GOOGL Six Figure Gains: AI Growth Strategy and Market Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on a Reddit post published on November 7, 2025, where an investor detailed their successful GOOGL investment strategy resulting in six-figure gains. The author implemented a concentrated position strategy, purchasing LEAPs in February and additional shares in July, anticipating favorable court rulings and AI-driven growth [0].

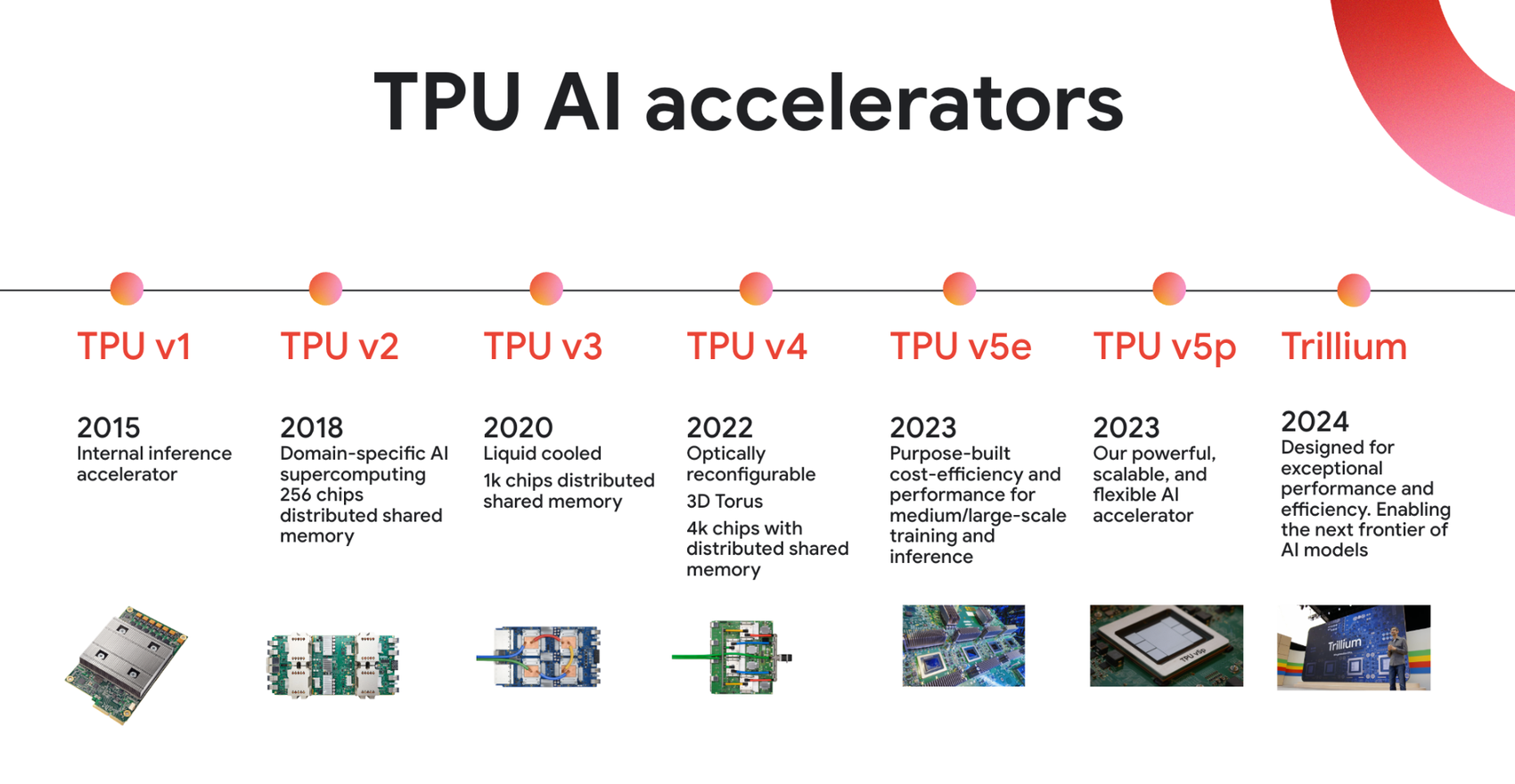

The investor’s core thesis positions GOOGL for Nvidia-like AI growth, driven by three key pillars: Tensor Processing Units (TPUs) for AI infrastructure, Google Cloud’s massive scaling opportunity with a $150+ billion backlog, and deep integration of Gemini AI across Google’s ecosystem. This long-term conviction approach involved minimal position trimming and milestone-based selling plans [0].

GOOGL’s exceptional Q3 2025 results validate the investment thesis, with record revenue of $102.35 billion and EPS of $2.87, significantly surpassing market expectations [0]. The company’s AI momentum is evidenced by Gemini AI reaching 650 million monthly active users with 3x query growth from Q2 2025 [0].

Google Cloud emerged as the primary growth engine, accelerating to 34% revenue growth with $15.15 billion in Q3, while maintaining an impressive $155 billion backlog [0]. The company increased its AI infrastructure investment to $91-93 billion for 2025, up from previous estimates of $85 billion, demonstrating commitment to AI leadership [0].

A landmark strategic partnership with Apple worth $1 billion annually to power AI Siri using Gemini represents significant competitive moat expansion [0, 4]. This deal not only provides substantial recurring revenue but also positions Google’s AI technology at the center of Apple’s ecosystem.

Waymo’s autonomous vehicle expansion to Silicon Valley, Austin, and planned San Diego rollout demonstrates Google’s diversification beyond core search and cloud, with the service achieving 200,000 weekly paid rides [0, 6].

The AI sector in 2025 experienced a paradox of unprecedented growth alongside mounting bubble fears and market volatility [0]. High-valuation tech stocks, including GOOGL, faced pressure from AI bubble concerns and economic jitters [1, 15]. However, investor sentiment shifted from speculative AI plays to established companies with proven business models and real revenue, benefiting GOOGL [0].

Enterprise AI adoption accelerated significantly, with Google signing more billion-dollar deals in the first nine months of 2025 than in the previous two years combined [0]. This enterprise momentum provides sustainable growth drivers beyond consumer-facing AI applications.

Despite intensifying regulatory headwinds affecting Big Tech, Google has navigated challenges through strategic acquisitions and continued AI investment [0, 8]. The DOJ’s approval of Alphabet’s $32 billion Wiz deal demonstrates the company’s ability to expand cloud security leadership while managing regulatory scrutiny [13].

Google has successfully regained its AI edge after earlier periods of perceived lag, with Reuters highlighting how the company’s comprehensive AI strategy spanning hardware (TPUs), software (Gemini), and cloud infrastructure created sustainable competitive advantages [12]. This multi-layered approach differentiates GOOGL from competitors focused on single AI segments.

The company’s strategic expansion beyond advertising revenue has proven highly successful, with Google Cloud now representing a substantial growth driver. The $155 billion backlog provides visibility into future revenue streams, while the Apple partnership creates a new high-margin revenue source [0, 4].

GOOGL’s increased capital expenditure to $91-93 billion for AI infrastructure reflects a strategic investment cycle similar to Nvidia’s successful data center expansion. This massive investment in TPUs and AI-specific computing power creates barriers to entry for competitors [0, 9].

The market’s confidence in GOOGL’s AI strategy is reflected in analyst sentiment, with 57 Buy ratings versus 0 Sell ratings and an average price target of $309.92 [0]. This consensus suggests professional investors share the Reddit author’s growth thesis.

- AI Bubble Volatility: High-valuation tech stocks remain susceptible to market corrections as AI bubble fears persist [1, 11, 15]

- Regulatory Pressure: Intensifying antitrust scrutiny could impact business practices and growth strategies [8, 16]

- Competition Intensification: Major tech rivals are investing heavily in AI infrastructure, potentially eroding market share [9]

- Economic Sensitivity: Advertising revenue remains vulnerable to economic downturns despite diversification efforts

- Enterprise AI Leadership: The accelerating enterprise AI adoption cycle favors established players with proven reliability [0]

- Cloud Market Expansion: Google Cloud’s growth rate significantly exceeds overall cloud market growth, indicating share gains [0]

- AI Monetization: Gemini’s integration across Google’s ecosystem creates multiple monetization pathways [0, 3]

- Autonomous Vehicle Market: Waymo’s expansion positions Google for leadership in the emerging autonomous transportation market [0, 6]

GOOGL’s strong balance sheet, diversified revenue streams, and technological leadership provide resilience against market volatility. The company’s initiation of quarterly dividend payments demonstrates confidence in sustainable cash flow generation [0].

Based on comprehensive analysis of the Reddit investment strategy and supporting market data, GOOGL represents a compelling case study in successful AI investment timing and thesis execution. The investor’s concentrated position strategy, while high-risk, capitalized on several key catalysts:

- Timing Excellence: February LEAP purchases and July share accumulation preceded major AI milestones and partnership announcements

- Thesis Validation: Strong Q3 2025 results and strategic partnerships confirmed the AI growth narrative

- Market Position: GOOGL’s combination of hardware (TPUs), software (Gemini), and infrastructure (Google Cloud) creates comprehensive AI exposure

- Financial Strength: Record revenue and earnings provide foundation for continued AI investment and shareholder returns

The analysis suggests that while AI sector volatility presents ongoing risks, GOOGL’s diversified business model, technological leadership, and strategic partnerships position the company for sustained AI-driven growth. The investor’s milestone-based selling approach aligns with professional risk management practices for concentrated positions [0].

Market data indicates continued analyst confidence with strong buy recommendations and price targets suggesting further upside potential. However, investors should monitor AI bubble dynamics and regulatory developments as key risk factors affecting the investment thesis [0, 1, 8].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.