Reddit (RDDT) Valuation Analysis: Strong Growth vs. Premium Pricing

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Reddit community sentiment is largely bullish on RDDT’s long-term prospects despite recent volatility:

-

Strong Bullish Consensus: Many users view RDDT as significantly undervalued long-term, citing improving ad targeting capabilities, 75% growth in advertisers, and rising average revenue per user (ARPU) Reddit

-

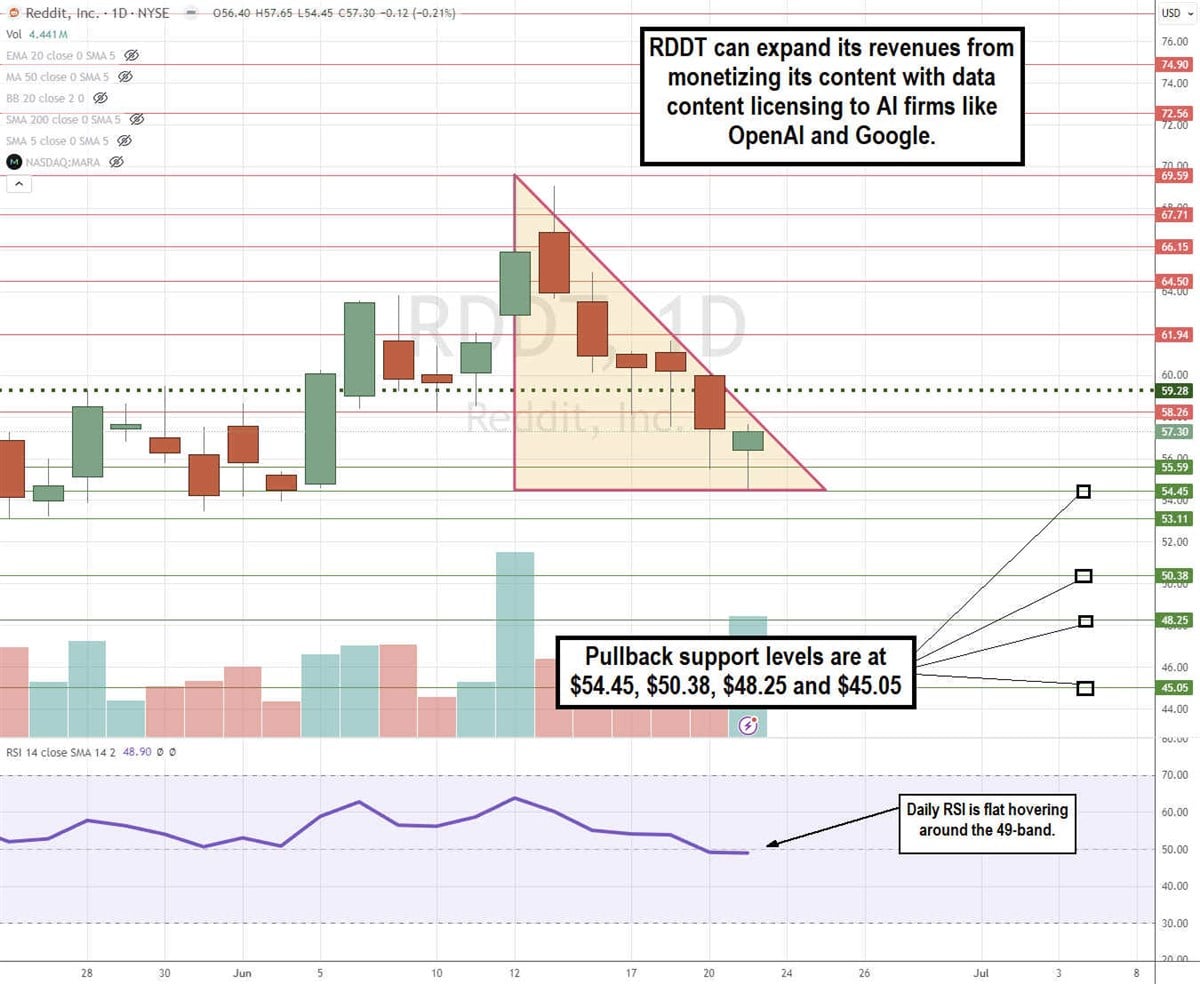

Growth Catalysts: Comments highlight Reddit’s unique demand-capture model versus demand-creation platforms like Meta, high user trust for product recommendations, and emerging AI data licensing revenue streams Reddit

-

Technical Views: Several users note a cup-and-handle formation with support around $188 and resistance near $300, advocating for buying dips under $200 Reddit

-

Valuation Debate: While some argue forward PE ~60x with high growth justifies current pricing, others note high TTM PE (109x) and call it overvalued based on traditional metrics Reddit

- Q3 2024 revenue of $585 million (+67.9% YoY) vs $546.65M expected

- Q3 2024 EPS of $0.80 (+400% beat) vs $0.50 expected The Globe and Mail

- Q4 2025 revenue guidance: $655-665 million (53-55% YoY growth) with 42% adjusted EBITDA margin

- Full-year 2025 analyst estimates: $2.14B revenue, $2.34 EPS

- Net margin: 18.33%, ROE: 15.55%

- P/E ratio of 113.4x-120.20x, significantly above market average of 38.83x Simply Wall St

- Analyst consensus price target of $217.50 represents only 1.96% upside from current $208 levels Yahoo Finance

- Simply Wall St analysis suggests Reddit is 24.9% overvalued with fair value below current share price Simply Wall St

- Consensus rating is “Moderate Buy” with 14 buy, 10 hold, 2 sell, and 2 strong buy ratings from 28 analysts MarketBeat

The Reddit community and traditional analysis present conflicting views on RDDT’s valuation:

- Strong earnings performance and growth trajectory are undisputed

- Company has successfully achieved profitability with robust margins

- Long-term growth potential through AI and advertising improvements is recognized

- Reddit users focus on growth potential and moat strength, justifying premium valuation

- Traditional metrics highlight extreme valuation multiples suggesting limited near-term upside

- Community sees dips as buying opportunities, while analysts see current pricing as fair to slightly overvalued

The disconnect suggests RDDT may be in a “growth stock premium” phase where traditional valuation metrics are less relevant. The stock appears suitable for growth-focused investors willing to pay premium multiples for continued expansion, but value investors may find better opportunities elsewhere.

- Potential S&P 500 inclusion could drive institutional demand Reddit

- AI data licensing represents emerging revenue stream

- Continued improvement in ad targeting and monetization

- Strong user engagement and trust for product recommendations

- User base aversion to advertising could limit monetization potential Reddit

- Bot-driven engagement questions may impact advertiser confidence

- Potential regulatory scrutiny on content moderation

- Declining daily active user growth rates Reddit

- High valuation multiples create vulnerability to growth disappointments

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.