation stocks could benefit from improved economic activity [1].

-

Treasury Bond Demand:Current flight-to-safety behavior (TLT +0.23%) indicates potential continued bond market strength during uncertainty periods [0].

Current market data suggests investors are positioning more defensively than the article’s optimistic scenarios would indicate. The significant underperformance of technology and small-cap stocks, despite potential trade deal benefits, indicates concerns about Fed policy path and inflation risks may outweigh trade optimism [0].

The Fed’s balance sheet policy shift ending quantitative tightening in December could provide liquidity support, but the impact remains uncertain without quantitative details [1]. The recommended 20-30% cash allocation appears prudent given current uncertainties and mixed market signals.

Critical monitoring points include the November 13th CPI release, employment data quality given shutdown effects, Fed communication clarity, and specific trade deal implementation timelines [1]. Technical levels to watch include QQQ RSI above 70 and 10-year Treasury yields below 4% as key market indicators [1].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.