In-depth Analysis of the Impact of Pop Mart's Overseas Expansion Strategy on ROE Improvement

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

According to the latest financial data and market analysis, Pop Mart (09992.HK)'s overseas expansion strategy has had a significant positive driving effect on its Return on Equity (ROE).

Pop Mart’s ROE improvement can be broken down using the DuPont analysis as follows:

| Financial Indicator | 2024 Actual | 2025 Forecast | Change Rate |

|---|---|---|---|

| ROE | 29.26% | 46.37% | +58.5% |

| Net Profit Margin | 23.97% | 32.33% | +34.9% |

| Gross Profit Margin | 66.79% | 73.82% | +10.5% |

| Net Profit Attributable to Parent Company (100 million yuan) | 31.25 | 100.2 | +220.6% |

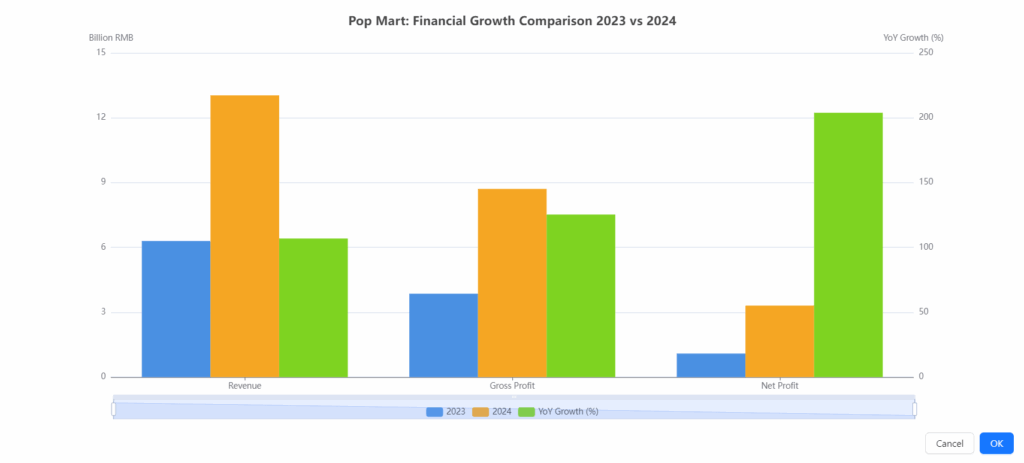

Adjusted net profit in the first half of 2025 reached 4.71 billion yuan, exceeding the full-year net profit of 2024, a year-on-year increase of 362.8%[3]. The explosive growth in net profit directly improves the return on shareholder equity.

Overseas expansion has brought significant economies of scale:

- Continuous Gross Profit Margin Improvement:It is expected to increase from 66.79% in 2024 to 74.71% in 2027, a cumulative increase of nearly 8 percentage points[1]. Higher product pricing power in overseas markets and supply chain optimization are the main drivers.

- Channel Efficiency Improvement:The number of overseas offline stores increased to 130 in 2024, and robot stores reached 192 units, with a significant increase in per-store output of retail stores[2]. Online channels also made simultaneous efforts: revenue from online channels in the Americas was 1.33 billion yuan, up 1977.4% year-on-year[3].

- Enhanced Brand Premium Capacity:Entry into global top landmarks such as the Louvre in Paris and Oxford Street in the UK has significantly improved the brand’s international image and premium capacity.

Overseas expansion has achieved global diversification of revenue sources:

| Regional Market | 2024 Revenue (100 million yuan) | YoY Growth Rate | Revenue Share |

|---|---|---|---|

| Southeast Asia | 24.0 | +619.1% | 47.4% |

| East Asia & Hong Kong, Macau, Taiwan | 13.9 | +184.6% | 27.4% |

| North America | 7.2 | +556.9% | 14.3% |

| Europe & Australia-New Zealand | 5.5 | +310.7% | 10.9% |

Regional diversification not only reduces single-market risks but also enables synergy between regions, overall improving the company’s profitability and risk resistance capabilities.

- Accelerated Store Expansion:The number of global stores reached 571 in the first half of 2025, including 41 in the Americas and 18 in Europe, a significant increase compared to the same period last year[3]

- Explosive Online Channels:Pop Mart’s official website once topped the US App Store shopping rankings, reaching nearly 100 countries and regions

- Global IP Operation:Top IPs such as The Monsters have become popular globally, with annual sales exceeding 3 billion yuan, a year-on-year increase of 726.6%[2]

- Mature Localized Operations:In April 2025, it launched a global organizational structure adjustment, establishing regional headquarters in four major global regions to achieve deeper localized operations

- Product Structure Optimization:Plush products achieved an explosive growth of 1289%, and block products sold out quickly upon their first launch; the multi-category matrix reduces dependence on a single category

- Member System Replication:The cumulative number of registered members reached 46.08 million, with members contributing 92.7% of sales and a repurchase rate of 49.4%; the overseas member system is replicating this model

Cinda Securities predicts that Pop Mart’s net profit attributable to parent company from 2025 to 2027 will reach 10.02 billion yuan, 14.93 billion yuan, and 18.12 billion yuan respectively, with corresponding ROEs of 46.37%, 39.82%, and 32.08%[1]. Although the growth rate of ROE will slow down, the absolute value will remain at a high level, reflecting the transition of overseas business from a high-growth period to a stable return period.

- Revenue Structure Optimization:The proportion of overseas revenue increased from 15.2% in 2022 to 38.9% in 2024, and it is expected to exceed 50% in 2025

- Profitability Improvement:Gross profit margin and net profit margin continue to improve, driven by scale effect and brand premium

- Operational Efficiency Improvement:Store expansion and online channel synergy improve per-store output and inventory turnover efficiency

- Policy and cultural differences in overseas markets may bring operational risks

- IP development and operation below expectations may affect growth sustainability

- Increased industry competition may compress profit margin space

[1] Cinda Securities Research Report - “Accelerated Globalization, World-Class Pop Mart” (http://testtoo1.oss-cn-hangzhou.aliyuncs.com/eastmoney_pdf/AP202508201731083127.pdf)

[2] Xinhuanet - “Pop Mart Releases 2024 Full-Year Financial Report: Revenue Exceeds 10 Billion Yuan, Net Profit Hits Record High” (http://www.news.cn/tech/20250326/76d665d54199492f8980a6f26fddd6a1/c.html)

[3] Siwei Finance - “Pop Mart Earns 4.7 Billion Yuan in Half a Year, Exceeding Last Year’s Full-Year Total; Overseas Market Layout Expands Significantly” (https://www.investorchina.cn/article/81811)

[4] Investing.com - Pop Mart (9992) Stock Quotes & Financial News (https://hk.investing.com/equities/pop-mart-international-group)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.