Analysis of the Far-Reaching Impact of the U.S. Approval for Samsung to Ship Chip Equipment to Its Chinese Factories

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This policy adjustment occurred during a critical period of U.S.-China tech competition. According to the latest information, the U.S. chip export control policy towards China has undergone significant changes: the Trump administration announced the postponement of tariffs on Chinese semiconductor imports until June 2027, while allowing NVIDIA to sell H200 AI chips to China and granting temporary exemptions to Samsung and SK Hynix’s factories in China [1][2]. This series of measures signals a shift in U.S. chip policy towards China from ‘full blockade’ to ‘precision control’.

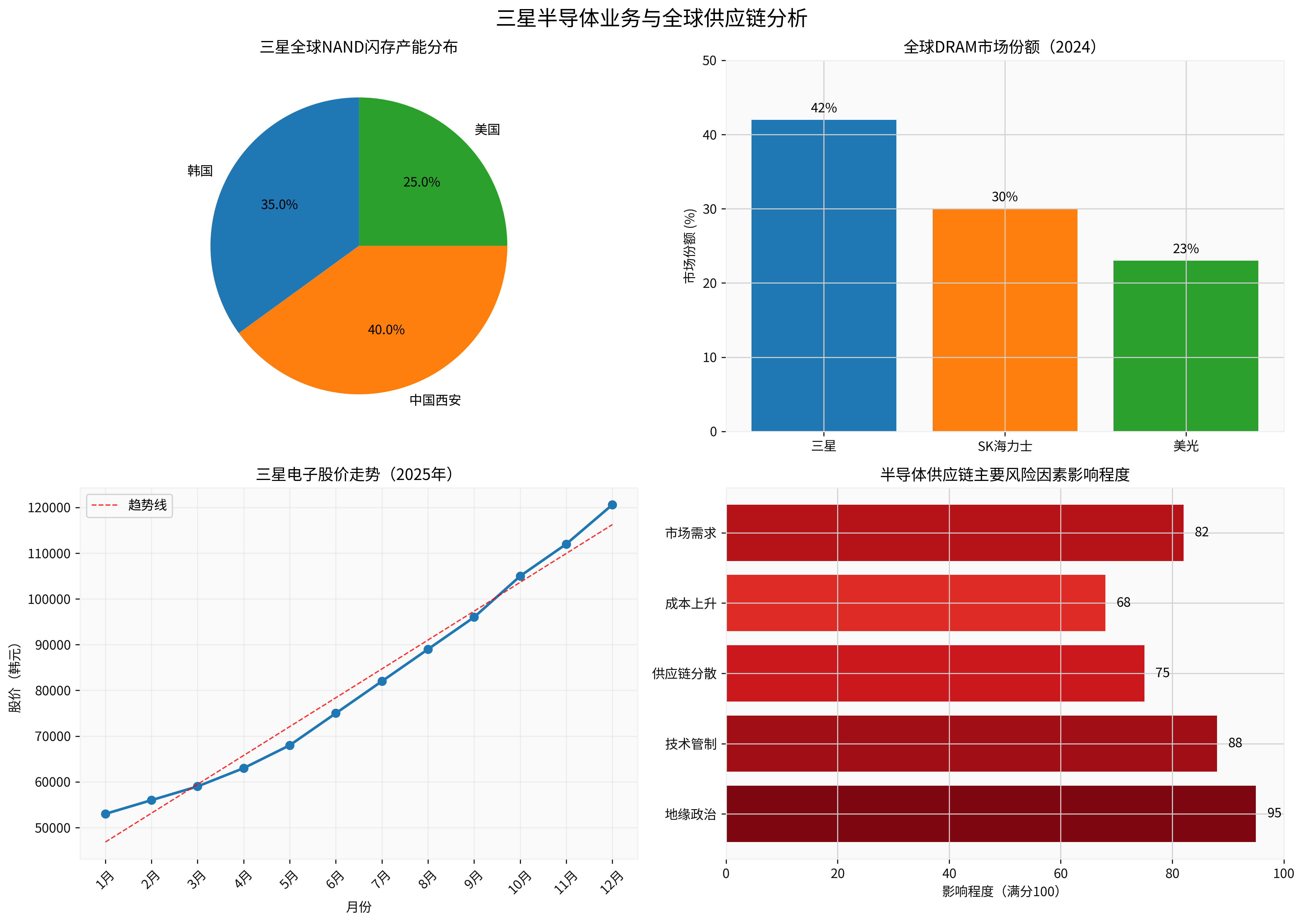

Currently, Samsung Electronics has a strong financial position. Its stock price rose by more than 125% cumulatively in 2025, with a market capitalization of 806.34 trillion KRW (approximately 671 billion USD) and a P/E ratio of 24.82x [0]. This market performance reflects investors’ confidence in Samsung’s prospects in the AI and storage chip sectors.

Samsung’s Xi’an factory is the core base of its global NAND flash capacity, with a monthly output of approximately 200,000 wafers, accounting for about 40% of the global NAND market share [1]. The U.S. approval for equipment shipment will:

- Ensure Stable Global NAND Supply: As Samsung’s most important NAND production base, equipment updates are directly related to the global storage chip supply.

- Avoid Supply Chain Disruption Risks: The global semiconductor foundry market reached 84.8 billion USD in Q3 2025, a year-on-year increase of 17% [5]. Any supply disruption will impact the global tech industry.

- Maintain Price Stability: Storage chip prices continued to rise in 2025 (DRAM prices increased by 171.8% year-on-year in Q3) [4]. Stable supply will help mitigate price fluctuations.

According to JIWEL Consulting data, the global wafer foundry capacity distribution is undergoing profound changes:

- In 2025, China’s monthly wafer capacity reached 10.1 million 8-inch equivalents, accounting for 35% of the global total.

- By 2027, China’s capacity in mature processes (28nm and above) will account for 47% of the global total, far exceeding Taiwan’s 36% [5].

This trend indicates that although the U.S. restricts the inflow of advanced process technology into China, mature process capacity is still expanding rapidly. Enterprises like Samsung participate in this process through their factories in China, which actually intensifies the geopolitical complexity of the global semiconductor industry.

The U.S. strategy shows obvious ‘technology stratification’ characteristics:

- For advanced processes(below 7nm, EUV lithography machines): Strict blockade.

- For mature processes(28nm and above): Allow limited development.

- For storage chips: Grant temporary exemptions to Korean enterprises.

This strategy not only slows down China’s catching-up speed in advanced processes but also avoids completely激化 contradictions leading to supply chain collapse, which is a refined geopolitical balancing act.

According to industry data:

- DRAM Market: Samsung holds 42% of the market share, ranking first globally.

- NAND Market: Samsung has approximately 37% of the market share, also leading [1].

The U.S. approval for equipment updates will enable Samsung to:

- Maintain the technical competitiveness of its Xi’an factory and ensure its leading position in advanced storage technologies such as V-NAND.

- Avoid production efficiency decline due to equipment aging (there was a case where a factory’s production efficiency dropped by 15% due to equipment maintenance issues [6]).

- Continue to utilize China’s relatively low production costs and完善 supply chain system.

Samsung’s capacity layout in China gives it significant cost advantages:

- Labor Cost: The cost of engineers and technicians in China is approximately 60-70% of that in Korea.

- Supply Chain Support: China’s semiconductor material and equipment supply chain is increasingly完善.

- Scale Effect: Centralized production at the Xi’an factory brings economies of scale.

These advantages allow Samsung to maintain a 10-15% cost advantage over competitors like Micron and Western Digital, making it more resilient in price wars.

Global storage chip buyers (including Apple, Dell, HP, etc.) attach great importance to supply chain stability. Samsung’s ability to continue shipping from its Chinese factories makes it more attractive in the following aspects:

- Supply Guarantee: Ensure long-term stable supply capacity.

- Risk Diversification: Reduce geopolitical risks through capacity layout in Korea, China, and the U.S.

- Technical Response: Quickly respond to demand changes from customers in different regions.

Samsung is adopting a ‘dual-track technology strategy’:

- Korea Local: Focus on R&D of the most advanced technologies (e.g., HBM4, 10nm-class DRAM).

- Xi’an, China: Focus on mature NAND technology and large-scale production.

- New U.S. Factory: Target government customers and high-security applications.

This layout allows Samsung to maximize the use of policy advantages in various regions while maintaining technical competitiveness in compliance with regulations.

The U.S.'s ‘conditional approval’ for Samsung and SK Hynix reflects multiple considerations:

- Avoid Supply Chain Disaster: China accounts for more than 35% of global semiconductor capacity; a complete cutoff will lead to global chip shortages.

- Maintain Ally Relationships: Korea is an important U.S. ally in the Indo-Pacific region; excessively harming Korean enterprises’ interests will affect bilateral relations.

- ‘Precision Decoupling’ Strategy: Only restrict the most advanced technologies (e.g., EUV lithography machines) and allow mature processes to continue developing.

- Time for Space: By postponing tariffs until 2027, it buys time for U.S. enterprises (e.g., Micron, Intel) to transfer capacity [2].

Facing U.S. restrictions, China is accelerating semiconductor autonomization:

- Equipment Localization: SMIC’s 28nm lithography machine has a yield rate of 90%, and plans to mass-produce EUV equipment in 2026 [6].

- Capacity Expansion: China’s wafer capacity increased by 14% year-on-year in 2025, reaching 35% of the global total [5].

- Market Share Growth: China’s wafer foundry market share has increased from 5% in 2000 to 21% in 2024 [5].

ASML CEO Christophe Fouquet once warned: ‘If China is pushed into a corner, it will completely break away from Western technology. When China completes independent R&D, it may export to us in reverse’ [6]. This concern is becoming a reality.

The global semiconductor industry chain is undergoing profound reconstruction:

Dimension |

Traditional Model |

Future Trend |

|---|---|---|

Geographic Distribution |

Concentrated in East Asia (Taiwan, Korea, Japan, China) | Decentralized (U.S., Europe, Southeast Asia) |

Technology Hierarchy |

Vertical Integration | Technology Stratification (Separation of Advanced and Mature Processes) |

Supply Chain |

Global Integration | Regionalization, Friendshoring |

Investment Model |

Market-Driven | Government Subsidy-Driven (e.g., CHIPS Act) |

Despite obtaining equipment approval, Samsung still faces multiple challenges:

- Policy Uncertainty: The U.S.'s ‘temporary exemption’ may be revoked at any time, and long-term investment has risks.

- Technological Gap: The Xi’an factory cannot obtain the most advanced equipment (e.g., EUV), which will gradually lag behind Samsung’s local factories in Korea.

- Geopolitical Risks: Deterioration of Sino-U.S. relations may lead to further restrictions or even require Samsung to withdraw from China.

- Competitors Catching Up: Competitors like SK Hynix and Yangtze Memory are rapidly narrowing the technological gap.

- Supply Chain Fragmentation: The global supply chain is splitting into ‘U.S. camp’ and ‘China camp’.

- Cost Increase: Supply chain reconstruction leads to a 10-15% increase in global semiconductor production costs.

- Decline in Innovation Efficiency: Technology blockade and scattered investment may slow down the global semiconductor innovation speed.

- Market Distortion: Government intervention leads to decreased resource allocation efficiency and overcapacity in some areas.

- Samsung’s Performance: Driven by AI demand and storage chip price increases, Samsung’s semiconductor sector revenue is expected to continue growing.

- Stock Price Impact: Although it has risen by 125% in 2025, if AI demand continues, there is still upside potential for the stock price.

- Policy Risks: Need to closely monitor policy changes before the implementation of tariffs in 2027.

- Technological Differentiation: Advanced processes (3nm, 2nm) are still dominated by TSMC and Samsung (Korea), while mature processes are gradually dominated by China.

- Supply Chain Regionalization: Major economies will establish relatively independent semiconductor supply chains.

- New Competitive Pattern: A ‘bipolar system’ may emerge — U.S. alliance vs China’s autonomous system.

For investors关注 Samsung and the semiconductor industry:

- Strong growth in storage chip demand driven by AI.

- Samsung’s solid leading position in the DRAM and NAND markets.

- The capacity advantage of Chinese factories will maintain cost competitiveness.

- Geopolitical risks may lead to supply chain disruption.

- Rapid catching-up by Chinese local enterprises (e.g., Yangtze Memory, Changxin Memory).

- Global semiconductor cyclical fluctuation risks.

- Short-Term Hold: Benefit from the cyclical upward trend of AI and storage chips.

- Long-Term Observation: Focus on Samsung’s strategic adjustments to its capacity in China and technological route choices.

- Risk Hedging: Consider allocating semiconductor assets in other regions (e.g., Taiwan, U.S.) to diversify geopolitical risks.

The U.S. approval for Samsung to ship chip equipment to its Chinese factories is an important symbol of U.S.-China tech competition entering the ‘refined control phase’. This decision:

- Short-Term: Stabilizes the global storage chip supply chain and avoids potential supply crises.

- Medium-Term: Provides Korean enterprises like Samsung with ‘breathing space’ to maintain competitiveness.

- Long-Term: Reflects the U.S.'s ‘precision decoupling’ strategy — limiting the most advanced technologies and allowing mature processes to develop, to achieve the dual goals of slowing down China’s technological progress and avoiding global economic damage.

For Samsung, this is both an opportunity and a challenge. The company can continue to utilize the capacity advantages of China, but needs to balance technological upgrades and geopolitical risks. The next three years (2026-2028) will be a critical period for the reconstruction of the global semiconductor industry chain, and Samsung’s strategic choices will profoundly affect its long-term competitive position.

[1] Jinling API Data - Samsung Electronics Company Overview and Financial Data

[2] Reuters - “US delays announcement of China chip tariffs until 2027” (https://www.reuters.com/world/china/us-impose-tariffs-chips-china-2025-12-23/)

[3] Fanggezi - “In-depth Research Report on Global DRAM and NAND Flash Memory Industry”

[4] Electronic Engineering Album - “Samsung to Mass-Produce HBM4 Chips on a Large Scale!”

[5] JIWEL Consulting - “2025 China Wafer Foundry Industry Listed Company Research Report”

[6] Sina Finance - “Announce to the World! China Plans to Mass-Produce Lithography Machines in 2026”

[7] NetEase - “Chip Foundry Market Changes: Mainland China is Truly Rising, Having Captured 21% Share”

[8] RFI French International Radio - “U.S.-China Semiconductor Offensive and Defensive War Reappears Turning Point: A Long and Arduous Road?”

[9] Tom’s Hardware - “Ten former Samsung employees arrested for industrial espionage charges” (https://www.tomshardware.com/tech-industry/semiconductors/ten-former-samsung-employees-arrested-for-industrial-espionage-charges-for-giving-china-chipmaker-10nm-tech)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.