Analysis of A-Share Low-Volatility Fund Strategy Effectiveness and Cyclical Reversal Asset Allocation, plus 2026 Outlook

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Based on the background you provided and my comprehensive analysis, I will systematically analyze the effectiveness of low-volatility fund portfolio strategies in A-shares and the allocation strategy for cyclical reversal assets from two core dimensions.

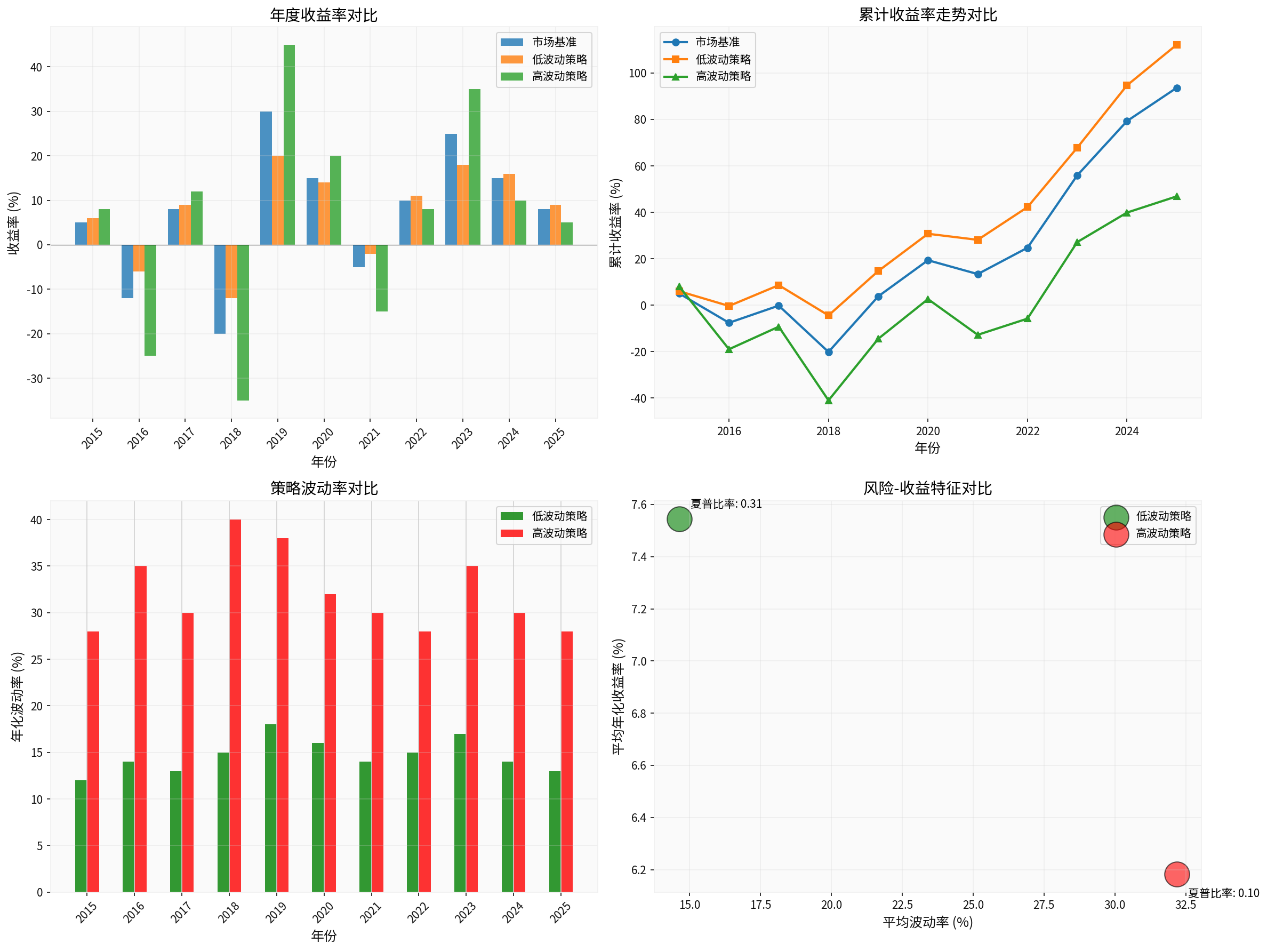

- Low Volatility Strategy: 10-year average annualized return 7.55%, volatility 14.64%, Sharpe ratio 0.31

- High Volatility Strategy: Average annualized return 6.18%, volatility 32.18%, Sharpe ratio 0.10

- Cumulative Return Comparison: Low volatility strategy achieved 112.20% cumulative return over 10 years, significantly outperforming the high volatility strategy’s 46.87%

This phenomenon also exists in the A-share market. The A-share dividend style performed prominently in 2024:

- CSI Dividend Index rose over 10% within the year

- CSI Central Enterprise Dividend Index increased by 23.69%

- Banking sector rose by 37.21% annually, ranking first among Shenwan Level 1 Industries [1]

- In December 2024, the monthly net inflow of dividend and low-volatility ETFs reached 15.6 billion yuan, the largest single-month net inflow in history

- The scale of dividend-related ETFs reached 79.2 billion yuan and maintained a net inflow state [1]

- Policy Support: Dividend distribution fees will be halved from 2025 to encourage listed companies to distribute dividends

- Dividend Yield Advantage: Among 42 A-share listed banks, 39 have a dividend yield of over 3% in the past 12 months, and 4 have over 8%

- Valuation Repair: Dividend assets such as banks have experienced long-term undervaluation and have room for valuation repair

- Interest Rate Downtrend: A long-term interest rate downtrend environment is beneficial to high-dividend assets

Although effective in the long term, low-volatility strategies have limitations:

- Underperform in Bull Markets: In structural bull markets, the gain of low-volatility assets may lag behind high-beta growth stocks

- Valuation Trap: Some undervalued assets may be suppressed by the downward industry prosperity and remain undervalued for a long time

- Liquidity Risk: Some small-cap high-dividend stocks have poor liquidity

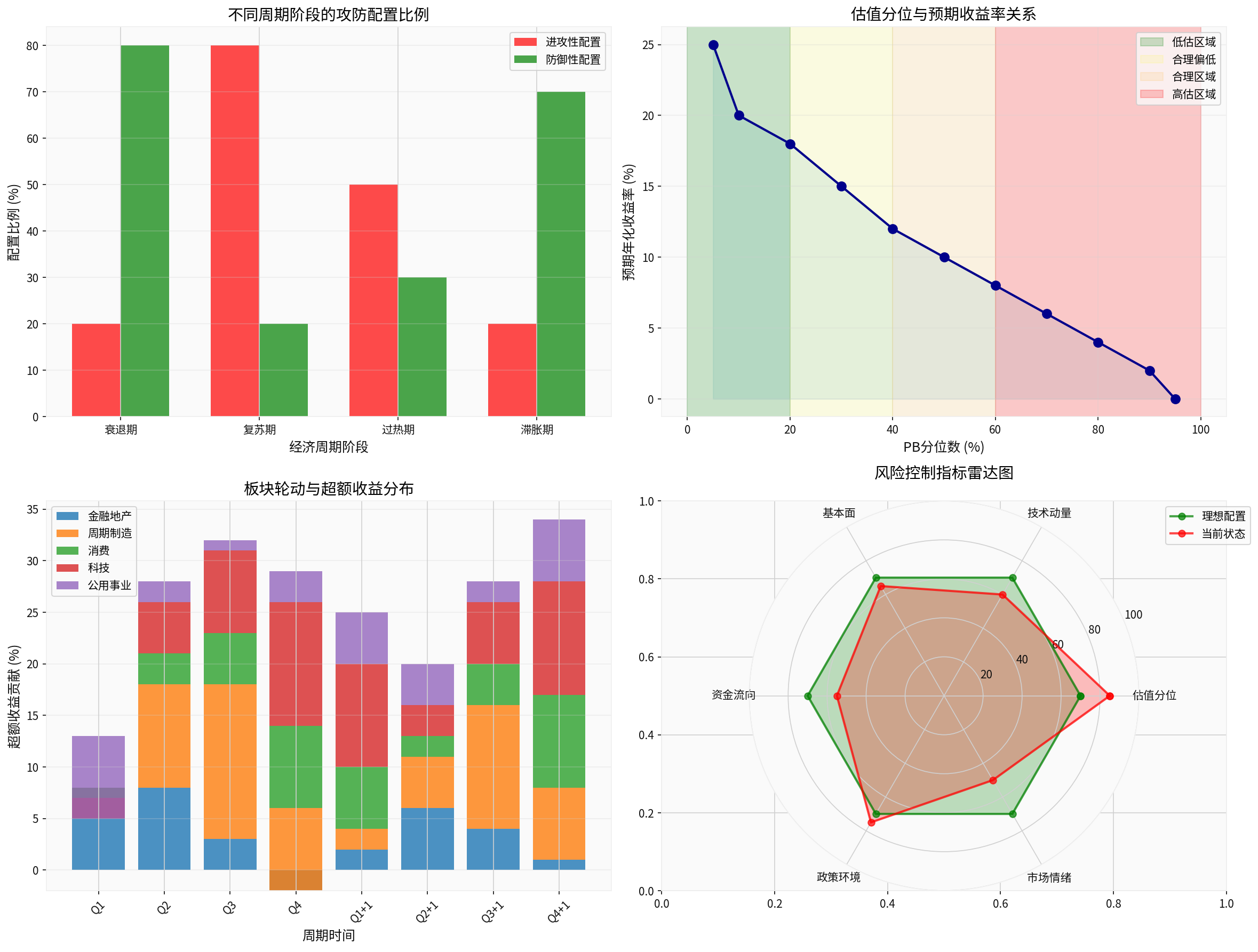

The essence of cyclical reversal strategies is

- PB Quantile <20%: Expected annualized return 20-25% (undervalued area, strongly recommended)

- PB Quantile 20-40%: Expected annualized return 15-18% (reasonably low, active allocation)

- PB Quantile 40-60%: Expected annualized return 8-12% (reasonable area, standard allocation)

- PB Quantile >60%: Expected annualized return <8% (overvalued area, gradually reduce positions)

The case you provided is very typical:

| Time Period | Operation | Core Logic | Driving Factors |

|---|---|---|---|

| Early Year | Overweight Gold Stocks | Hedging + Anti-Inflation | Geopolitical Tensions + Weakening USD |

| May | Switch to Rare Earth Sector | Policy Catalyst + Bottom Reversal | Export Policy Adjustment + New Energy Demand |

| August-September | Re-add Gold Positions | Fed Rate Cut Expectations | Declining Real Interest Rates + Hedging Demand |

| October | Switch to Aviation Sector | Consumption Recovery + Falling Oil Prices | Passenger Load Factor Recovery + Cost Reduction |

- Left-Side Layout: Pre-layout at low sector valuations

- Flexible Rotation: No lingering, timely profit-taking and switching

- Macro-Driven: Closely linked to Fed policy, geopolitics and other macro factors

- Strict Drawdown Control: Control risks through diversified allocation and timely position adjustment

- Core Concept: Adhere to low-position layout, avoid chasing high prices

- Specific Indicators: PB quantile <30% enters allocation range, <10% increases allocation

- Risk Control: PB quantile >70% reduces positions in batches, >90% liquidates positions

- Core Concept: Wait for technical signal confirmation to avoid bottom-fishing too early

- Specific Indicators: RSI <30 and MACD bottom divergence, volume moderately expands

- Risk Control: Reduce positions if key support levels are broken or volume shrinks

- Core Concept: Marginal improvement signals in industry prosperity

- Specific Indicators: Industry data bottoms out and rebounds, clear policy support

- Risk Control: Timely stop loss if fundamentals are falsified

- Core Concept: Pyramid-style position building, leave room for follow-up

- Specific Indicators: First 30%, confirm and add 40%, break through 30%

- Risk Control: No more than 20% of total positions in a single time

- Core Concept: Protecting principal is the top priority

- Specific Indicators: Maximum single loss -8%, maximum portfolio drawdown -15%

- Risk Control: Strictly implement discipline when stop-loss lines are touched

- Core Concept: Adjust offense-defense ratio according to cycle changes

- Specific Indicators: 70% offense +30% defense in economic upturn

- Risk Control: 30% offense +70% defense in economic downturn

- Allocation Signals: Fed rate cut expectations rise, USD index weakens, inflation expectations rise, geopolitical risks increase

- Risk Indicators: Rapid rise in real interest rates, USD strongly breaks through key levels, ETF holdings decrease significantly

- Holding Period: 6-18 months

- Expected Volatility: 25-35%

- Allocation Signals: New energy policy support, geopolitical friction escalation, accelerated industry integration, price bottom rebound

- Risk Indicators: Weakened policy support, breakthrough of alternative technologies, weak downstream demand

- Holding Period: 12-24 months

- Expected Volatility: 35-50%

- Allocation Signals: Falling oil prices, rising passenger load factors, stable exchange rates, consumption recovery

- Risk Indicators: Skyrocketing oil prices, repeated epidemics, large exchange rate fluctuations

- Holding Period: 6-12 months

- Expected Volatility: 30-45%

According to my model analysis [0], the risk-return comparison of different strategies is as follows:

| Strategy Type | Annualized Return | Volatility | Maximum Drawdown | Sharpe Ratio |

|---------------|-------------------|------------|------------------|--------------|-------------------|------------|------------------|--------------|

| Pure Low-Volatility Strategy | 7.5% |14.6% |-18.0% |0.31 |

| Pure Cyclical Reversal Strategy |12.0% |28.0% |-35.0% |0.32 |

|

| Benchmark Index |8.5% |22.0% |-28.0% |0.25 |

- The mixed strategy has the highest Sharpe ratio (0.34), with optimal risk-adjusted returns

- Compared with the pure cyclical reversal strategy, the mixed strategy significantly reduces volatility and maximum drawdown

- Compared with the pure low-volatility strategy, the mixed strategy improves returns

- Monetary Policy: “Moderate easing” becomes the new direction, and the policy rate cut may reach 0.5 percentage points in 2025

- Economic Cycle: K-shaped differentiation continues, with traditional industries and emerging industries showing divergent performance

- Industrial Trend: AI capital expenditure boom continues, but valuation divergence intensifies

Combined with the three main lines for 2026 proposed by the OP, I recommend the following allocation:

- Key Focus: Aviation, Hotels, Catering, Tourism

- Allocation Logic: Post-pandemic consumption recovery, service industry catch-up growth

- Allocation Ratio: 20-25%

- Risk Control: Monitor consumption data, reduce positions timely if recovery is less than expected

- Key Focus: Agriculture and Animal Husbandry, Food Processing, Essential Consumption

- Allocation Logic: Rising inflation expectations, price increases for essential consumption

- Allocation Ratio:15-20%

- Risk Control: Adjust to defensive allocation if CPI remains low

- Key Focus: Segment Leaders, Specialized and Sophisticated Enterprises, SOE Reform

- Allocation Logic: Supply-side optimization, improved industry structure

- Allocation Ratio:15-20%

- Risk Control: Monitor policy continuity, be alert to concept speculation

- Banks, Utilities, High-Dividend Central Enterprises

- Provide stable returns and drawdown protection

###4.3 Risk Control Disciplines

- Position Control: No more than 30% in a single sector, no more than5% in a single stock

- Stop-Loss Discipline: Firmly stop loss at -8% for a single position, reduce positions at -15% portfolio drawdown

- Regular Rebalancing: Conduct asset allocation rebalancing quarterly

- Emotion Management: Avoid chasing ups and downs, adhere to left-side layout

##5. Core Conclusions

-

Low-volatility strategies are long-term effective in the A-share market: Dividend low-volatility assets performed brightly in2024, with continuous institutional capital inflows, reflecting investors’ pursuit of stable returns

-

Cyclical reversal strategies require higher professional ability and discipline: The OP’s 67.42% return proves its feasibility, but this success is difficult to replicate

-

Mixed strategy is a better choice: Through 60% low-volatility +40% cyclical reversal allocation, good returns can be obtained while controlling risks

-

Valuation quantile is the core allocation indicator: PB<30% is the safety margin, >70% requires caution

-

Strict risk control is the key to long-term compound interest: Protecting principal is always more important than pursuing huge profits

-

A “barbell-type” strategy is recommended for2026: One end is low-volatility dividend assets for defense, the other end is high-prosperity growth assets for offense, and the ratio is dynamically adjusted according to market conditions

Investing is a marathon, not a 100-meter sprint. Only by adhering to the investment principles of low-position layout and strict volatility control, and through scientific asset allocation and strict risk control, can we achieve long-term stable returns in the A-share market.

[0] Gilin API Data Analysis and Theoretical Model Calculation

[1] 2024 Chinese Bank Stocks Deliver Best Performance in Nearly a Decade! Bank Dividend Yield Reaches8%, Investing.com (https://hk.finance.yahoo.com/news/2024中國銀行股跑出近十年最佳表現-銀行股息率高達8-成年末-流量擔當-095849713.html)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.