JPMorgan November Chartbook: Optimistic Outlook for Eurozone and Emerging Markets

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on the Proactive Investors report [1] published on November 3, 2025, which detailed JPMorgan’s latest market outlook. The bank’s equity strategists, led by Chief Equity Strategist Mislav Matejka, have shifted to a more optimistic stance on global equities, particularly highlighting opportunities in the Eurozone and emerging markets [1].

The report identifies three key drivers supporting this improved outlook: a “calmer global backdrop,” “improving signals from China,” and a more favorable growth-policy trade-off with “moderating inflation and easing central banks creating room for equities to push higher” [1]. This strategic assessment aligns with current market performance data showing the S&P 500 gaining 2.44% and the NASDAQ Composite increasing 4.88% over the past 30 trading days [0].

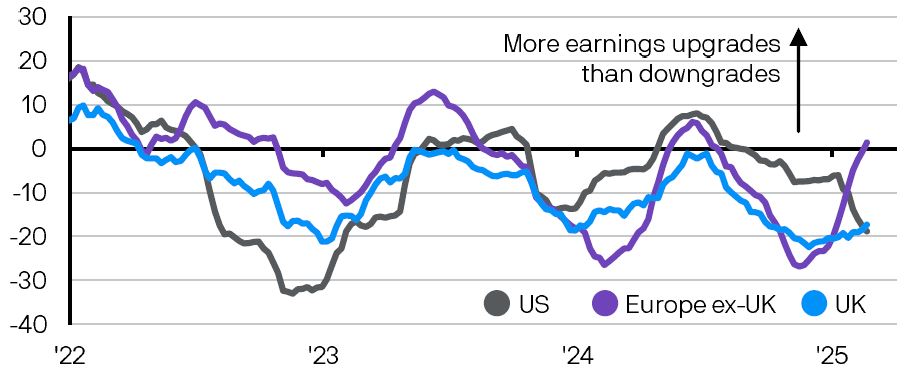

JPMorgan’s regional rotation thesis emphasizes moving away from this year’s outperformers (defense stocks and banks) into exporters, French equities, and interest rate-sensitive sectors like utilities and real estate [1]. Current sector data partially supports this view, with Real Estate performing strongly (+1.77%) and Financial Services showing gains (+1.38%), though Technology continues to lag (-1.74%) [0].

The bank’s bullish stance on emerging markets is particularly noteworthy given recent performance data. The MSCI Emerging Markets Index has shown remarkable strength in 2025, up nearly 27% year-to-date compared to the S&P 500’s 14% returns [2]. This significant outperformance validates JPMorgan’s overweight positioning on emerging markets versus developed markets and suggests the rotation may already be underway.

JPMorgan’s reiteration of its Eurozone equities upgrade suggests the region may “finally break out of its sideways drift since spring” [1]. This represents a potentially significant opportunity as European markets have historically lagged US counterparts, and a catch-up trade could provide substantial returns if the bank’s thesis materializes.

The bank’s emphasis on the improving growth-policy trade-off highlights the critical role of monetary policy in supporting equity markets. With inflation moderating and central banks expected to maintain a “gentler monetary stance” through next year [1], the accommodative policy environment could provide sustained support for risk assets, particularly rate-sensitive sectors.

-

US Labor Market Vulnerability: JPMorgan specifically identifies a sharper-than-expected slowdown in the US labor market as a key risk that could derail the optimistic scenario [1].

-

AI Trade Froth: The bank warns about potential overvaluation in artificial intelligence-related stocks, suggesting concentration risk in popular technology themes [1].

-

Crowded Positioning Risk: Investor positioning could create volatility during the anticipated sector rotations [1].

-

China Recovery Sustainability: While signals from China are improving, the economic recovery remains fragile and could reverse quickly.

-

Policy Implementation Risk: Central bank signals of easing may not translate into timely policy implementation.

The analysis suggests several key opportunities:

-

Emerging Markets Catch-up: With EM indices already showing strong performance [2], continued outperformance could provide significant alpha opportunities.

-

Eurozone Rotation: The potential breakout from Eurozone’s sideways drift since spring [1] offers substantial upside potential.

-

Sector Rotation Benefits: Interest rate-sensitive sectors like utilities and real estate could benefit from continued monetary easing [1].

-

Export-Oriented Plays: Improved Chinese outlook and declining trade tensions create a constructive setup for export-oriented companies [1].

JPMorgan’s November chartbook presents a compelling case for increased exposure to Eurozone and emerging markets, supported by improving macroeconomic conditions and favorable monetary policy trends. The bank’s strategic emphasis on rotating out of this year’s outperformers into undervalued sectors aligns with current market dynamics showing strength in real estate (+1.77%) and financial services (+1.38%) [0].

The report’s optimism is grounded in three fundamental pillars: moderating inflation pressures, accommodative central bank policies, and improving Chinese economic signals [1]. However, the analysis acknowledges potential headwinds including US labor market risks, AI sector overvaluation, and crowded positioning that could create volatility during rotations.

Current market data partially validates JPMorgan’s thesis, with emerging markets already demonstrating significant outperformance in 2025 [2] and sector rotation patterns beginning to emerge. The coming months will be critical in determining whether the anticipated Eurozone breakout and continued emerging market strength materialize as the bank projects.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.