Analysis Report on Industrial Chain Advantages and Sustainability of Dingtai Hi-Tech (301377)

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on the collected information, I will provide you with an in-depth analysis report on the industrial chain advantages of Dingtai Hi-Tech.

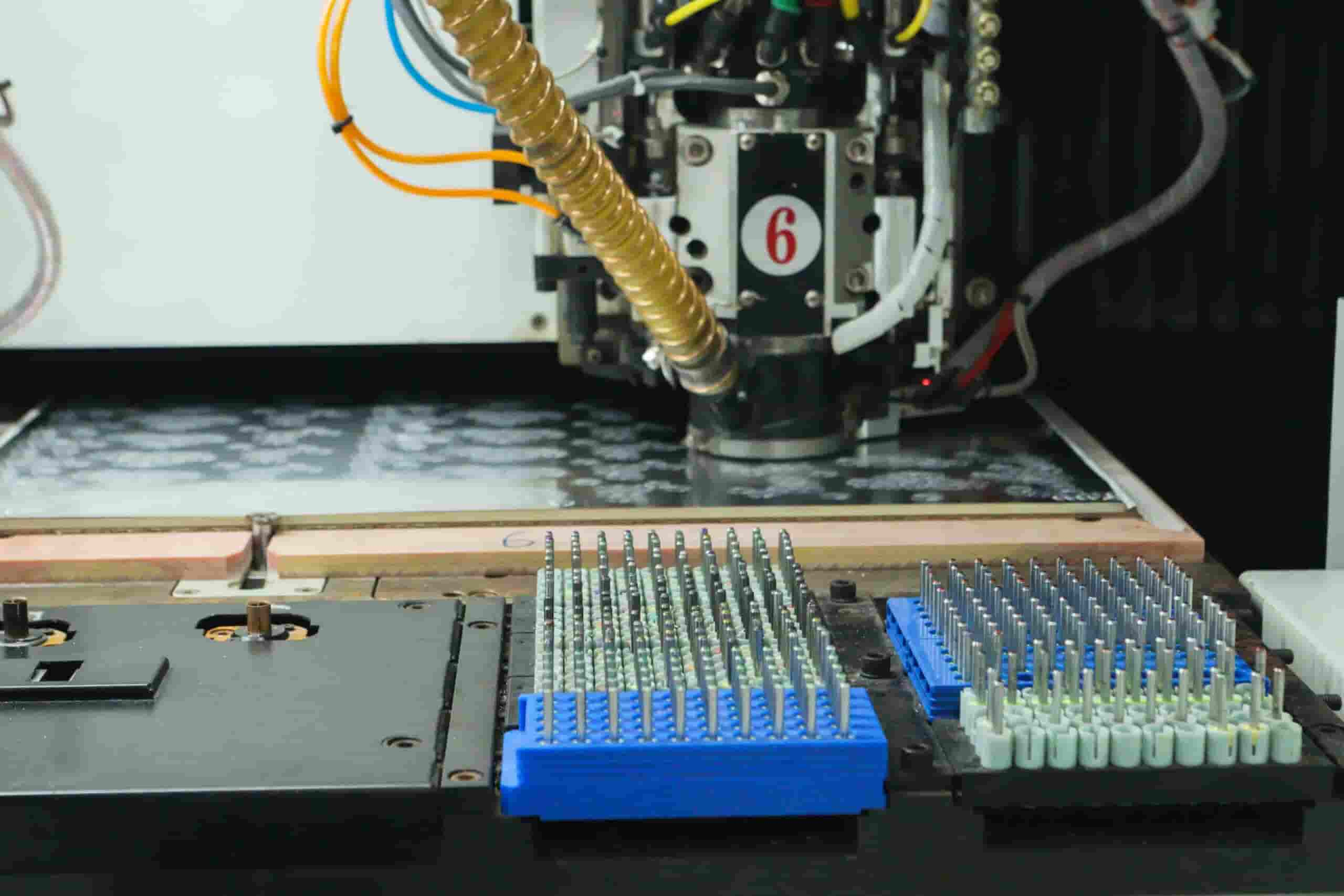

Dingtai Hi-Tech was founded in 2013, with its headquarters in Dongguan City, Guangdong Province. It is a world-leading supplier of PCB (Printed Circuit Board) drill bits. The company is listed on the ChiNext Board of the Shenzhen Stock Exchange, with stock code 301377. Its product portfolio includes PCB drill bits, milling cutters, brush wheels, automated equipment, industrial film products, CNC tools, and surface coatings, forming a complete integrated industrial chain system covering tools, materials, and equipment.

Dingtai Hi-Tech independently develops PCB tool production equipment such as high-precision multi-station grinding machines through its subsidiary Dingtai Robotics, and holds patent technologies for relevant software and hardware. According to public information, the

| Cost Component | Self-Developed Equipment | Imported Equipment | Cost Savings |

|---|---|---|---|

| Equipment Procurement Cost | 1/3 | 1 (Benchmark) | ~66% |

| Maintenance Cost | Lower | Higher (including premium for imported parts) | Significant |

| Spare Parts Supply Cycle | Fast response | Longer (dependent on imports) | Time cost savings |

| Technical Support Response | Localized service | Cross-border service | Efficiency improvement |

Self-developed equipment not only reduces procurement costs, but also brings significant improvements in production efficiency and yield rate:

-

Precise Process Control: With an in-depth understanding of the production process and key control nodes, the company can accurately use and adjust equipment parameters to achieve refined machine control, thereby significantly optimizing the product production process[1].

-

Higher Yield Rate: The high compatibility between self-developed equipment and production processes results in a significantly higher product yield rate compared to competitors using imported equipment.

-

Market Response Efficiency: Localized equipment greatly shortens the cycles of equipment debugging, fault response, and product iteration, improving market response speed and flexibility in capacity expansion[1].

The company’s 2025 performance forecast shows that it expects to achieve a net profit attributable to parent shareholders of RMB 410-460 million, representing a year-on-year increase of 80.72%-102.76%, and a non-recurring net profit increase of 88.16%-112.91% year-on-year[3][4]. This growth mainly benefits from:

- Surge in AI Server Demand: Global AI server shipments are expected to grow from 2 million units in 2024 to 5.4 million units in 2029, with a compound annual growth rate (CAGR) of 21.7%[5].

- Upgrade of PCB Thickness: AI servers have continuously increasing requirements for PCB thickness. An 8mm thick PCB requires 4 drill bits with different length-diameter ratios compared to a 3mm thick PCB, increasing the cost per hole by dozens of times[2].

- Upgrade of High-End Materials: Interlayer materials are being upgraded to M9 grade (with silica content of 99.99%), which accelerates the wear rate of drill bits and further increases replacement demand[2].

- Continuous Increase in R&D Investment: The company’s R&D expenditure increased from RMB 79.817 million in 2022 to RMB 110 million in 2024, accounting for 6.5%-7.5% of its revenue[5].

- Accumulation of Patent Technologies: The company holds independent intellectual property rights for equipment software and hardware, forming a technical moat.

- Breakthroughs in Coating Technologies: The company has independently developed various coating technologies such as CVD coatings, PVD hard coatings, and Ta-C lubricating coatings, and has achieved large-scale mass production of coating processing, forming a differentiated competitive advantage[1].

- Overseas Capacity Expansion: The company’s Thai subsidiary has achieved mass production, with an initial monthly PCB drill bit capacity of 15 million units; in 2025, it acquired assets of Germany’s MPK Kemmer to accelerate expansion into the European market[5].

- Construction of Global Network: The company plans to further increase investment in Asia and Europe to build a global operation network covering “R&D - Production - Sales - Service”.

Other competitors in the industry (such as Jinzhou Seiko, Japan’s Uniloy, and Jiandian Technology) may increase R&D investment to narrow the technological gap. In particular, imported equipment suppliers such as Switzerland’s Romantik may launch more cost-effective products.

The PCB industry is cyclical. If the progress of AI computing power construction falls short of expectations, or if downstream consumer electronics demand remains weak, it may affect the company’s performance growth[2].

PCB drill bits use tungsten carbide and cobalt powder as basic raw materials, and fluctuations in raw material prices may affect the company’s profitability.

The procurement of imported equipment and raw materials involves foreign currency settlement, and exchange rate fluctuations may affect the cost structure.

| Advantage Dimension | Short-term (1-2 years) | Medium-term (3-5 years) | Long-term (Over 5 years) |

|---|---|---|---|

| Cost Advantage | ★★★★★ Strong | ★★★★☆ Relatively Strong | ★★★☆☆ Moderate |

| Technical Barriers | ★★★★★ Strong | ★★★★☆ Relatively Strong | ★★★☆☆ Requires continuous investment |

| Market Share | ★★★★★ Top position maintained | ★★★★★ Further improvement | ★★★★☆ Leading position maintained |

| Customer Stickiness | ★★★★★ Strong | ★★★★☆ Relatively Strong | ★★★★☆ Relatively Strong |

- High-Quality Track: The construction of AI computing power drives a surge in PCB demand, and as a global leader, the company directly benefits from the simultaneous increase in industry volume and price.

- Significant Cost Advantage: The cost of self-developed equipment is only 1/3 that of imported equipment, forming a long-term cost moat.

- Broad Growth Space: The net profit attributable to parent shareholders is expected to reach RMB 440 million, RMB 810 million, and RMB 1.57 billion in 2025-2027 respectively, with a high compound growth rate[4].

- Global Layout: Overseas capacity expansion and acquisition actions are accelerating, opening up incremental market space.

- AI computing power construction falls short of expectations

- R&D progress of high length-diameter ratio drill bits falls short of expectations

- Macroeconomic risks

- Sharp fluctuations in raw material prices

- Risk of exchange rate fluctuations

The cost advantage of Dingtai Hi-Tech’s self-developed equipment has strong sustainability, mainly based on the following judgments:

- Deep Technical Accumulation: The company has been deeply engaged in the PCB tool field for over 30 years, with profound technical accumulation, which is difficult for competitors to replicate in the short term.

- Continuous R&D Investment: Maintaining an R&D investment intensity of 6.5%-7.5% to ensure the sustainability of technological leading advantages.

- Structural Upgrade of AI Demand: The growth in demand for high-end PCBs has structural characteristics rather than cyclical fluctuations, providing long-term growth momentum for the company.

- Industrial Chain Synergy Effect: The company has formed an integrated layout of tools, materials, and equipment, with obvious industrial chain synergy advantages.

- Technology catch-up progress of competitors

- Changes in supply and demand pattern due to industry capacity expansion

- Fluctuations in raw material costs and exchange rates

Overall, Dingtai Hi-Tech’s industrial chain advantages have strong sustainability in the medium term. The company is expected to continue to benefit from the improvement in the prosperity of the PCB industry driven by AI computing power construction, relying on its technological, cost, and first-mover market advantages.

[1] Tianfeng Securities Research Institute - Initial Coverage Report on Dingtai Hi-Tech (301377) (http://pdf.dfcfw.com/pdf/H3_AP202411291641110991_1.pdf)

[2] Soochow Securities Research Institute - In-Depth Research on Dingtai Hi-Tech: Computing Power Construction Drives Surge in PCB Processing Demand (https://pdf.dfcfw.com/pdf/H3_AP202512011791944813_1.pdf)

[3] Securities Times - Multiple A-Share Companies Expect Significant Net Profit Growth in 2025 (https://www.stcn.com/article/detail/3572609.html)

[4] Sina Finance - Commentary on Dingtai Hi-Tech’s 2025 Annual Report Performance Forecast (https://finance.sina.com.cn/roll/2026-01-06/doc-inhfkskm5476519.shtml)

[5] Dingtai Hi-Tech HKEX Filing Materials (https://www.hafoo.com.hk/news/hant/notice/202512013579355345)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.