Photovoltaic Industry Leading Enterprises Investment Value Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on the latest data and market information obtained, I will provide you with a comprehensive investment value analysis report on leading enterprises in the photovoltaic industry.

- Current Stock Price: 21.80 CNY (2025-12-26)

- P/E Ratio: -11.51x (negative value indicates loss)

- P/B Ratio: 2.19x

- ROE: -18.28% (in severe loss status)

- Net Profit Margin: -9.44%

- Current Ratio: 1.24 (liquidity is acceptable)

- Tongwei Co., Ltd. is in a deep loss statewith an ROE of -18.28%, far below the healthy level.

- It rebounded 45.5% from the annual low of 14.98 CNY on June 19, 2025 [0], indicating improved market expectations.

- P/B ratio of 2.19xis relatively high for a loss-making enterprise, suggesting the market has partially priced in future recovery expectations.

- Current Stock Price: 54.96 CNY

- P/E Ratio: -1820.00x (distorted due to extremely low profitability)

- P/B Ratio: 2.01x

- ROE: -0.11% (near break-even)

- Net Profit Margin: -0.16%

- Current Ratio: 0.31 (tight liquidity)

- Hesheng Silicon Industry is near break-even(ROE -0.11%), better than Tongwei.

- Higher liquidity riskwith a current ratio of only 0.31; need to monitor short-term debt repayment pressure.

- Latest financial report (2025-10-29): EPS 0.06 CNY vs. expected 0.27 CNY, 77.8% below expectations, indicating profit recovery is still weaker than expected [0].

Chart 1: 2025 full-year price trends and 60-day moving average of the two stocks. Tongwei rebounded more strongly from the low (45.5% vs. 21.6%) with higher volatility.

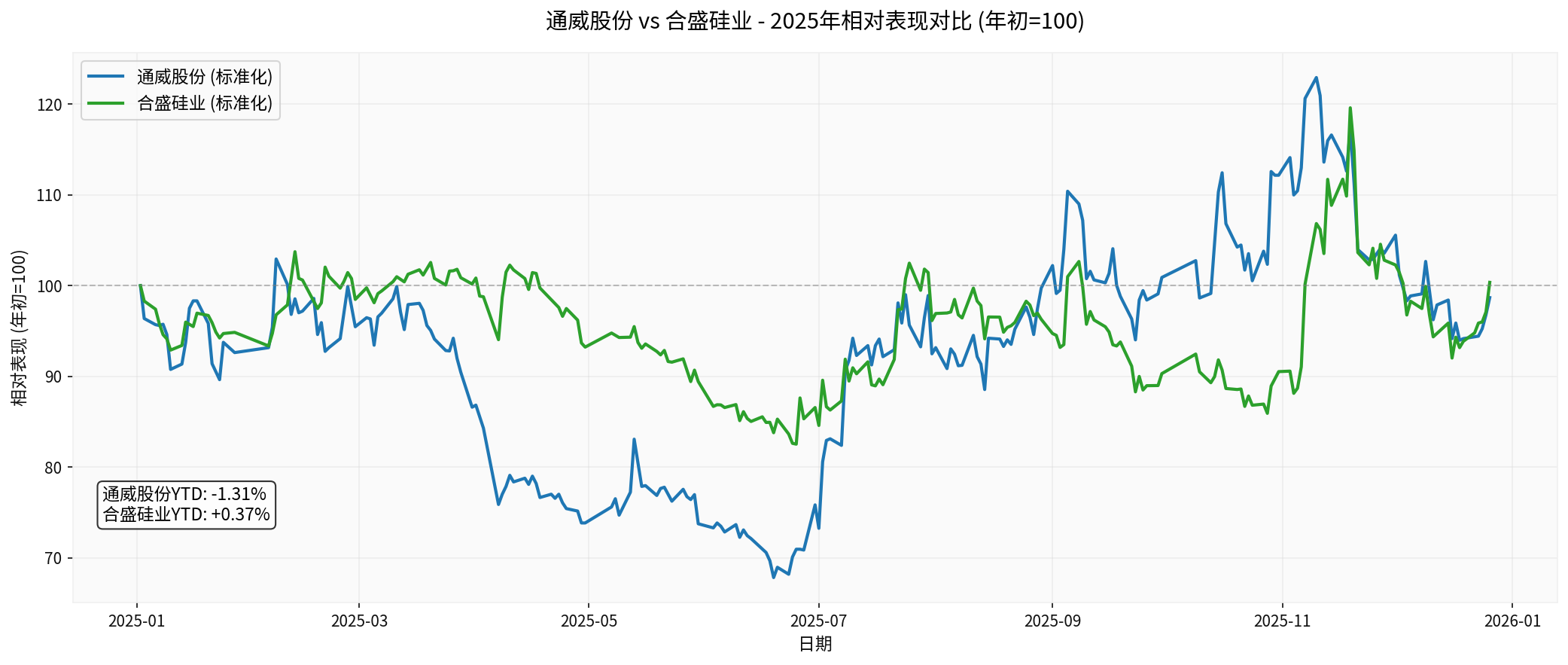

Chart 2: Normalized comparison with the beginning of the year as 100. Hesheng Silicon Industry performed slightly better than Tongwei (+0.37% vs. -1.31%) for the year, but both significantly underperformed the broader market.

According to market information, the polycrystalline silicon industry is undergoing

-

Leaders Join Forces to Address Overcapacity: Multiple Chinese polycrystalline silicon producers, including Tongwei Co., Ltd., have established a joint venture to jointly address overcapacity issues. Tongwei holds 30.35%, while GCL Technology and Daqo New Energy hold 16.79% and 11.13% respectively [1].

-

Strict Policy Control Over New Capacity:

- The Ministry of Industry and Information Technology and other departments issued the “Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry”, strictly controlling new capacity.

- Jiangsu Province explicitly eliminated small and inefficient devices to promote the industry towards scale and intensification [2].

- Fixed asset investment in the chemical raw material manufacturing industry decreased by 5.2% year-on-year in the first eight months of 2025, and the capacity release cycle is nearing its end [2].

-

JPMorgan Optimistic About 2026: The bank pointed out that as corporate profitability gradually improves and the industry competition pattern becomes rational, the profit margins of leading enterprises in the photovoltaic and lithium battery industries under the “anti-involution” theme have begun to recover [2].

Based on your provided observations:

- Q3 polycrystalline silicon average price was about 50,000 CNY: Enterprises were basically break-even.

- Q4 polycrystalline silicon average price was about 60,000 CNY:Key Observation— Can gross margin reach 20%?

This price level is crucial for profitability recovery. If Q4 can maintain 60,000 CNY/ton and cost control is proper, the gross margin of leading enterprises is expected to improve significantly.

✅

- Small and medium-sized capacity is forced to exit, leading enterprises’ market share increases.

- Capacity utilization rate rebounds, unit cost decreases.

✅

- Polycrystalline silicon price rebounded from the bottom to 60,000 CNY/ton (your observation data).

- Price is close to the profit inflection point, with further upward momentum.

✅

- Industry consortium led by Tongwei and other leaders enhances bargaining power [1].

- Anti-involution policies prevent new capacity shocks [2].

✅

- Global photovoltaic installation demand continues to grow.

- High growth in AI infrastructure capital expenditure in 2026 benefits photovoltaic demand [2].

❌

- Tongwei’s ROE is -18.28%, requiring a long process to recover from deep losses to profitability [0].

- Hesheng Silicon Industry’s ROE is only -0.11%, but the latest financial report was below expectations, casting doubt on the strength of recovery [0].

❌

- Both companies have a P/B ratio of over 2x (Tongwei:2.19x, Hesheng:2.01x), which is not low in a loss state [0].

- The market has partially priced in profit improvement expectations (Tongwei rebounded 45.5% from the low).

❌

- Hesheng Silicon Industry’s current ratio is only 0.31, with high short-term debt repayment pressure [0].

- May face financing pressure before profit recovery.

❌

- Although policy-driven, actual clearing speed may be slower than expected.

- If prices fall back below 50,000 CNY, profit improvement will be delayed again.

| Polycrystalline Silicon Price | Industry Profit Status | Corresponding Gross Margin |

|---|---|---|

| 50,000 CNY/ton | Basic break-even | 0-5% |

| 60,000 CNY/ton | Key Observation |

15-20% (Target) |

- P/E: Not applicable (loss)

- P/B:2.19x

- Market Capitalization: Approximately 95.9 billion USD

- Valuation Assessment: Moderately High, partially pricing in recovery expectations.

- P/E: -1820x (distorted due to extremely low profitability)

- P/B: 2.01x

- Market Capitalization: Approximately 64.4 billion USD

- Valuation Assessment: Moderately High, liquidity risk needs discounting.

The Price-Earnings to ROE Ratio (PR) formula you developed:

| ROE Level | Theoretical Reasonable PB | Current Actual PB (Tongwei) | Current Actual PB (Hesheng) |

|---|---|---|---|

| 30% | About3-4x | 2.19x (Undervalued) | 2.01x (Undervalued) |

| 20% | About2-2.5x | 2.19x (Reasonable) | 2.01x (Reasonable) |

| 10% | About1-1.5x | 2.19x (Overvalued) | 2.01x (Overvalued) |

-18% (Tongwei Actual) |

N/A | 2.19x (Severely Overvalued) |

- |

-0.1% (Hesheng Actual) |

N/A | - | 2.01x (Severely Overvalued) |

- Both companies have negative current ROE, PR model is not applicable.

- If ROE recovers to15-20%, current P/B of2x is reasonably low valuation.

- But before ROE turns positive, current valuation is expensiveas it prices in unrealized profit improvement.

✅

- Supply-side reform policy benefits.

- Capacity clearing trend.

- Price rebound from the bottom.

- Stable leading position.

❌

- Actual extent of profitability recovery (needs Q4 financial report verification).

- Uncertainty whether Q4 gross margin can reach 20%.- Specific progress and timeline of capacity clearing.

- Sustainability of demand-side growth.

- ✓ Polycrystalline silicon leader, most benefited.

- ✓ Rebounded 45.5% from the low, indicating restored market confidence.

- ✓ Participated in industry consortium, strong control [1].

- ✗ Currently in deep loss (ROE -18.28%) [0].

- ✗ P/B of 2.19x is high in loss state.

- Existing Holdings: Can continue to hold, but set stop-loss level (e.g.,18-19 CNY).

- New Investors: Wait for Q4 financial report to verify gross margin突破20% before entering.

- Observation Indicators:

- Whether Q4 polycrystalline silicon average price maintains 60,000 CNY.

- Whether Q4 gross margin reaches 20%.- Whether 2026Q1 profit forecast exceeds expectations.

- ✓ ROE near break-even (-0.11%), better than Tongwei [0].

- ✓ 2025 YTD performance slightly better (+0.37% vs. -1.31%).

- ✗ High liquidity risk (current ratio of0.31) [0].

- ✗ Latest financial report significantly below expectations (EPS -77.8%) [0].

- ✗ Industrial silicon demand is weaker than polycrystalline silicon.

- Not Recommended for New Positions: High liquidity risk and underperformance risk.

- Existing Holdings: Consider stop-loss or hedging; prioritize monitoring Q4 cash flow improvement.

- Watch Conditions: Wait for current ratio to rise above 0.7 and consecutive two quarters of profit exceeding expectations.

✅

- Price has reached the 60,000 CNY target; consider phased profit-taking with “sell more as it rises”.

- Retain part of the exposure as a spot substitute and hedge tool.

⚠️

- Tongwei can be a standard allocation in the stock part, but control position (no more than30%).

- Hesheng Silicon Industry is recommended to avoid temporarily, or wait for clearer profit signals.

📊

- Increase allocation to inverter segment(e.g., Sungrow Power Supply): More benefited from installation growth, less price competition [3].

- Focus on enterprises with leading overseas layout: Like JinkoSolar (U.S. factory put into production), avoid trade barriers [2].

- Consider power station operation: Stable business model, less affected by industrial chain price fluctuations.

| Time Node | Observation Focus | Verification Standard | Impact on Investment Decision |

|---|---|---|---|

January2025 |

Q4 Financial Report Release | Gross margin ≥20% | ✓ Increase Tongwei holdings if met |

February2025 |

Post-Spring Festival Demand Start | Polycrystalline silicon price maintains60,000 CNY | ✓ Increase positions if price stabilizes |

March2025 |

2025Q1 Forecast | Profit exceeds expectations | ✓ Confirm reversal trend |

June2025 |

2025 Half-Year Report | ROE turns positive and >10% | ✓ Confirm cyclical reversal |

End of2025 |

2025 Annual Report Verification | Full-year profit exceeds expectations | ✓ Long-term holding confidence |

- Macroeconomic Risk: Global economic slowdown may affect photovoltaic installation demand.

- Policy Change Risk: Policy risks such as subsidy withdrawal and trade barriers.

- Technology Route Risk: New technologies (e.g., perovskite) may impact the existing pattern.

- Capacity Clearing Not Meeting Expectations: Price war may restart.

- Liquidity Risk: Especially for Hesheng Silicon Industry, need to monitor short-term debt pressure.

[0] Gilin AI Financial Database - Financial data, valuation indicators, price data and technical analysis of Tongwei Co., Ltd. (600438.SS) and Hesheng Silicon Industry Co., Ltd. (603260.SS)

[1] Bloomberg - “China’s Polysilicon Giants Join Forces to Tackle Overcapacity” (December10,2025) - https://www.bloomberg.com/news/articles/2025-12-10/china-s-polysilicon-giants-join-forces-to-tackle-overcapacity

[2] JPMorgan 2026 Investment Outlook - “JPMorgan Optimistic About Four Theme Drivers of MSCI China Index in2026” - https://hk.finance.yahoo.com/news/摩根大通看好2026-msci中國指數-ai-反內卷-海外佈局與消費復甦四大主題驅動-231004197.html

[3] Yahoo Finance - “Citi: PV Product Prices Relatively Stable This Week, Polycrystalline Silicon Price Downside Limited, Focus on Anti-Involution” - https://hk.finance.yahoo.com/news/花旗-本周光伏產品價格相對穩定-料多晶硅價下行有限-關注反內捲-021456401.html

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.