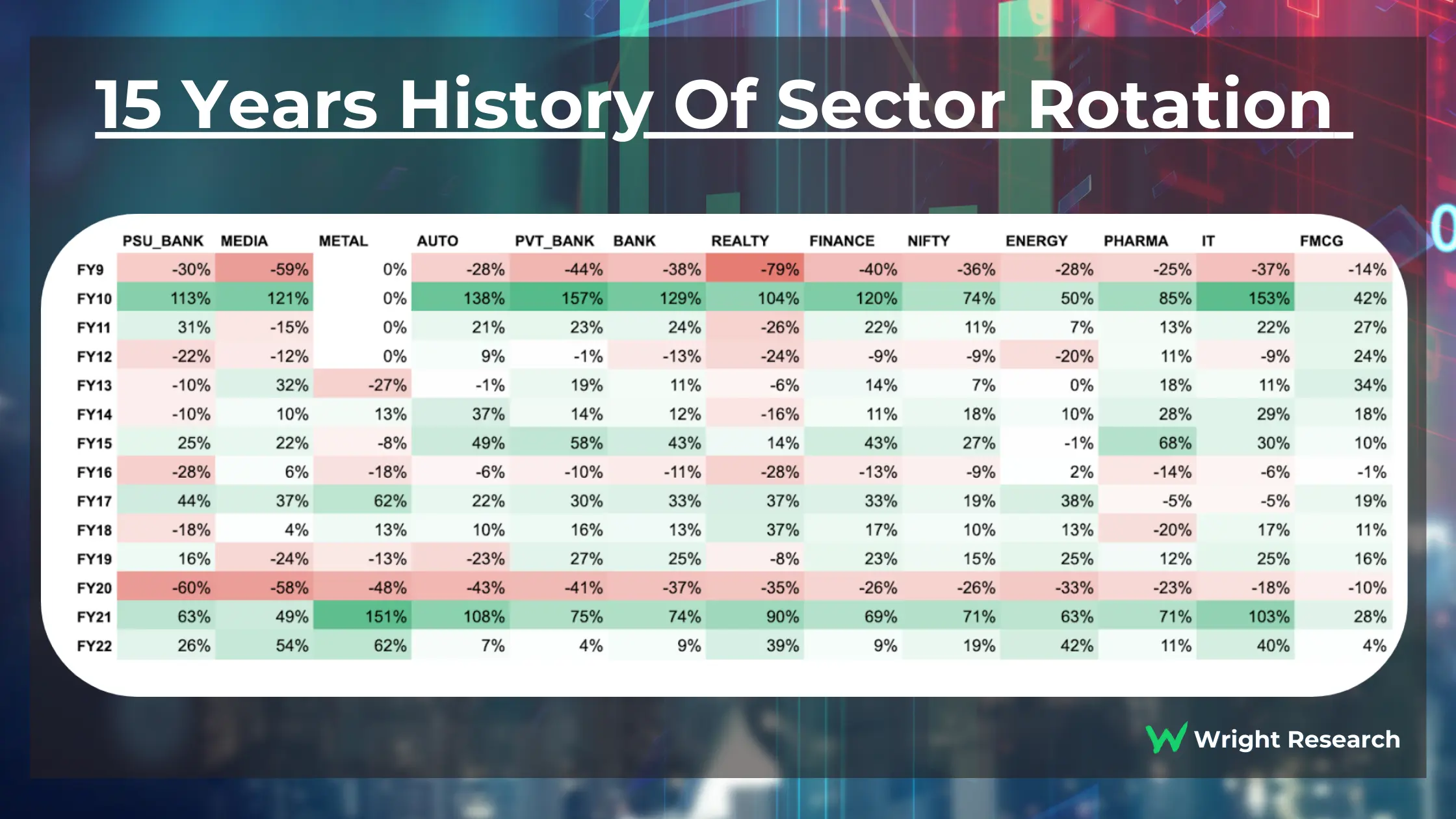

Intraday Market Update - November 4, 2025: Modest Gains Amid Sector Rotation

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on market data and news developments from November 4, 2025, covering the midday trading session [0][1][2][3].

U.S. equity markets are trading modestly higher in the midday session, with the S&P 500 gaining 0.21% to 6,802.59, the Nasdaq Composite advancing 0.30% to 23,529.68, and the Dow Jones Industrial Average adding 0.13% to 47,209.69 [0]. The Russell 2000 is also up 0.12% to 2,450.66, indicating broad-based participation across market capitalizations.

The session is characterized by notable sector rotation away from technology toward more cyclical sectors. Energy (+1.17%) and Basic Materials (+0.84%) are the clear leaders, while Consumer Cyclical (+0.65%) also shows strength [0]. Conversely, Industrials (-0.52%), Real Estate (-0.30%), and Communication Services (-0.21%) are lagging. This rotation suggests investors may be seeking value and cyclical exposure amid uncertainty in high-growth technology names.

Trading volume patterns indicate moderate market participation. S&P 500 volume stands at 1.37 billion shares, while the SPDR S&P 500 ETF (SPY) is trading down 0.83% on elevated volume of 28.12 million shares compared to its average of 72.75 million [0]. Large volume bursts in S&P 500 stocks reached 59.4 million shares worth $9.7 billion in transactions, with Technology showing the biggest dollar volume bursts [3].

Several major corporate announcements are significantly impacting individual stocks:

-

Gartner (IT)plunged 8.62% to $224.71 despite announcing increased 2025 guidance and over $1 billion stock buyback program, demonstrating that even positive fundamental news can be met with skepticism in current market conditions [1][0].

-

Palantir Technologies (PLTR)continued its decline, falling 6.95% to $192.79 on heavy volume of 70.59 million shares. This extends yesterday’s 6.8% drop despite beating Q3 estimates, suggesting valuation concerns may be outweighing earnings performance [1][0].

-

Xanadu Quantum Technologiesannounced going public via SPAC merger with Crane Harbor, valuing the combined entity at $3.1 billion, potentially creating new investment opportunities in the quantum computing space [1].

President Trump announced via Truth Social that SNAP benefits will only be paid after a government shutdown ends, appearing to defy federal court rulings. This development could impact consumer sentiment and retail sector performance [1]. Additionally, Federal Reserve Governor Lisa D. Cook is scheduled to speak on “The Economic Outlook and Monetary Policy” at 1:00 PM ET, which could provide guidance on future rate policy [2].

Nippon Steel unveiled a $14 billion investment plan for U.S. Steel operations, potentially signaling confidence in U.S. manufacturing and infrastructure [1]. U.S. Steel (X) is trading flat at $54.84 on elevated volume of 14.51 million shares near its 52-week high of $54.91, suggesting investor interest in the company’s prospects [0].

-

Government Shutdown Uncertainty:The ongoing political standoff regarding SNAP benefits and potential government shutdown could negatively impact consumer confidence and retail sector performance [1].

-

Technology Sector Volatility:The continued weakness in high-growth technology stocks, particularly Palantir and Gartner, suggests valuation concerns may persist despite strong earnings [0][1].

-

Fed Policy Uncertainty:Upcoming commentary from Fed Governor Lisa Cook could impact rate expectations and market volatility [2].

-

Cyclical Sector Strength:Energy and Basic Materials are showing strong performance, potentially offering opportunities for investors seeking sector rotation plays [0].

-

M&A Activity:The Nippon Steel investment in U.S. Steel and the Xanadu SPAC merger suggest continued M&A activity in specific sectors [1].

-

Value Opportunities:The rotation away from high-growth technology may create value opportunities in overlooked sectors or individual stocks that have been oversold [0].

The current market environment is characterized by modest overall gains but significant underlying sector rotation. Major indices are trading higher, but the leadership has shifted from technology to more cyclical sectors like Energy and Basic Materials [0]. Individual stock volatility remains elevated due to earnings reactions and corporate announcements, with notable declines in Gartner (-8.62%) and Palantir (-6.95%) despite positive fundamental news [1][0].

Technical levels show the S&P 500 trading between support at 6,766 (today’s low) and resistance at 6,820 (today’s high), while the Nasdaq is between 23,422 and 23,644 [0]. Market sentiment appears mixed, with investors balancing positive corporate developments against concerns about government shutdown and technology valuations.

The afternoon session will be influenced by Fed Governor Cook’s speech at 1:00 PM ET and any developments regarding the government shutdown situation [1][2]. Investors should monitor volume patterns and sector rotation signals for indications of market direction heading into the close.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.