Brokerage Firm Compliance Issues with Stepped-Up Cost Basis for Inherited Securities

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on a Reddit discussion [1] from November 13, 2025, where a user reported that their brokerage firm failed to provide a stepped-up cost basis for inherited stocks, creating concerns about IRS reporting and tax return compliance.

The stepped-up basis provision is a critical tax mechanism that adjusts inherited assets’ cost basis to their fair market value on the date of the previous owner’s death [2]. This adjustment is essential because the cost basis determines capital gains taxes owed when the asset is eventually sold [2]. When someone inherits capital assets such as stocks, the IRS “steps up” the cost basis to the asset’s value when inherited [3], potentially eliminating years of accumulated capital gains from tax liability.

The issue arises from brokerage reporting requirements. Brokerage firms must report securities transactions on Form 1099-B, which includes cost basis information for “covered securities” [4]. However, complications frequently occur with inherited assets, as brokers may not automatically apply stepped-up basis without proper documentation [5]. If the basis shown on Form 1099-B is incorrect, taxpayers must take corrective action through specific IRS procedures [6].

- Documentation required includes death certificates, estate valuation documents, and proof of inheritance relationship

- Fair market value must be determined as of the date of death (or alternate valuation date up to 6 months later if estate tax return filed) [6]

- Taxpayers must ensure correct basis reporting regardless of broker errors [8]

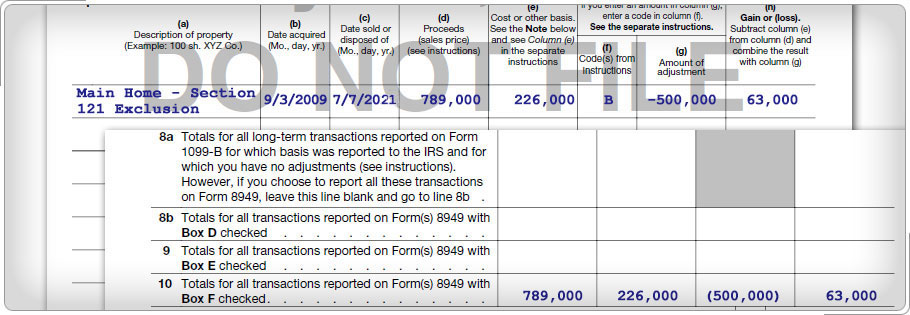

- Use Form 8949 for reporting sales with basis discrepancies

- Check Box B when basis wasn’t reported to the IRS

- Enter correct stepped-up basis and make appropriate adjustments in column (g)

- Maintain supporting documentation for basis calculations

- Many brokerages require formal requests with supporting documentation

- Some firms have specific forms or procedures for inherited securities

- Response times vary significantly between firms

- Escalation may be necessary for complex cases

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.