U.S. Labor Market Persistent Softening: Job Openings Near Five-Year Lows

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

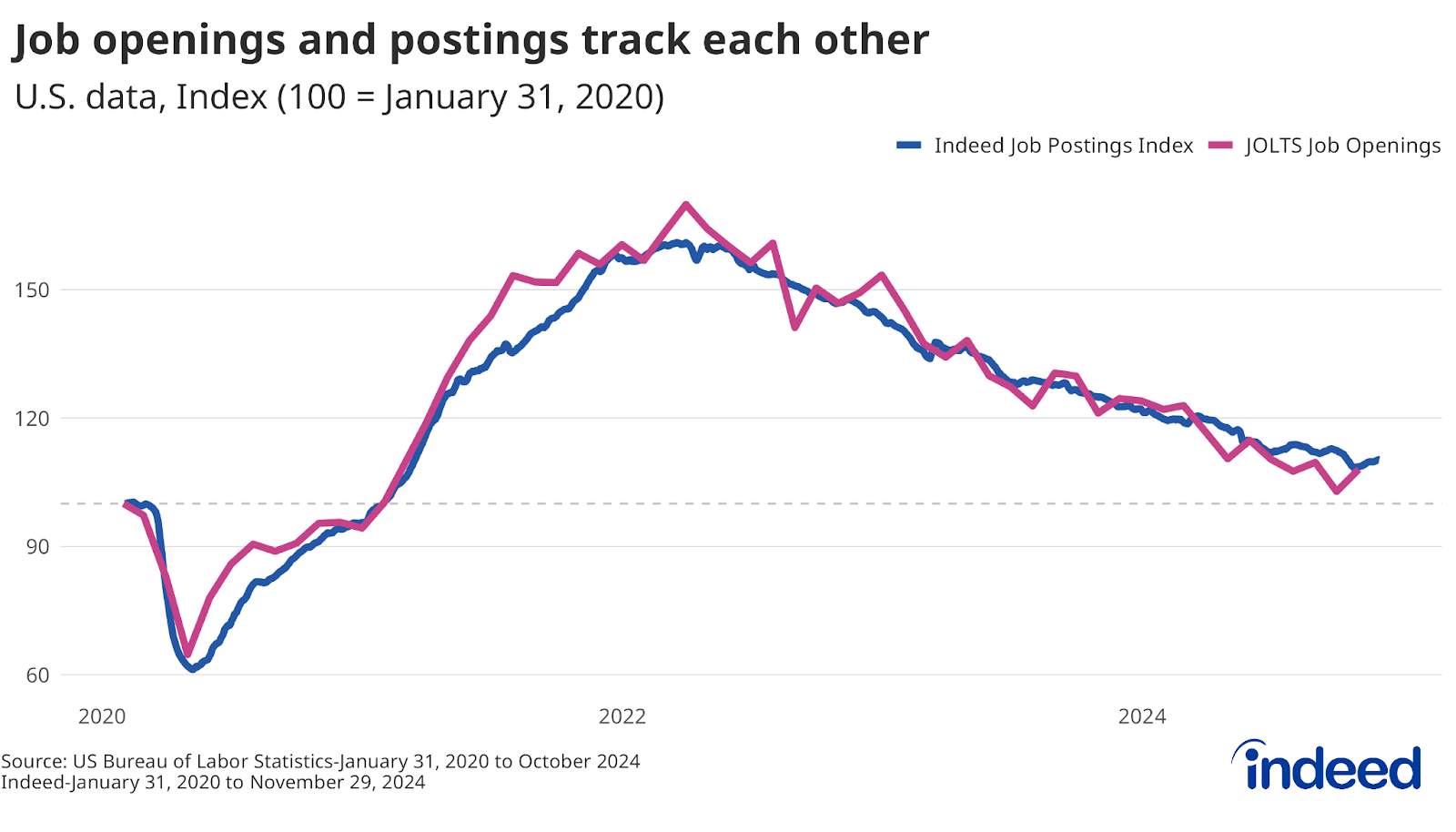

This analysis is based on the MarketWatch report published on January 7, 2026, which reported that U.S. job openings remain stuck near five-year lows, with the economy “barely adding new workers” as job creation is nearly offset by job destruction [1]. The November 2025 JOLTS (Job Openings and Labor Turnover Survey) data, released by the Bureau of Labor Statistics, shows job openings holding at approximately 7.67 million—significantly below the post-pandemic peak above 10 million and approaching levels last seen in 2020-2021 [1][2][3]. Market reaction has been measured, with major indices showing mixed performance: the S&P 500 and NASDAQ registering modest gains while the Dow Jones and Russell 2000 declined, suggesting investor caution without panic [0]. The data aligns with Indeed Hiring Lab’s characterization of a “low-hire, low-fire” environment that signals economic stabilization without robust momentum [4].

The November 2025 JOLTS report reveals a labor market characterized by equilibrium rather than expansion. Job openings have remained persistently in the high-7-million range, representing a substantial decline from the elevated levels observed during the post-pandemic recovery period [2][3]. The Bureau of Labor Statistics characterized October job openings as “unchanged at 7.7 million” with both hires and total separations showing minimal change, suggesting a labor market that has reached a steady-state condition [3].

The near-parity between hires and separations—each running at approximately 5.1 million—indicates that the economy is creating roughly as many jobs as it is destroying [1]. This dynamic explains MarketWatch’s characterization that the economy is “barely adding new workers,” as net job creation, while positive, lacks the acceleration that would signal robust economic growth. The job openings rate has stabilized around 4.6%, which, while healthy by historical standards, represents a significant moderation from the 6-7% rates seen during the 2021-2022 period [3].

The equity market’s response to the JOLTS data reflects a nuanced investor perspective [0]. The S&P 500’s marginal gain of 0.08% and the NASDAQ’s more pronounced 0.42% advance suggest that market participants are processing the labor data without dramatic repricing. However, the Dow Jones’ 0.52% decline and the Russell 2000’s 0.62% drop merit closer examination [0].

The divergence between large-cap indices (S&P 500, NASDAQ) and small-cap indices (Russell 2000) is particularly noteworthy. Small-cap companies tend to be more sensitive to domestic economic conditions and labor market dynamics, as they often have narrower profit margins and greater reliance on consumer spending. The Russell 2000’s underperformance may indicate investor concern about smaller companies’ ability to navigate an environment of constrained hiring and potentially softening consumer demand [0].

The labor market data carries significant implications for Federal Reserve monetary policy [4]. The “low-hire, low-fire” environment described by Indeed Hiring Lab suggests economic stabilization without the inflationary pressures that typically concern central bankers [4]. This alignment supports expectations for continued rate normalization at upcoming Federal Open Market Committee meetings, particularly the January 28-29, 2026 gathering.

The relationship between labor market conditions and Fed policy operates through multiple channels. First, softening labor markets reduce upward pressure on wages, which in turn moderates services inflation—a key component of the Fed’s preferred inflation measures. Second, a balanced labor market with minimal net hiring suggests that the economy may be operating below its maximum sustainable growth rate, providing room for accommodative policy. Third, the Fed has explicitly stated its intention to respond to softening labor conditions as part of its dual mandate, making the JOLTS data a direct input into policy deliberations [4].

The most significant insight from the JOLTS data is the emergence of what labor economists describe as a “low-hire, low-fire” equilibrium [4]. This environment is characterized by minimal net job creation despite continued economic activity, reflecting a period of organizational optimization following the pandemic-era hiring surge. Companies appear to have adjusted their workforce levels to match current demand conditions, reducing both aggressive hiring and significant layoffs.

This equilibrium presents both opportunities and risks. On the opportunity side, the absence of significant job losses suggests corporate resilience and avoids the negative feedback loops that can develop when rising unemployment depresses consumer spending. On the risk side, the lack of hiring momentum may indicate corporate uncertainty about the economic outlook or structural changes in labor demand that reduce the need for additional workers.

The Russell 2000’s underperformance relative to large-cap indices warrants attention as a potential leading indicator [0]. Historically, small-cap equities have served as bellwethers for domestic economic health due to their concentrated exposure to U.S. consumer spending and their relative insulation from international revenue streams that can benefit large multinational corporations. The 0.62% decline in the Russell 2000, while not catastrophic, suggests that market participants perceive elevated risk in smaller companies’ prospects amid softening labor markets [0].

This small-cap weakness could reflect several underlying concerns. First, smaller companies may face higher financing costs that become more burdensome as interest rates remain elevated. Second, reduced hiring may constrain small-cap revenue growth, as these companies often depend on labor force expansion to drive output. Third, the “low-hire, low-fire” environment may be more acutely felt in small-cap sectors that depend on labor-intensive business models.

The labor market dynamics suggest a continuation of wage growth moderation [3]. The quits rate—a measure of worker confidence in finding alternative employment—has declined from post-pandemic peaks, indicating reduced worker bargaining power. This development carries implications for consumer spending, as wage growth directly influences household income and, consequently, consumption patterns. The expected moderation in wage growth may contribute to a more gradual trajectory for consumer spending, potentially affecting retail and consumer discretionary sectors.

The analysis reveals several risk factors that warrant monitoring. The labor market balance risk is evident in the “low-hire, low-fire” environment, which suggests economic momentum is waning without reaching crisis levels—a subtle but concerning trend that could indicate underlying weakness in aggregate demand [4]. This subtleness is particularly important because it may not trigger the same policy response as more acute economic distress.

Small-cap vulnerability represents a second significant risk factor, as the Russell 2000’s decline may indicate investor concern about smaller companies’ ability to navigate softening labor market conditions [0]. This risk is particularly relevant for portfolios with concentrated small-cap exposure, as sector-specific weakness could produce meaningful underperformance.

Wage pressure risk manifests through the relationship between labor market conditions and consumer spending. With quits rates declining and hiring slowing, wage growth moderation is expected, potentially creating a feedback loop where reduced consumer spending leads to further hiring restraint [3]. This dynamic could become self-reinforcing if not offset by other economic factors.

The labor market data also presents opportunity windows for various stakeholders. For the Federal Reserve, the evidence supports a gradual approach to rate normalization, potentially extending the economic expansion by maintaining accommodative financial conditions [4]. This policy trajectory could provide support for equity valuations, particularly in interest-rate-sensitive sectors.

For employers, the current labor market environment offers opportunities to optimize workforce composition without the aggressive cost-cutting measures that would be required in a more severe downturn. The “low-hire, low-fire” equilibrium allows companies to improve productivity and adjust compensation structures while maintaining workforce stability.

For workers, the data suggests a period of job security without significant wage acceleration. While this may represent a reduction in bargaining power compared to the post-pandemic period, the absence of significant layoffs provides stability that has been absent in previous economic transitions.

The labor market data carries elevated short-term time sensitivity due to several upcoming events. The December 2025 Employment Situation report, scheduled for January 9, 2026, will provide critical confirmation of labor trend trajectories [2]. The January 27-29, 2026 FOMC meeting will incorporate the JOLTS data and subsequent employment reports into policy decisions [2]. Additionally, state-level JOLTS data releasing January 27, 2026, will offer insights into regional labor market variations that may not be apparent in national aggregates [2].

The November 2025 JOLTS data indicates that U.S. job openings remain near five-year lows at approximately 7.67 million, with hiring and separations in rough equilibrium at roughly 5.1 million each [1][3]. This dynamic has produced a labor market characterized by stability without expansion, with the job openings rate holding at approximately 4.6% [3]. Market reaction has been measured, with equity indices showing mixed performance that suggests caution without panic [0]. The Federal Reserve’s upcoming policy decisions will likely incorporate this data, with expectations leaning toward continued rate normalization [4]. The “low-hire, low-fire” environment described by labor economists signals a period of economic balance that merits continued monitoring for signs of either acceleration or deterioration [4].

The upcoming employment reports and Federal Reserve communications will provide additional signals about the trajectory of labor market conditions and their implications for monetary policy. Market participants should monitor these developments closely while maintaining awareness that the current data reflects stabilization rather than either robust growth or significant distress.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.