Titan Mining (TII) NYSE American Uplisting Analysis: Critical Minerals Growth Potential

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

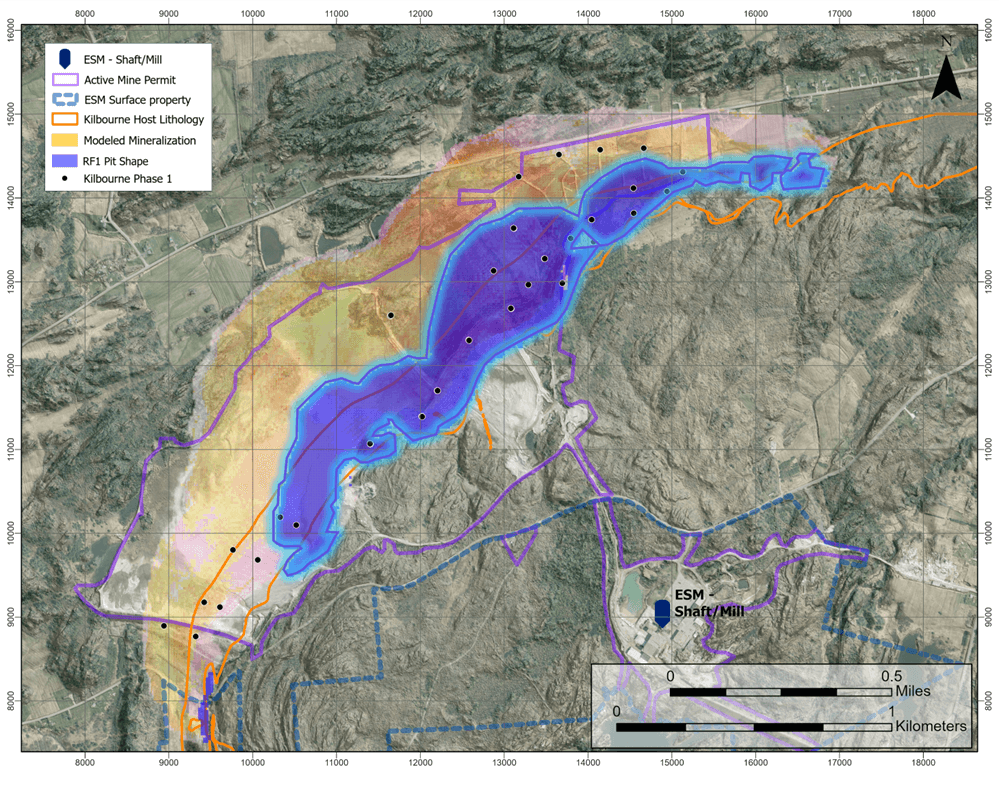

Titan Mining (NYSE American: TII; TSX: TI) completed its uplisting to NYSE American on November 21, 2025 [1], transitioning from OTCQB (TIMCF, now ceased). The company operates a cash-flow positive zinc mine (Empire State Mine) and is expanding into natural flake graphite production with a target of 40,000 tonnes/year, potentially supplying ~50% of U.S. demand [2]. It has received a Letter of Interest from the U.S. EXIM Bank for up to $120M in financing for its Kilbourne Graphite Project [2].

Short-term market impact: TI.TO (TSX) closed at $3.46 on Nov21, up 0.58% in after-hours trading [4]. TIMCF (OTC) closed at $2.38, up 0.85% with low volume (8.5k shares) [5]. The Basic Materials sector was up 1.39% on Nov21, aligning with positive sentiment for critical minerals [6].

Long-term implications: Uplisting is expected to increase institutional investor participation and liquidity [1]. The graphite project aligns with U.S. domestic supply chain goals, positioning Titan to benefit from policy tailwinds like the Inflation Reduction Act [3].

- Critical Minerals Alignment: Titan’s graphite project addresses U.S. supply chain vulnerabilities, as graphite is a key battery material and defense input. The project’s potential to supply ~50% of U.S. demand underscores its strategic value [2].

- Diversified Revenue Streams: The company combines existing cash-flow positive zinc operations with emerging graphite production and potential germanium extraction (21g/t concentrations at Empire State Mine) [3].

- Investor Access Expansion: Uplisting to NYSE American removes barriers for U.S. institutional investors, which could support future capital raises for the graphite project [1].

- Policy Tailwinds: Alignment with U.S. critical minerals initiatives may lead to incentives or contracts [3].

- Institutional Investment: Increased liquidity post-uplisting could attract larger investors [1].

- Graphite Demand Growth: Global demand for battery-grade graphite is projected to rise, benefiting domestic producers [2].

- Execution Risk: Graphite production is in commissioning phase (target Q42025), with delays potentially impacting revenue timelines [3].

- Financing Uncertainty: The EXIM Bank financing is a Letter of Interest, not a final agreement [2].

- Commodity Price Volatility: Zinc and graphite prices are subject to global market fluctuations [4].

- Small Cap Volatility: Titan’s market cap (~$314M CAD) increases sensitivity to market sentiment [4].

- Uplisting: Completed Nov21, 2025 (NYSE American: TII; OTC TIMCF ceased).

- Operations: Cash-flow positive zinc mine (Empire State Mine), graphite project (40k tonnes/year target).

- Financing: $120M EXIM Bank Letter of Interest.

- Metrics: TI.TO (Market Cap: $314.57M CAD, P/E:18.21); TIMCF (Market Cap: $216.23M USD, P/E:23.80) [4,5].

- Timelines: Graphite commissioning Q42025, customer qualification Q12026 [3].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.