2025 Thermal Power Sector Valuation Recovery and Investment Analysis of Wanneng Power (000543.SZ) & Beijing Energy Power (600578.SS)

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

- Foundation of coal price-thermal power logic: Current rising capital expenditure on the coal supply side brings pressure for capacity rebalancing and inventory accumulation, making it difficult for coal prices to rise sustainably, which provides conditions for bottoming out the input costs of thermal power plants; if electricity prices remain range-bound, the logic for thermal power to shift from a strong cyclical to a “high dividend + cash flow” attribute is sound.

- Valuation recovery path: Wanneng Power (000543.SZ) currently has a P/E of only 8.38x, P/B of 1.16x, and ROE of 14.63%, reflecting good profitability and capital efficiency but being undervalued; although the specific P/E data of Beijing Energy Power (600578.SS) has not been fully obtained yet, its 2024 net profit was 1.723 billion yuan and asset-liability ratio was 137%, with tight liquidity; short-term valuation recovery depends on stable cash flow and dividend expectations.

- Institutional preference direction: The current shift from a “dividend floor” to a combination of “declining coal prices + new energy catalysts” is reasonable, but we still need to monitor the suppression of electricity prices by excess power supply in Anhui region.

- Coal price pressure and supply-demand characteristics: In 2025, coal mining enterprises (such as China Shenhua, Shaanxi Coal Industry) have limited gains compared to power companies, reflecting sufficient upstream supply; thermal power companies gain marginal profits through declining coal prices, which is consistent with the phased shift from “strong cyclical -> dividend stock”.

- Profit stability/cash flow perspective: Wanneng Power’s cash flow indicators are negative in the metadata but overall ROE is high (14.63%) and net profit margin is 8.14% [0]; Beijing Energy Power’s 2024 revenue was 35.43 billion yuan, net profit was 1.72 billion yuan, and gross profit margin remained around 13%, indicating that profitability has elasticity under the premise that coal prices no longer rise.

- New energy and consumption advantages: The topic mentions new energy projects and priority consumption; if the grid connection of renewable energy installations and energy storage accelerates in the future, it will further enhance the sustainability of dividends; at the same time, high supply in Anhui may suppress electricity prices, which must be accompanied by consumption improvement or a shift to a parity bidding mechanism.

| Dimension | Wanneng Power (000543.SZ) | Beijing Energy Power (600578.SS) |

|---|---|---|

| Current Price | 8.82 yuan | 5.38 yuan |

| 2025 YTD Gain | +14.7% | +57.3% |

| 2024 YTD Gain | +33.8% | +78.7% |

| 20/60-day Moving Average | 8.31 / 8.08 yuan, stock price above moving average | 4.76 / 4.69 yuan, stock price also rising |

| Annualized Volatility | 33.45% | 27.95% |

| Sharpe Ratio (assuming 2.5% risk-free rate) | 2.71 | 2.20 |

| Valuation | P/E 8.38x, P/B 1.16x, ROE14.63% | Key valuation not disclosed timely, asset-liability ratio137%, current ratio0.51 (tight) [0] |

| Financial Health | Conservative financial attitude (high depreciation/high CapEx) | Stable gross profit and EBITDA growth but high cash leverage [0] |

##4. Strategy and Risk Tips

- Balance “dividend + catalyst”: Dividend-focused positions with Wanneng as the core can be increased opportunistically at quarterly report/dividend announcement, Anhui new energy commissioning, and environmental compliance nodes; Beijing Energy can be used as a second-line flexible addition, focusing on coal price recovery and changes in financing costs.

- Risk control: Electricity prices in Anhui region are suppressed by high supply; need to continuously monitor inter-provincial transactions of regional power grids, electricity price policy adjustments, and new energy curtailment risks; if coal prices rebound or national regulation on thermal power tightens, the logic needs to be re-evaluated.

- Attention signals: Observe changes in the revenue share of “non-coal power (new energy/energy storage)” of the two companies, dividend plans, coal price sensitivity, and capital expenditure rhythm. If Wanneng announces a high dividend target and Beijing Energy optimizes its debt structure, the valuation recovery window will be larger.

##5. Data Visualization Supplement

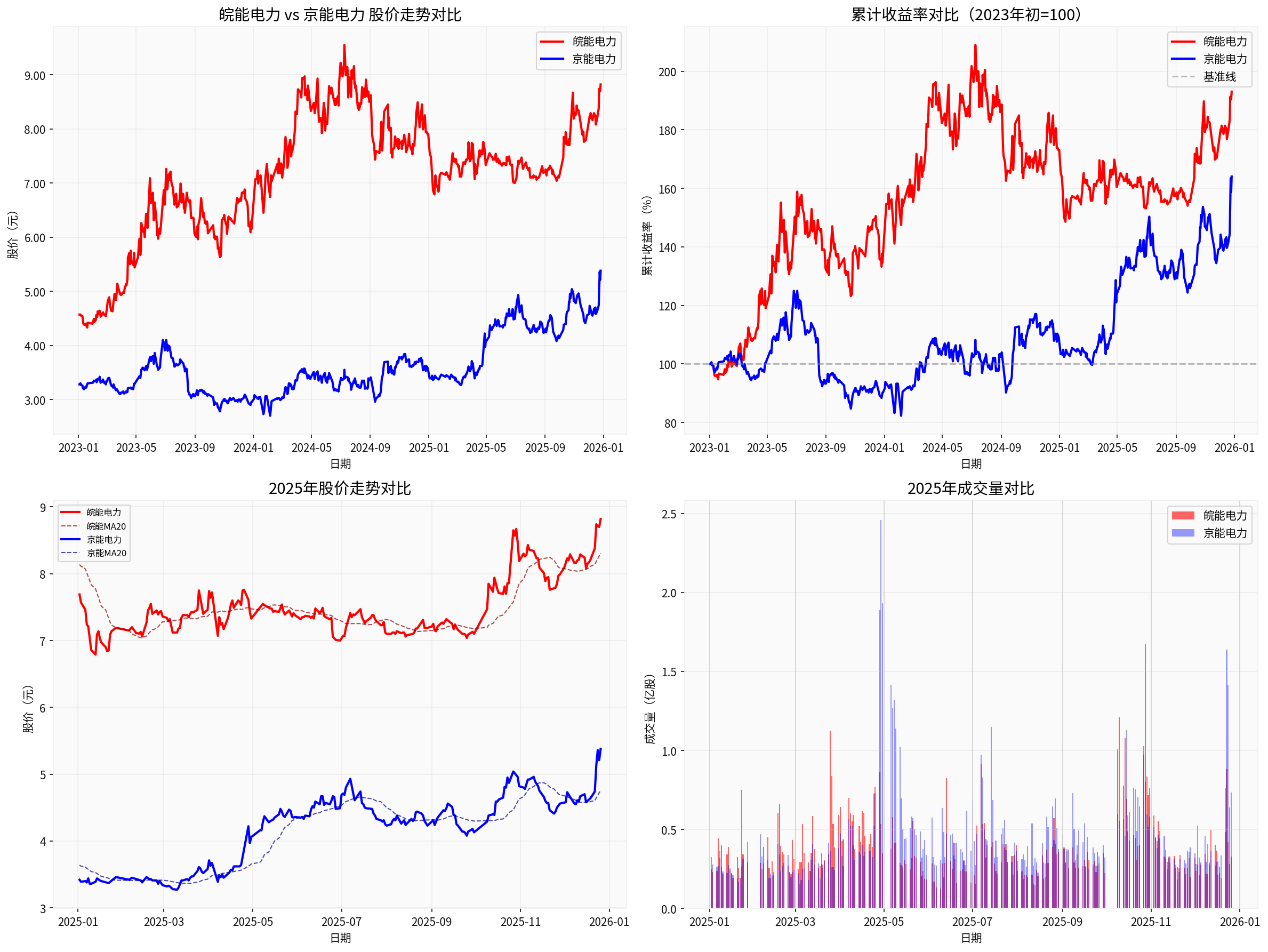

Figure note: The chart shows the comparison of stock prices and cumulative returns of the two companies since 2023 (X-axis: date; Y-axis: stock price/normalized return), with 2025 trends and trading volume attached, supporting the intuitive judgment that “Wanneng is undervalued and Beijing Energy has higher elasticity.” [0]

##6. Need to Enable Deep Research Mode

If you need to further verify regional supply-demand models, coal price sensitivity, dividend forecasts, or obtain more industry research, institutional ratings, and event-driven judgments, you can enable the

[0] Jinling API Data (including real-time quotes, financial indicators, Python custom analysis and charts for Wanneng Power/Beijing Energy Power, 2025-12-27)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.