Analysis of Driving Factors and Market Impact for Zhongsheng Pharmaceutical (002317) Limit-Up

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

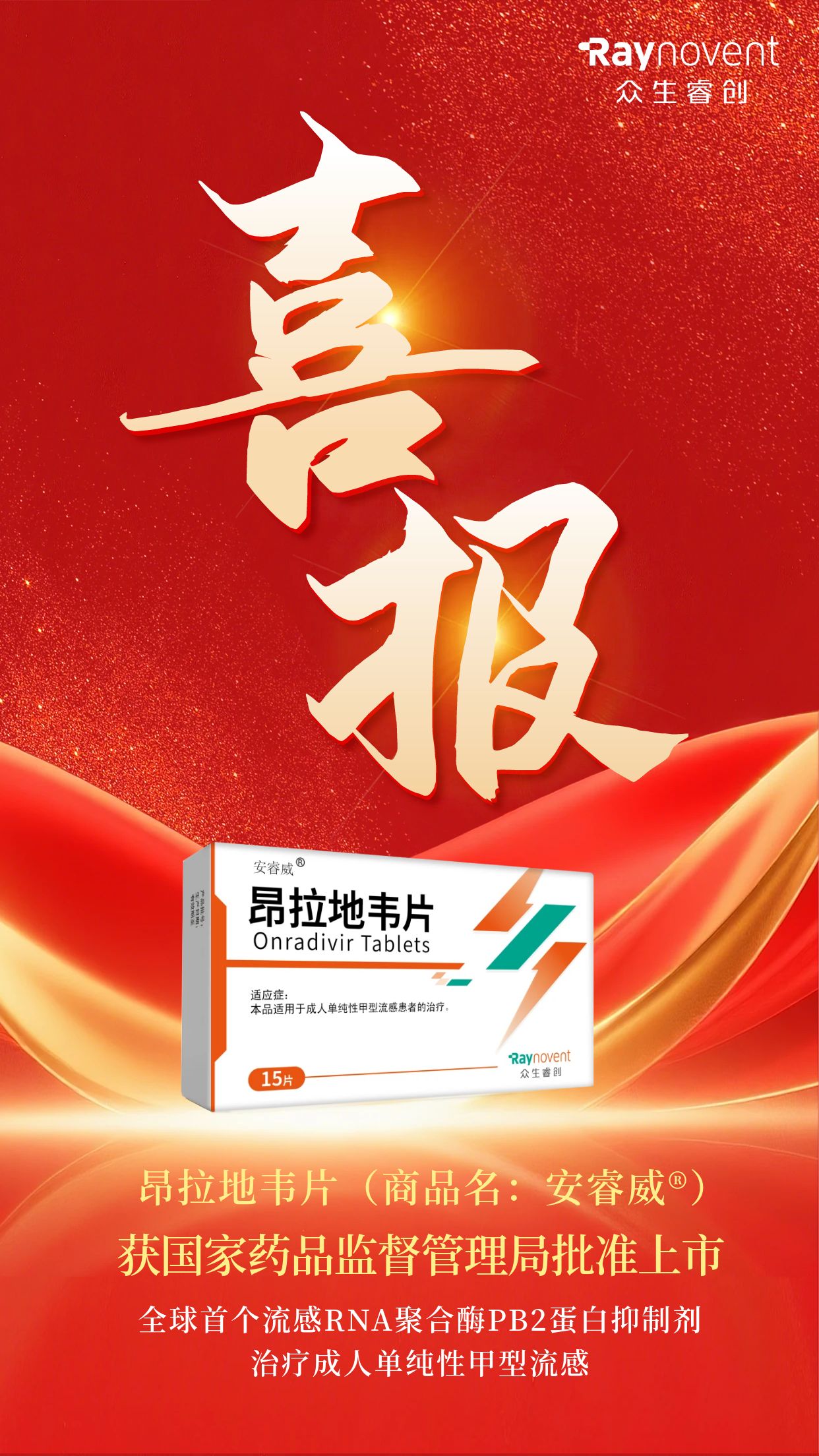

This analysis is based on the event that Zhongsheng Pharmaceutical (002317) entered the limit-up pool released by tushare_zt_pool [0] on November 17, 2025. Key points include: the company’s innovative drug Angladivir Tablets was approved (the world’s first influenza RNA polymerase PB2 inhibitor), a 68.4% year-on-year increase in net profit for the first three quarters of 2025, a net purchase of 585 million yuan by main funds on November 14 [1], and a cumulative increase of over 22% in the past three days. Key findings: unanimous buy ratings from 5 institutions, and favorable industry policies supporting the innovative drug sector. Main impacts: the company’s market value rose to 22.1 billion yuan, driving sentiment in the pharmaceutical sector.

The recent strong stock performance of Zhongsheng Pharmaceutical stems from the superposition of multiple driving factors:

- Innovative Drug Breakthrough: Angladivir Tablets was approved for marketing, filling the gap in the global influenza treatment field and becoming the company’s core growth engine. Meanwhile, multiple research projects (pediatric influenza, obesity/diabetes treatment) have entered Phase III clinical trials, with a complete pipeline layout.

- Outstanding Performance: Revenue in the first three quarters of 2025 was 1.889 billion yuan (slightly down 1.01% year-on-year), but net profit attributable to shareholders was 251 million yuan (up 68.4% year-on-year), and non-net profit increased by 30.36%, indicating improved profitability.

- Capital Inflow: On November 14, main funds had a single-day net purchase of 585 million yuan [1], accounting for 28.81% of total turnover, with a turnover rate of 10.39%, indicating high market capital attention.

- Industry Policy: The SW Pharmaceutical Index has risen 18.2% since the beginning of the year, and the innovative drug sector has continued to strengthen due to favorable policies (such as the release of innovative drug results in Shenzhen [6]).

- Technology and Market Resonance: The technical barrier of the world’s first PB2 inhibitor combined with the arrival of the flu season forms a resonance effect between product market demand and stock prices.

- Consensus between Institutions and Retail Investors: Unanimous buy ratings from 5 institutions (target average price of 20.97 yuan) and large inflows of main funds indicate a consensus among institutions and market funds on the company’s prospects.

- Industry Spillover Effect: The limit-up of Zhongsheng Pharmaceutical has driven sentiment in the innovative drug sector, and the Hong Kong Stock Exchange Pharmaceutical ETF (159718) has active trading [6], reflecting sector linkage.

- Clinical Uncertainty: The progress of clinical trials and review results of research projects (such as obesity/diabetes treatment) are uncertain [3], which may affect future performance expectations.

- Short-term Volatility Risk: A cumulative increase of over 22% in the past three days has short-term profit-taking pressure, and the company has issued an announcement on abnormal stock trading fluctuations [5].

- Market Competition: The influenza treatment field may face competition from subsequent similar drugs, so continuous attention to changes in product market share is needed.

- Product Commercialization: As the world’s first PB2 inhibitor, Angladivir Tablets is expected to quickly occupy the high-end influenza treatment market, bringing significant revenue growth.

- Pipeline Value: If multiple Phase III clinical projects succeed, they will further enrich the product matrix and enhance the company’s long-term valuation.

- Policy Dividends: The innovative drug industry continues to receive policy support, and the company is expected to enjoy dividends such as R&D subsidies and rapid approval.

The limit-up of Zhongsheng Pharmaceutical is the result of multiple factors including innovative drug breakthroughs, performance improvement, capital inflows, and industry policies. The company has established technical advantages in the influenza treatment field, but clinical uncertainty and short-term market fluctuations need to be vigilant. Investors should make decisions based on their own risk preferences, combined with the company’s long-term development prospects and short-term market sentiment.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.