TruGolf Holdings (TRUG) Compact Indoor Golf Simulator Market Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

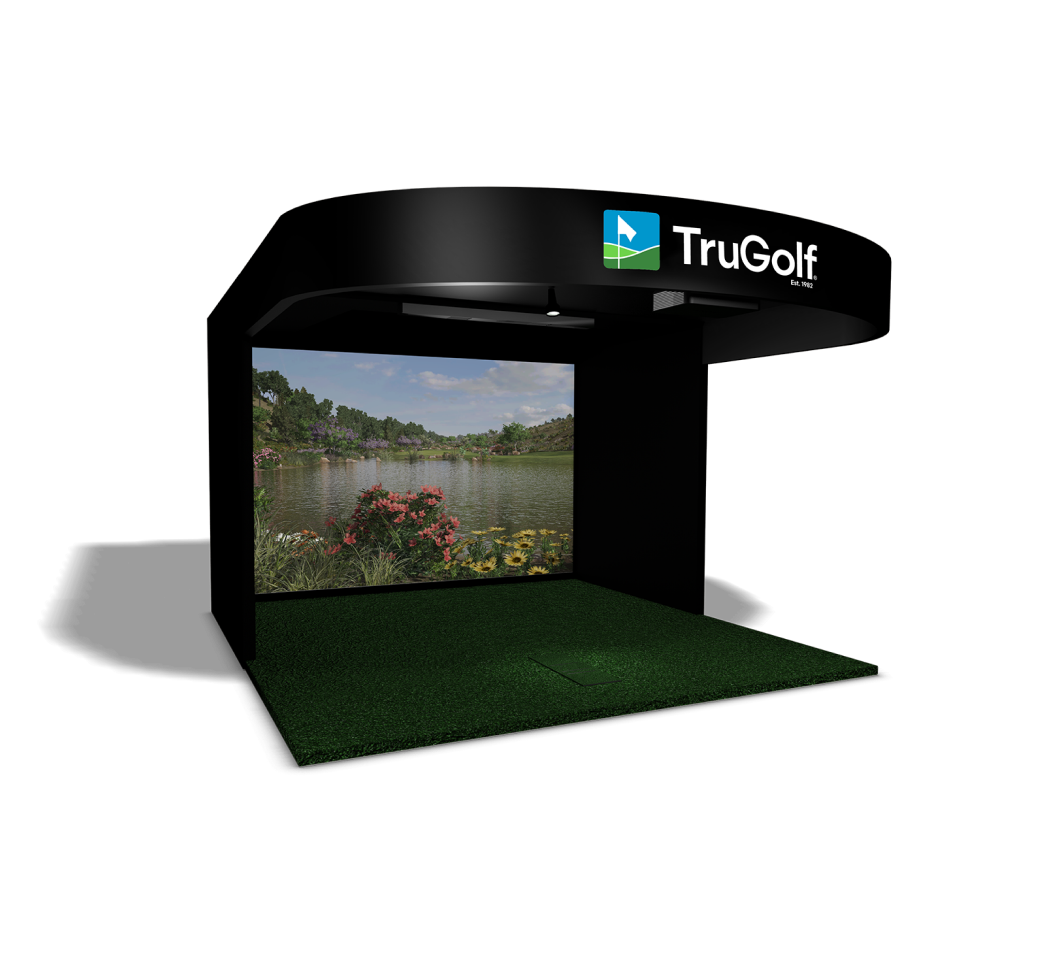

TruGolf Holdings (TRUG) operates in the $1.9B-$2.2B global indoor golf simulator market [3], focusing on compact, urban-friendly designs to address space constraints in dense cities [1]. Its core products include simulators with high-speed camera launch monitors (Apogee) and E6 Connect software (LiDAR-scanned courses) [1], with recent AI integration via the 2025 mlSpatial acquisition [4]. The company’s Q3 2025 results show 69% gross margins and $11.4M unrestricted cash [2], supporting franchise expansion (e.g., Golf Everywhere partnership [0]). TRUG’s market cap ($2.2M) trades below book value ($4.3M) [2], indicating potential undervaluation. Competitive analysis reveals TRUG’s strengths in compact footprint (50-70% less space than TopGolf [5]) and software ecosystem [1], while facing challenges from larger players like TrackMan and Golfzon [4].

- Urbanization Alignment: TruGolf’s compact model capitalizes on global urbanization trends (68% of population by 2050 [3]), driving demand for space-efficient leisure options.

- Software Moat: E6 Connect’s wide adoption (used by multiple simulator brands [1]) creates switching costs for users.

- AI Differentiation: The mlSpatial acquisition positions TRUG to lead in personalized training features, widening its competitive gap [4].

- Undervaluation Signal: Market cap below book value suggests the market may underappreciate TRUG’s cash reserves and growth potential [2].

- Opportunities: Franchise expansion into urban markets [0], AI-enhanced product offerings [4], and growing indoor golf participation (15% of new players [3]).

- Risks: Franchise execution delays [0], TopGolf’s potential compact venue launch [5,4], AI scaling challenges [4], zoning restrictions for commercial venues [5], and limited brand recognition vs. competitors [4].

- Financials: Q3 2025 revenue $4.1M, 69% gross margins, $11.4M unrestricted cash, market cap $2.2M (below book value $4.3M [2]).

- Market: Global simulator market $1.9B-$2.2B (2025) with 9-11% CAGR [3]; urban segment is a key growth driver.

- Product: Compact simulators (residential $6.995k-$24k [1], commercial custom pricing [0]) with AI integration [4].

- Competitive: TRUG holds ~5-7% market share [4], competing via compact footprint and software ecosystem [1].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.