Treasury Yield Spike Analysis: Fed Rate Cuts vs Market Reality

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on the MarketWatch report [1] published on October 30, 2025, which reported that Federal Reserve Chair Jerome Powell triggered a backup in Treasury yields despite the Fed’s rate-cutting action.

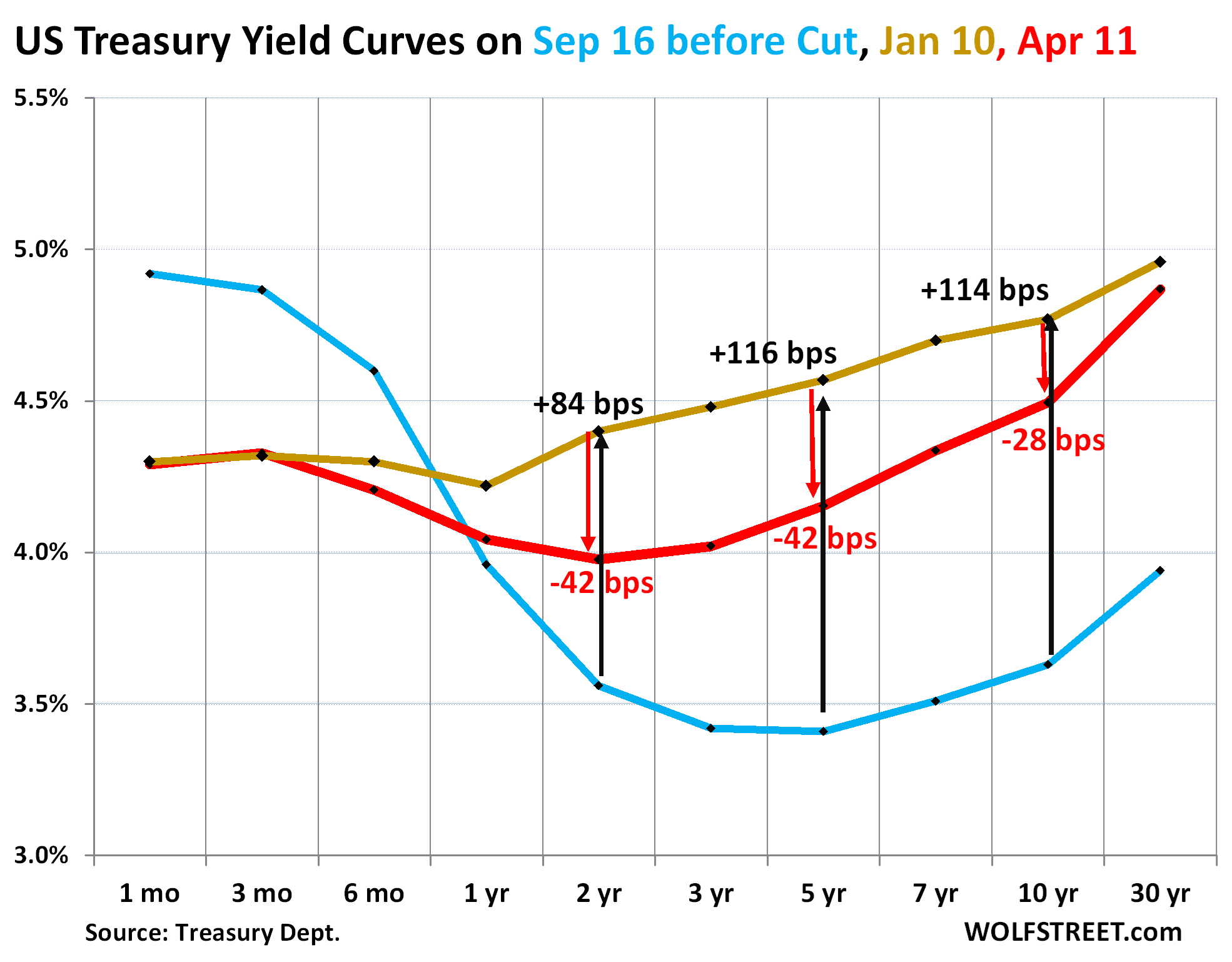

The market experienced a significant disconnect between Federal Reserve policy action and market reaction on October 30, 2025. Despite the Fed lowering its policy rate by 25 basis points to a target range of 3.75%-4.00%, the 10-year Treasury yield surged to approximately 4.09%, posting its biggest jump since July [1]. This yield spike represents a rapid 10-basis point increase from the 3.99% level recorded on October 28, 2025, according to FRED data [2].

The bond market reaction was immediate and substantial, with long-term Treasury securities particularly affected. The iShares 20+ Year Treasury Bond ETF (TLT) declined 0.57% to $90.57, while the Vanguard Total Bond Market ETF (BND) fell 0.17% to $74.60 [0]. Long-term Treasury securities experienced even steeper declines, with TLT falling 1% and VGLT dropping 0.9% on Wednesday alone [1].

Equity markets also felt the impact, with the tech-heavy NASDAQ experiencing the steepest decline at -1.57%, closing at 23,581.14. The S&P 500 fell 0.99% to 6,822.34, while the Dow Jones showed relative resilience with a 0.23% decline to 47,522.12 [0].

Powell’s hawkish messaging was delivered intentionally during his opening remarks, not as off-the-cuff comments, sending what analysts described as a “clear message” to markets [1]. The Fed Chair emphasized “strongly differing views” within the Fed about another rate cut in December, stating it was “far” from a “foregone conclusion” [1]. This communication strategy effectively reset market expectations that had previously priced a December rate cut as a “virtual lock.”

The CME FedWatch Tool showed traders dialed back December cut probability to approximately 73% following the press conference [1]. This repricing reflects growing uncertainty about the Fed’s policy path, with BlackRock’s Rick Rieder suggesting an increased chance of a skipped December cut that could delay further accommodative moves into 2026 [1].

Powell highlighted the Fed’s complex balancing act between inflation concerns and labor market uncertainty. He specifically noted that “higher tariffs are pushing up prices in some categories of goods, resulting in higher overall inflation” [1]. The Fed Chair also referenced the policy stance, stating “now we’re 150 basis points closer to neutral, wherever that may be, than we were a year ago” [1].

The yield spike reflects broader structural concerns including large government deficits and the Treasury’s appetite for long-term issuance [1]. The upcoming Treasury Department quarterly refunding announcement next week adds another layer of uncertainty, as the specific duration and composition of Treasury issuance will be crucial for market direction [1].

-

Policy Uncertainty: The Fed’s internal division on rate cuts may significantly impact market volatility through year-end [1]. Users should be aware that the combination of policy uncertainty and inflation concerns creates heightened sensitivity to economic data releases.

-

Inflation Persistence: Historical patterns suggest that tariff-driven inflation typically leads to prolonged price pressures. The risk that a “one-time increase in the price level does not become an ongoing inflation problem” remains a key concern [1].

-

Bond Market Volatility: The disconnect between Fed rate cuts and rising yields indicates potential for continued bond market turbulence [1][2]. This divergence suggests that traditional relationships between monetary policy and bond yields may be temporarily disrupted.

-

Treasury Refunding Announcement: The Treasury Department’s statement on issuance composition next week will be critical for market direction [1].

-

December Fed Meeting: The FOMC decision on December 9-10 regarding rate cuts will provide clarity on policy trajectory [1].

-

Inflation Data: Upcoming CPI and PCE reports will offer evidence on whether tariff-related inflation effects are “relatively short-lived” or becoming “more persistent” [1].

-

Labor Market Indicators: Employment data will help assess the downside risks to the labor market that Powell referenced [1].

There’s a notable split among market participants. Wells Fargo Investment Institute views the current volatility as a “buying opportunity” given the “pretty clear trend here in place for lower rates” [1]. However, the more cautious perspective from BlackRock suggests potential for delayed accommodative moves into 2026 [1].

The analysis reveals several critical factors driving Treasury market dynamics:

- Yield Spike: 10-year Treasury yield rose to 4.09% despite Fed rate cuts, representing a significant market disconnect [1][2]

- Bond Market Impact: Major bond ETFs declined sharply, with long-term Treasuries experiencing the steepest losses [0][1]

- Policy Communication: Powell’s intentional hawkish messaging successfully reset market expectations for December rate cuts [1]

- Economic Context: Tariff-driven inflation and labor market uncertainty create complex policy challenges [1]

- Market Divergence: Professional investors remain split on whether current volatility represents a buying opportunity or signals prolonged uncertainty [1]

The combination of Fed policy uncertainty, inflation concerns, and large government financing needs may significantly impact bond market stability and borrowing costs across the economy. The divergence between monetary policy action and market reaction suggests heightened sensitivity to economic data releases and Fed communications through year-end.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.