S&P 500 November 2025 Performance Analysis: Worst Since 2008

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

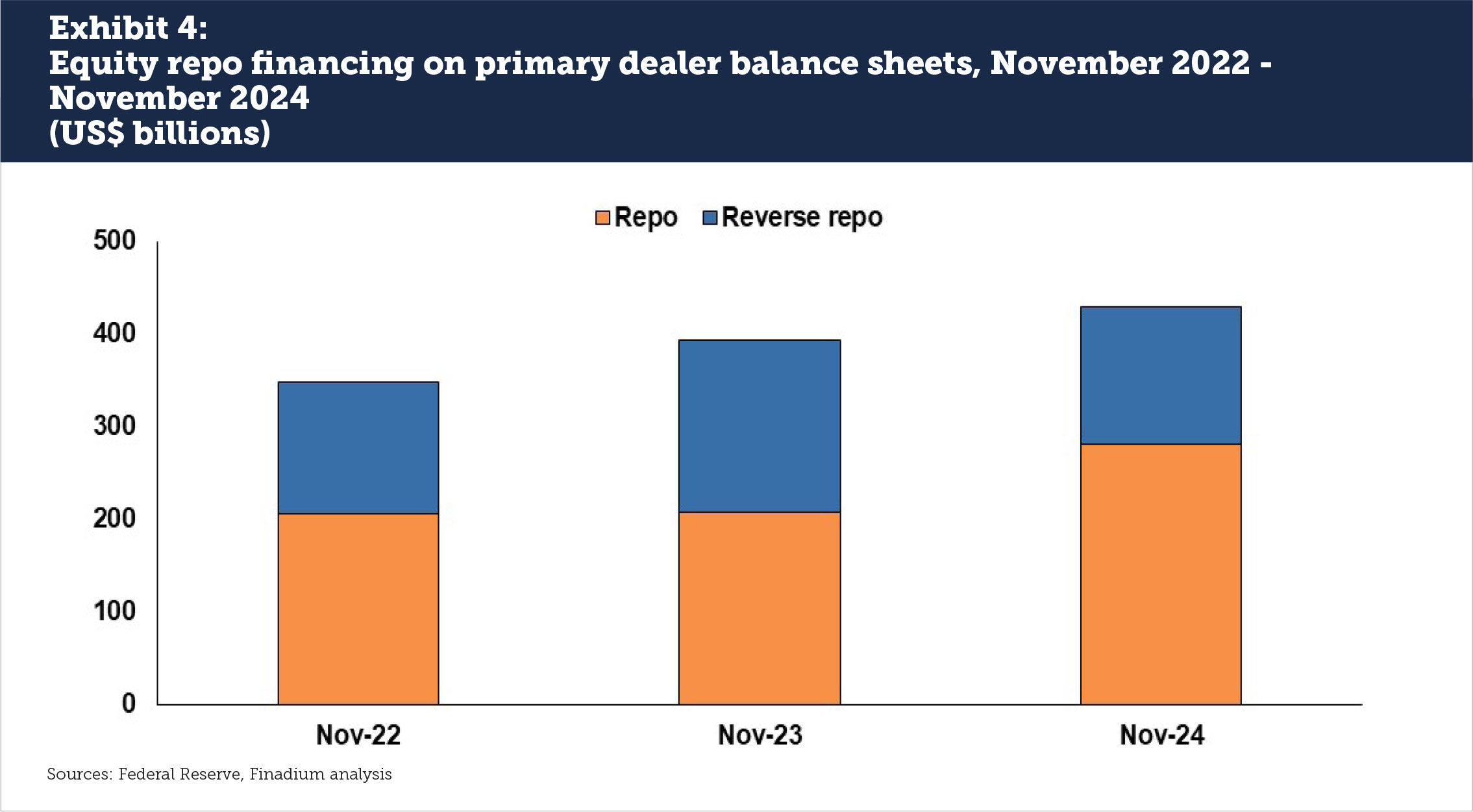

The S&P 500 has declined ~3.42% in November 2025 (from Nov3 close 6851.98 to Nov18 close6617.33) [0], marking its worst November performance since 2008. This decline is driven by liquidity tightness in short-term funding markets—repo rates remain high despite Fed cuts [4]—and investor caution, leading to a rotation to defensive sectors. Defensive sectors like Energy (+2.01%) and Utilities (+1.15%) outperformed, while cyclicals such as Consumer Defensive (-1.62%) and Consumer Cyclical (-0.94%) underperformed [0]. The 10-2 Year Treasury yield spread (0.53%) is below its long-term average (0.85%) [6], indicating ongoing market uncertainty.

- Defensive Rotation: The shift to defensive sectors suggests investor caution but not panic—unlike 2008, when the S&P500 declined ~11.32% by Nov18 [2][3].

- Liquidity Over Volatility: The decline is more tied to funding market stress than equity volatility alone, as highlighted by persistent repo rate highs [4].

- Magnitude Context: While the worst since 2008, the 2025 decline is significantly smaller (3.42% vs.11.32% in 2008 up to Nov18), indicating less systemic risk [2][3].

- Risks: Persistent repo rate tightness may increase corporate funding costs, pressuring cyclical sector earnings [4]. Further declines in cyclical sectors (Tech, Consumer Cyclical) are possible if liquidity issues persist.

- Opportunities: Defensive sectors (Energy, Utilities, Healthcare) offer relative safety amid market uncertainty [0]. Monitoring Fed policy announcements for liquidity relief could present tactical opportunities.

The S&P500’s November 2025 decline (~3.42%) is the worst since 2008 but less severe. Defensive sectors outperform cyclicals, driven by liquidity concerns (high repo rates). Key metrics: Energy (+2.01%), Consumer Defensive (-1.62%), repo rates high [0][4]. Investors should monitor repo rates and Fed actions for future market direction.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.