Analysis of the Effectiveness of Momentum Rotation Strategy in China's Fund Market

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

According to the four-asset rotation strategy backtest you mentioned, this strategy uses a 20-day momentum signal and selects the strongest-performing asset for allocation every week. The backtest shows:

- Rotation Strategy: Annualized return 24.24%, Sharpe ratio 1.08

- Equal-weighted Benchmark: Annualized return 11.63%, Sharpe ratio 0.94

This result shows significant

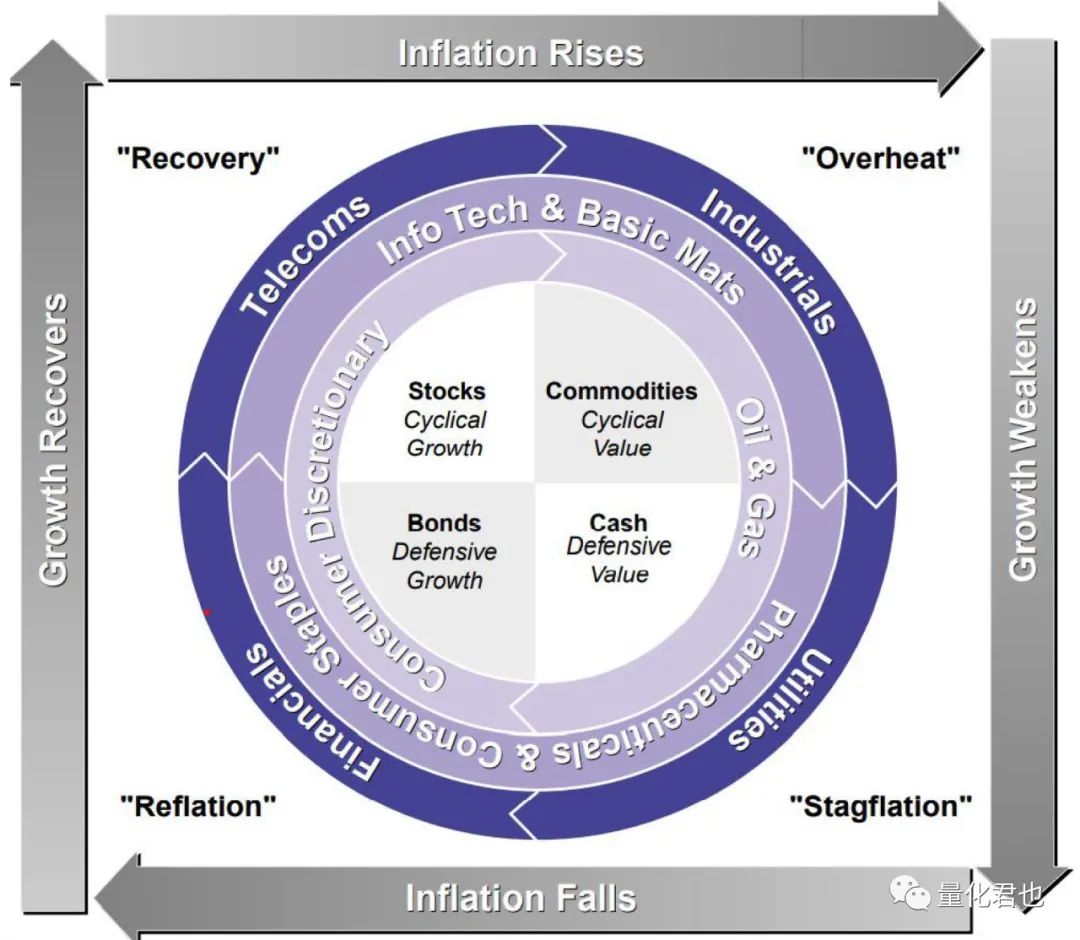

According to academic research and market practice, the momentum effect does exist in China’s market, but has the following characteristics:

- Strong short-term momentum: Short-term momentum of around 20 days is relatively obvious in China’s market

- Gradual improvement in market efficiency: As the market matures and information dissemination accelerates, the profit margin of pure momentum strategies is narrowing

- High retail participation: The high proportion of retail investors in the A-share market may lead to more significant momentum effects but also greater instability

This is the factor with the largest difference between backtest and real trading:

- ETF transaction costs: Two-way transaction costs are approximately 0.1%-0.3%

- Slippage costs: Actual transaction prices are often worse than theoretical prices

- Impact of rotation frequency: Weekly rotation means about 50 transactions per year, with cumulative transaction costs reaching 5%-15%

- Theoretical backtest: 24.24%

- After deducting transaction costs: Approximately 10%-15%

- After deducting management fees: May drop to 8%-12%

The performance of momentum strategies varies significantly in different market environments:

| Market Environment | Strategy Performance | Risk Factors |

|---|---|---|

| Trending market | Excellent performance | Clear momentum signals |

| Volatile market | Poor performance | Frequent false breakouts |

| Market reversal | Faces ‘momentum crash’ risk | Short-term large losses |

- Four-asset rotation requires quick position switching

- Some ETFs may experience insufficient liquidity during specific periods

- Impact costs increase significantly when large funds are operated

- Popularization of quantitative strategies leads to narrowing alpha

- Faster information dissemination shortens the momentum cycle

- Increased capital in similar strategies reduces profit margins

- When multiple funds use similar strategies, returns are exhausted in advance

- Herding effect may lead to large losses when the strategy fails

- Increased institutionalization of the market and decreased proportion of retail investors

- Changes in regulatory policies may affect market operation modes

- The A-share market still has many irrational trading behaviors

- Obvious policy-driven market characteristics, with more trending opportunities

- Large market sentiment fluctuations, momentum effect may persist

- Changes in economic cycles and monetary policies create rotation opportunities

- Correlations between different asset classes will not disappear completely

- Historical backtest: 24.24%

- Actual expectation: 10%-15% (after considering transaction costs)

- Conservative estimate: 8%-12% (after considering market environment changes)

- Consider extending the lookback period (e.g., 60 days) to reduce transaction frequency

- Set stop-loss mechanisms to control ‘momentum crash’ risk

- Avoid frequent operations during extremely volatile markets

- Combine with other strategies (e.g., value, quality factors)

- Set maximum drawdown limits (e.g.,15%-20%)

- Consider adding market environment identification mechanisms

- Choose low-cost ETF products

- Optimize transaction execution to reduce slippage

- Consider adjusting rotation frequency (e.g., biweekly or monthly)

Regular evaluation is needed:

- Performance of the strategy in different market environments

- Actual situation of transaction costs

- Comparison with benchmarks (e.g., CSI 300, CSI 500)

The high returns from historical backtests are difficult to fully replicate, mainly due to:

- Transaction cost erosion: Actual returns may decrease by more than 10%-15%

- Market environment changes: The future market may be more volatile or more efficient

- Strategy crowding risk: Increased similar strategies reduce profit margins

- Overfitting risk: Backtest parameters may be over-optimized

- Reasonable expectations: Setting an annual return target of 10%-15% is more realistic

- Strict risk control: Set stop-loss and maximum drawdown limits

- Dynamic adjustment: Adjust parameters according to market environment changes

- Portfolio allocation: Treat the rotation strategy as part of the overall asset allocation, not the whole

[1] Bank Stock Rotation Effect and High Dividend Strategy - Yahoo Finance

[2] Guide to Momentum Trading Strategies - Investopedia

[3] Quantitative Investment Strategies: Models, Algorithms, and Techniques - Investopedia

[4] Research on Asset Rotation Strategies in China’s A-share Market (2024-2025) - Yahoo Finance

[5] Application of Quantitative Analysis in Finance - Investopedia

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.