S&P 500 Record High Amid Fed Rate Cut Uncertainty - Market Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on the Seeking Alpha report [1] published on November 3, 2025, which reported that the S&P 500 set a new record high amid shifting Federal Reserve rate cut expectations.

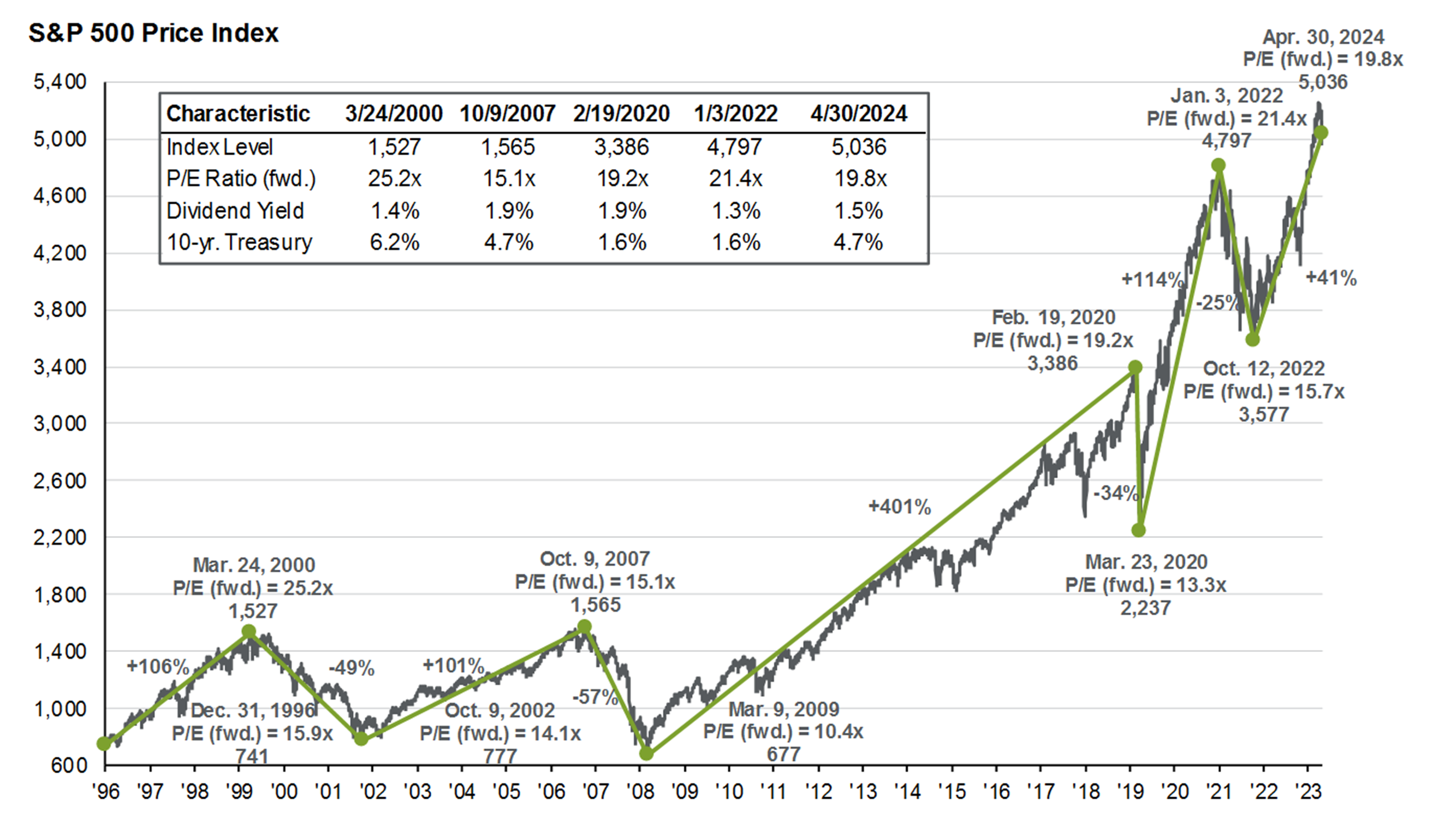

The S&P 500’s achievement of a record high of 6,890.89 on October 28, 2025, represents a complex market scenario where apparent strength masks underlying vulnerabilities [1]. The rally was catalyzed by two significant developments: a new U.S.-China trade truce over the weekend and substantial deals and earnings announcements from AI companies on Tuesday [1]. However, this positive momentum has been tempered by evolving Federal Reserve policy expectations.

Following the Fed’s recent quarter-point reduction of the Federal Funds Rate to a target range of 3.75-4.00%, market expectations for further monetary easing have diminished significantly. The CME Group’s FedWatch Tool, which previously showed over 90% probability of a December 2025 rate cut, now indicates only a 63% chance of additional easing [1][2]. This represents a substantial shift in market sentiment regarding monetary policy trajectory.

The market’s reaction has been nuanced. While the index reached its peak on October 28, subsequent trading sessions reveal consolidation and profit-taking:

- October 29: S&P 500 closed at 6,890.59 (-0.29%) [0]

- October 30: S&P 500 closed at 6,822.34 (-0.56%) [0]

- October 31: S&P 500 closed at 6,840.20 (-0.57%) [0]

This 0.7% pullback from the record high suggests investors are reassessing positions in light of the revised Fed outlook [0].

The most telling aspect of current market dynamics is the pronounced sector rotation occurring beneath the surface of the index record [3]. Traditional rate-sensitive sectors are outperforming while growth-oriented areas lag:

- Financial Services: +1.38%

- Real Estate: +1.77%

- Energy: +2.81%

- Technology: -1.74%

- Utilities: -2.00%

- Basic Materials: -1.30%

This rotation pattern is classic for environments where rate cut expectations diminish. Financial Services benefit from potentially higher net interest margins, while Technology and Utilities face pressure from higher discount rates affecting growth stock valuations [3].

A critical concern emerging from the analysis is the weak market breadth despite the record high. Only 5 out of 11 sectors posted positive returns, indicating that the index’s strength is concentrated rather than broad-based [3]. This divergence between market cap-weighted and equal-weighted indices has been noted in broader market analysis, suggesting gains are driven by mega-cap stocks rather than widespread market participation [4].

The Federal Reserve’s communication strategy appears to be creating uncertainty about future policy direction. The reduction in December rate cut probability from over 90% to 63% suggests either:

- Fed officials are signaling more caution about future rate cuts

- Recent economic indicators show more resilience than expected

- Futures markets are adjusting to a potentially higher-for-longer rate environment [1][2]

This policy uncertainty creates a challenging environment for market participants, particularly those positioned for continued monetary easing.

The current market environment presents conflicting signals between index performance and underlying market health. The S&P 500’s record high of 6,890.89 on October 28, 2025, was driven by positive developments including U.S.-China trade truce and AI sector strength [1]. However, this surface-level strength masks concerning underlying dynamics:

- Fed Policy Uncertainty: December 2025 rate cut probability has fallen from 90%+ to 63%, creating headwinds for growth-oriented investments [1][2]

- Weak Market Breadth: Only 45% of sectors are positive, indicating narrow rather than broad-based market strength [3]

- Sector Rotation: Clear shift away from Technology (-1.74%) toward Financial Services (+1.38%) and Real Estate (+1.77%) [3]

- Market Concentration: Gains concentrated in mega-cap stocks, increasing vulnerability to large-cap corrections [4]

Decision-makers should carefully monitor Fed communications, upcoming economic data releases, market breadth indicators, and yield curve movements for additional clarity on market direction. The current environment of heightened policy uncertainty suggests increased volatility potential, particularly if economic data continues to surprise to the upside and further reduces rate cut expectations.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.