Analysis of the Impact of Accelerated Tesla AI Chip Iteration on FSD Competitiveness and Corporate Valuation

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on collected data and market information, I have prepared this in-depth analysis report for you.

On January 17, 2026, Tesla CEO Elon Musk announced on social media platform X that the design work for the company’s next-generation AI5 chip (Hardware 5) is nearly complete, while the next-generation AI6 chip has entered the early development stage [1]. More importantly, Musk revealed that Tesla plans to use a

This strategic layout marks Tesla’s complete transformation from early reliance on external chip suppliers (such as NVIDIA) to an

| Chip Generation | Performance Improvement | Expected Mass Production Time | Core Positioning |

|---|---|---|---|

AI4 |

Baseline Version | 2024-2025 | Current FSD Hardware Foundation |

AI5 |

50x the performance of AI4 [1] | Small-scale trial production in late 2026, mass production in 2027 | High-level Autonomous Driving, Robotaxi |

AI6 |

Further improvement over AI5 (early design phase) | 2028 and beyond | Next-generation Robotics and AI Democratization |

Tesla’s mixed-precision architecture (FP16/BFLOAT16/INT8) delivers

The traditional automotive chip design cycle is typically

- Rapid Iteration Capability: Accelerates closed-loop optimization of software-defined hardware, enabling collaborative evolution of FSD algorithms and chip hardware

- Cost Control Advantage: Shortening the R&D cycle means lower labor and time costs

- Catching Up with Moore’s Law: Beyond advanced manufacturing processes (3nm/2nm), achieve exponential performance improvement through architectural innovation

Tesla has currently deployed

- More Complex Real-Time Environmental Perception: The 50x performance leap means it can process higher-resolution sensor data (lidar redundancy solution, 4D millimeter-wave radar fusion)

- Improved End-to-End Learning Efficiency: Massive corner case data can be processed for rapid inference and model fine-tuning on the vehicle end

- Unlocking the Value of ‘Shadow Mode’: Vehicles can continuously compare autonomous driving decisions during human operation, accumulating high-quality training samples

Current FSD pricing is a one-time purchase of

| Cost Component | Traditional Solution (Purchased from NVIDIA) | Tesla’s Independent Development Solution |

|---|---|---|

| Single Chip Cost | H100 is approximately $30,000 | Expected $3,000 (90% reduction) |

| Supply Chain Bargaining Power | Dependent on external supply cycles | Vertically integrated, dual supply from TSMC/Samsung |

| Diminishing Marginal Costs | Linearly decreases with scale | Exponentially decreases after R&D cost amortization |

Waymo provided

- No In-Vehicle Safety Officer Required: Sufficient computing power redundancy to support Level 4 decision-making

- Full Scenario Coverage: Expansion from highway loops to complex urban road conditions

- Accelerated Regulatory Compliance: High-performance on-vehicle computing reduces reliance on the cloud and lowers the risk of communication latency

However, the following challenges require careful assessment:

- Waymo’s First-Mover Advantage: As of 2025, it has provided a cumulative total of20 million fully autonomous rides[5], leading in operational experience and regulatory trust

- Uncertainty in Technology Roadmap: If regulation tightens or safety incidents occur, it may delay the realization of value from FSD iteration

- Competitor Follow-Up: BYD DiPilot, Baidu Apollo, etc. are accelerating independent development of high-level intelligent driving chips

Tesla’s current market capitalization is

| Valuation Component | Implied Value | Key Driver |

|---|---|---|

| Automotive Business | ~60% | Q3 2025 revenue of $28.1 billion |

| FSD/Robotics Business | ~25% | AI chips + software subscription revenue potential |

| Energy Storage | ~10% | 46.7 GWh deployed in 2025 (YoY +49%) |

| Other (Robotics, etc.) | ~5% | Long-term expectations for Optimus |

Notably, Tesla’s current

Accelerated AI chip iteration can reshape valuation from the following dimensions:

- FSD Subscription Revenue: Assuming FSD penetration reaches 30% in 2030 (current ~10%), annual subscription revenue can reach $20 billion

- Robotaxi Revenue Sharing: If 1 million Robotaxis are in operation, with an average annual income of $30,000 per vehicle and Tesla taking a 20% cut, corresponding revenue will be $6 billion

- Chip External Sales: Supplying to third-party robotics manufacturers, referencing NVIDIA’s data center business model

- Slow FSD penetration, moderate growth in subscription revenue

- Robotaxi cannot be scaled until after 2028

- High costs during chip production capacity ramp-up

| Institution | Rating | Target Price | Core View |

|---|---|---|---|

| Wedbush Securities | Buy | $600 (highest) [5] | Optimistic about Robotaxi’s 30-city coverage plan |

| UBS | Sell | $300 | Questions growth momentum of automotive sales |

| Baird | Buy | $550 | Optimistic about synergy between energy business and AI |

Current analyst consensus is

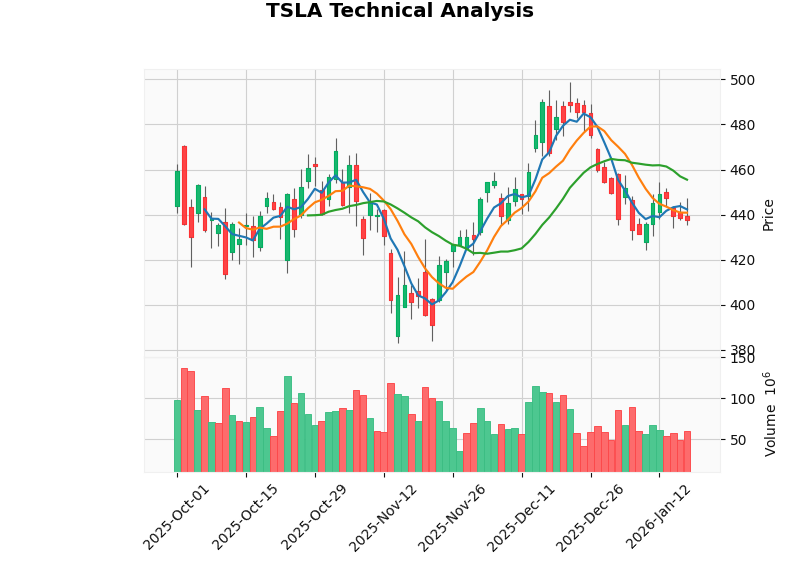

Based on technical analysis tool data [7]:

| Indicator | Value | Signal Interpretation |

|---|---|---|

| Stock Price | $437.50 | In a medium-term sideways trading range |

| Support Level | $430.05 | Short-term critical support |

| Resistance Level | $455.48 | Upper edge of the upward channel |

| MACD | No crossover | No clear trend signal for now |

| KDJ | K=44.6, D=41.3 | Bullish in the short term but needs confirmation |

| Beta | 1.83 | Higher volatility than the broader market |

The current stock price is oscillating between $430 and $455, waiting for

| Dimension | Score (1-5) |

|---|---|

| AI Chip Technology Leadership | ★★★★★ |

| FSD Commercialization Certainty | ★★★☆☆ |

| Valuation Rationality | ★★☆☆☆ |

| Short-term Catalyst | ★★★☆☆ |

| Long-term Growth Potential | ★★★★★ |

- Mass Production Schedule Risk: If AI5 is delayed to after 2028, competitors may narrow the gap

- Macroeconomic Risk: High interest rate environment suppresses demand for high-end electric vehicles, affecting cash flow

- Regulatory Risk: FSD safety incidents may lead to regulatory tightening and function restrictions

- Valuation Pullback Risk: If FSD penetration falls short of expectations, the current 268x P/E ratio has room for downward revision

Tesla’s strategic layout of a 9-month AI chip iteration cycle has fundamentally reshaped the competitive landscape of the autonomous driving industry. The

From a valuation perspective, independent AI chip development is the

Current market pricing has partially reflected the positive impact of AI chips, but has not yet fully priced in the revenue increment after Robotaxi large-scale deployment. It is recommended that investors keep track of AI5 mass production progress and FSD function iteration, and deploy positions during appropriate valuation windows.

[1] The Driven - “Elon Musk says Tesla AI 5 chip design ‘almost done’, with 50x more performance” (https://thedriven.io/2026/01/18/elon-musk-says-tesla-ai-5-chip-design-almost-done-with-50x-more-performance/)

[2] AInvest - “Tesla’s Mixed-Precision AI Architecture: A Game-Changer for Edge AI and Robotics” (https://www.ainvest.com/news/tesla-mixed-precision-ai-architecture-game-changer-edge-ai-robotics-2601/)

[3] PatentPC - “Tesla vs. Waymo vs. Cruise: Who’s Leading the Autonomous Vehicle Race” (https://patentpc.com/blog/tesla-vs-waymo-vs-cruise-whos-leading-the-autonomous-vehicle-race-market-share-stats)

[4] PatentPC - “Tesla FSD Pricing Model Analysis” (https://patentpc.com/blog/tesla-vs-waymo-vs-cruise-whos-leading-the-autonomous-vehicle-race-market-share-stats)

[5] CNN Business - “Tesla’s profit engine is sputtering. Elon Musk has bet its future on Robotaxi” (https://www.cnn.com/2026/01/13/business/tesla-robotaxi-musk-2026)

[6] JINLING API - Tesla Company Profile and Financial Data

[7] JINLING API - Tesla Technical Analysis Data

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.